Check These Before You Transfer an Account From Vanguard

I received an email from Vanguard notifying me of upcoming changes to its fee schedule. The one change that stands out for me is that Vanguard may charge $100 effective July 1 if I transfer an account to another broker unless I have $5 million with Vanguard.

I’ve been investing with Vanguard for over 25 years. I have had the feeling from some changes by Vanguard in recent years that I’m not as valued as before. This latest announcement finally pushed me to the inevitable. I submitted a request to transfer my account to Fidelity before the new fee takes effect.

If you’re thinking along the same lines, you should check a few things before you transfer your accounts out of Vanguard.

Table of Contents1. Do you have a taxable account at Vanguard?2. Cost Basis Method Election in Taxable Account3. Do you have Vanguard mutual funds?4. Do your Vanguard mutual funds have ETF shares?5. Wait for Everything to Settle6. Save Cost Basis Details of Taxable Accounts7. Save Account Number and Recent Statement8. Request Transfer of Assets at the Receiving Firm9. Verify Cost Basis in Taxable Account10. Residual Sweep11. Dividend Reinvestment and Cost Basis Settings in the New Account1. Do you have a taxable account at Vanguard?Tax-advantaged accounts such as Traditional and Roth IRAs can be transferred to another broker without tax consequences. The transfer doesn’t generate a 1099 form. It doesn’t count toward your annual contribution limit. Please skip to Step 3 if you only have tax-advantaged accounts at Vanguard.

Transferring a regular taxable brokerage account needs more careful attention.

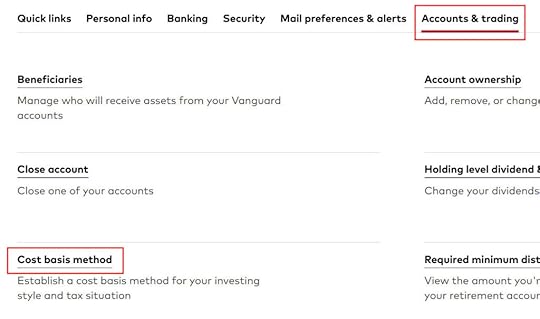

2. Cost Basis Method Election in Taxable AccountIf you have mutual funds (not stocks, ETFs, bonds, or brokered CDs) in a regular taxable brokerage account, you should first make sure the cost basis method of your holdings is set to Specific Identification (“SpecId”). The default cost basis method for mutual funds is Average Cost. Setting it to SpecId will transfer the cost basis of each tax lot when you transfer your account. It’ll help you minimize taxes when you sell in the future.

This only applies to taxable accounts. You don’t need to do anything with the cost basis method in tax-advantaged accounts.

You can see or change your current setting in Profile & settings (the head icon) -> Accounts & trading tab -> Cost basis method.

The change may take a day or two to complete. Wait until it’s done before you continue.

3. Do you have Vanguard mutual funds?Individual stocks, ETFs, bonds, and brokered CDs are all equally available at another broker. You can transfer these easily to another broker and hold, buy, or sell them at the new broker. Please skip to Step 5 if you only have individual stocks, ETFs, bonds, and brokered CDs in your Vanguard account.

If you have Vanguard mutual funds, there’s usually no charge for holding existing shares or automatically reinvesting dividends at another broker but you may have to pay a commission when you buy more shares of those funds. Fidelity and Charles Schwab don’t charge a commission for selling shares of Vanguard mutual funds you already own but they do charge for buying additional shares outside of automatic dividend reinvestments. Some other brokers charge for both buying and selling.

I have Vanguard mutual funds but I’m not buying new shares in those funds. I will only hold, automatically reinvest dividends, and sell my existing shares over time. I won’t incur any fees when I hold my Vanguard mutual funds at Fidelity.

4. Do your Vanguard mutual funds have ETF shares?If you have Vanguard mutual funds and you want to buy more shares in the future besides automatically reinvesting dividends, see if your funds are also available as an ETF. Look up the fund on Vanguard’s website. If the fund is also available as an ETF, it will say so under the name of the fund.

Vanguard can convert these mutual funds to the equivalent ETF tax-free without a fee. You’ll need to call Vanguard to convert them to ETF. After your funds are converted to ETFs, you can transfer the resulting ETFs to another broker and buy more shares of the ETFs at the new broker.

Be sure to complete Step 2 before you call Vanguard to convert your mutual fund to ETF in a taxable account. If the mutual fund is still on the Average Cost method when it gets converted, the converted ETF will only have the average cost.

There’s a small risk that Vanguard will mess up the cost basis when you convert your mutual funds to ETFs in a taxable account. I didn’t want to take that chance when I transferred a taxable account from Vanguard. I’m OK with only holding the Vanguard mutual funds, automatically reinvesting dividends, and selling without a commission at Fidelity. I just won’t buy new shares.

Some Vanguard funds aren’t available as an ETF. If you transfer your account, buying new shares of those funds will likely incur a commission at the new broker. You’ll have to find an alternative. Some Vanguard funds not available as an ETF are still the best-in-class. Maybe you should keep your account at Vanguard if you will buy more shares of those funds.

5. Wait for Everything to SettleIf you decide to transfer and you have recent transactions in your Vanguard account (money in, money out, trades, converting mutual funds to ETFs), you should wait for everything to settle before you transfer your account. It’s easier for everyone if you transfer when nothing is in the air.

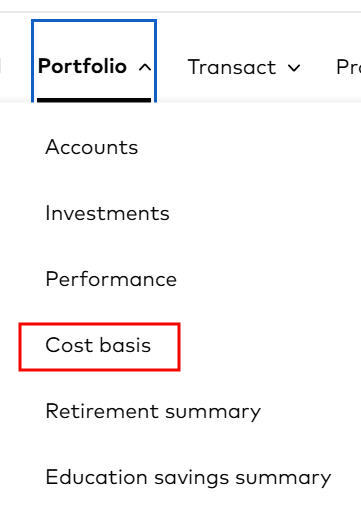

6. Save Cost Basis Details of Taxable AccountsIt’s important to keep the cost basis records accurate when you transfer a taxable account. You should save or print your cost basis details before you transfer. This doesn’t apply to tax-advantaged accounts.

You see these details under Portfolio -> Cost basis.

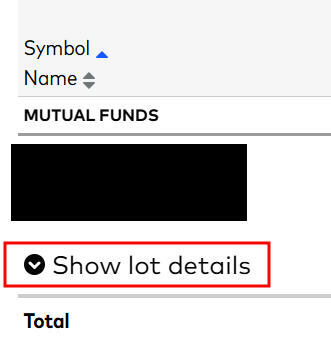

Expand “Show lot details” under each holding. Save the page to a PDF or print it.

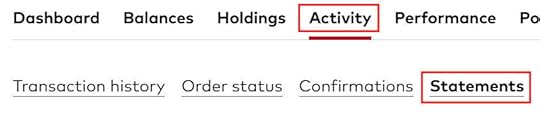

7. Save Account Number and Recent StatementYou’ll need to give your Vanguard account number and a recent statement when you transfer your account. The statements are under Activity -> Statements.

The statement doesn’t show your full account number. You need to copy your account number and save it separately.

8. Request Transfer of Assets at the Receiving FirmYou should initiate the transfer at the receiving firm. The process is usually online. It’s under Accounts & Trade -> Transfers and then “Move an account to Fidelity” in Fidelity. Look for something similar at other brokers.

You’ll be asked where you’re transferring from, the account number at the sending firm, what type of account it is, whether you’d like to transfer everything in the account or only part of it, whether you’re transferring into an existing account or a new account (and create this new account when applicable), and finally to attach a recent account statement of the source account.

The account type should match (Traditional-to-Traditional, Roth-to-Roth, taxable-to-taxable, trust-to-trust). The account name should also match (individual-to-individual, joint-to-joint). If they don’t match, please fix them on either side first.

If you’re asked whether you’d like to transfer in-kind or sell and transfer cash, make sure to choose in-kind. In-kind means transferring each holding as-is without any change. Only transferring in-kind won’t trigger taxes in a taxable account.

The transfer usually takes a week or sooner to complete.

9. Verify Cost Basis in Taxable AccountIf the transfer is successful, the holdings will come over first without the cost basis details. That’s normal. The cost basis details will come in another week or two. You should verify the cost basis details against the records you saved in Step 6.

10. Residual SweepIf you do a full account transfer and any of your investments paid dividends during the transfer, the dividends may still go into your old account. There will be another automatic sweep to transfer any residual amounts. You don’t have to initiate it. It will come over in a few weeks.

11. Dividend Reinvestment and Cost Basis Settings in the New AccountDividend reinvestment and cost basis tracking method for your newly transferred holdings will follow the settings in the receiving account. Take a look and set them to your preference.

I automatically reinvest dividends and use the default cost basis method in tax-advantaged accounts. In a taxable account, I automatically send the dividends to the spending account and use Actual Cost for cost basis and Fidelity’s Tax-Sensitive default disposal method.

***

Transferring a Vanguard account isn’t difficult but it requires some planning, especially when you’re transferring a taxable account with mutual funds. Sometimes it’s better not to transfer. The most important parts are not to sell anything and trigger taxes and to preserve the cost basis records for individual lots in taxable accounts.

Learn the Nuts and Bolts I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read Reviews

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read ReviewsThe post Check These Before You Transfer an Account From Vanguard appeared first on The Finance Buff.

Harry Sit's Blog

- Harry Sit's profile

- 1 follower