2023 Mortgage Interest Limit in TurboTax, H&R Block, FreeTaxUSA

[Updated on January 30, 2024 with screenshots for 2023 tax filing.]

Many homeowners refinanced to a sub-3% mortgage when interest rates were low a couple of years ago. The mortgage interest most people pay isn’t large enough to make them itemize their deductions. They just take the standard deduction. Those who can still deduct their mortgage interest tend to have a large mortgage.

Table of ContentsLimit on DeductionAverage Mortgage BalanceTurboTaxH&R BlockFreeTaxUSALimit on DeductionThe Tax Cuts and Jobs Act of 2017 reduced the limit on the mortgage balance on which you can deduct the mortgage interest from $1 million to $750,000. The lower limit applies to homes acquired after December 15, 2017. The large increase in home prices in recent years makes recently bought homes in high-price areas more likely to exceed the $750,000 limit.

However, lenders still report 100% of the mortgage interest paid on the 1098 form without adjusting for either the old $1 million limit or the new $750,000 limit. If your mortgage balance is over the limit, deducting the mortgage interest is more complicated than just using the number from the 1098 form.

It isn’t simply multiplying $750,000 by your interest rate either when your mortgage balance started above $750,000 and ended below $750,000 or when you took out the loan in the middle of the year.

Average Mortgage BalanceA key concept is your average mortgage balance during the year. When your average mortgage balance exceeds the limit, your deductible mortgage interest is:

Loan Limit / Average Mortgage Balance * Actual Mortage Interest Paid

If you paid $30,000 in mortgage interest on an average mortgage balance of $1,000,000 and you’re subject to the $750,000 limit, your deductible mortgage interest is pro-rated to:

$750,000 / $1,000,000 * $30,000 = $22,500

IRS Publication 936 gives several ways to calculate your average mortgage balance:

Average of first and last balance methodInterest paid divided by interest rate methodMortgage statements methodThe first method is simpler and it gives you a slightly larger deduction but you can use it only if you didn’t prepay more than one month’s principal during the year.

Here’s how it works in TurboTax, H&R Block, and FreeTaxUSA tax software.

TurboTaxThe screenshots below are taken from TurboTax Deluxe downloaded software. The TurboTax downloaded software is both less expensive and more powerful than TurboTax online software. If you haven’t paid for your TurboTax online filing yet, you can buy TurboTax download from Amazon, Costco, Walmart, and many other places and switch from TurboTax online to TurboTax download (see instructions for how to make the switch from TurboTax).

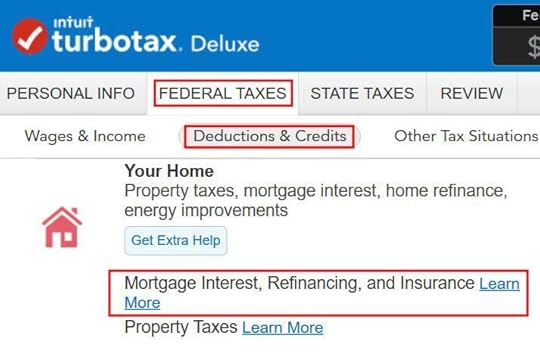

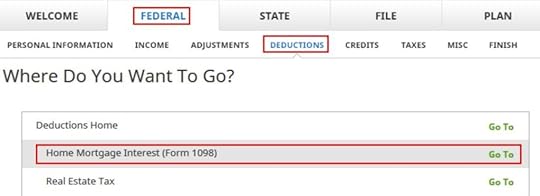

Find the mortgage interest topic in the Your Home section under Federal Taxes -> Deduction & Credits.

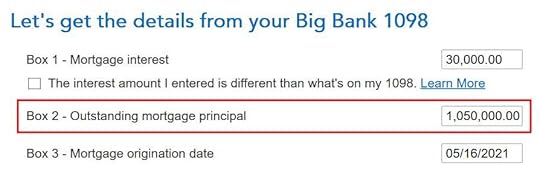

Form 1098

When it asks you to enter information from your 1098 form, enter the numbers as they appear on your form. If Box 2 is blank on your 1098, enter the mortgage balance at the beginning of the year (or your beginning loan balance if you took out the loan during the year).

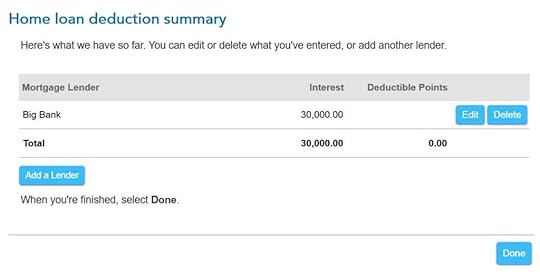

You get to this summary after you answer a few more questions. Click on Done but you’re not done yet.

Purchase Date and Ending Balance

The purchase date of the home determines whether you have a $1 million limit or a $750,000 limit for the mortgage interest deduction. If this mortgage was from a refinance, you still enter the date when you originally bought the home.

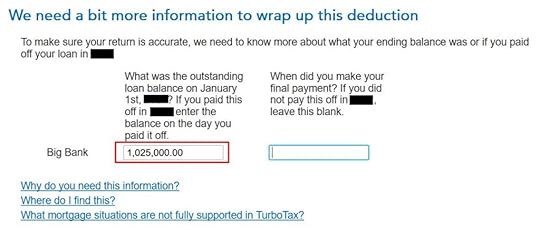

TurboTax asks for the balance as of January 1 of the following year because it uses the “average of first and last balance method” to calculate your average mortgage balance for the year. This works when you didn’t make extra principal payments during the year.

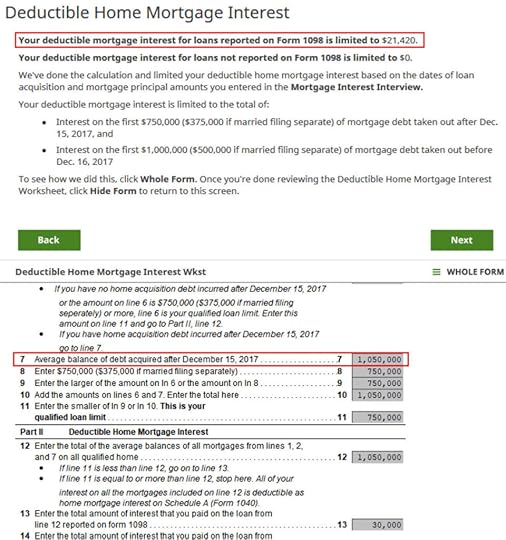

TurboTax calculates a deduction using the “average of first and last balance method” but you can’t legally use that method if you prepaid more than one month’s principal during the year. You must calculate your average mortgage balance in a different way and give the pro-rated deductible mortgage interest to TurboTax.

If You Prepaid PrincipalIf you had the mortgage for all 12 months and your interest rate didn’t change during the year, which is the case for most people with a fixed-rate mortgage, you can use the “interest paid divided by interest rate method” to calculate your average mortgage balance. Suppose you paid $30,000 in mortgage interest and your rate is 2.875%, your average mortgage balance is:

$30,000 / 0.02875 = $1,043,478

Your deductible mortgage interest is:

$750,000 / $1,043,478 * $30,000 = $21,562

If your interest changed during the year, you’re better off using the “mortgage statements method.” Download the monthly statements from your lender. Add up your balance from January to December and divide by 12. That’s your average mortgage balance during the year. Use that number to calculate your pro-rated deductible mortgage interest and give it to TurboTax:

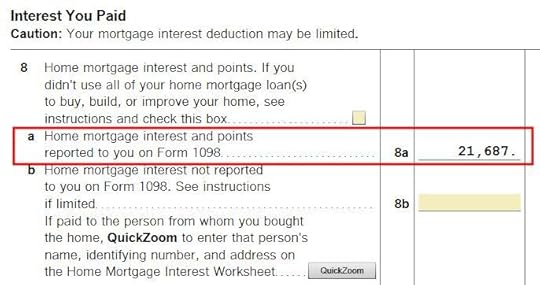

Verify on Schedule ALoan Limit / Average Mortgage Balance * Actual Mortage Interest Paid

To confirm how much mortgage interest deduction you’re getting, click on Forms on the top right and find Schedule A in the list of forms in the left panel.

Scroll down to the middle and find Line 8. You’ll see the mortgage interest deduction.

H&R BlockMortgage interest deduction works differently in the H&R Block software.

Find “Home Mortgage Interest (Form 1098)” under Federal -> Deductions.

1098 Entries

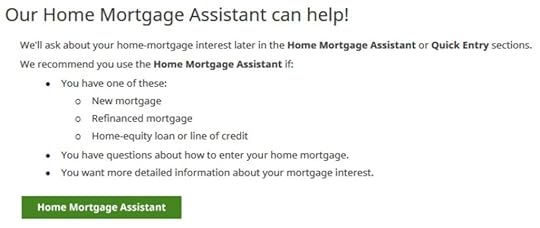

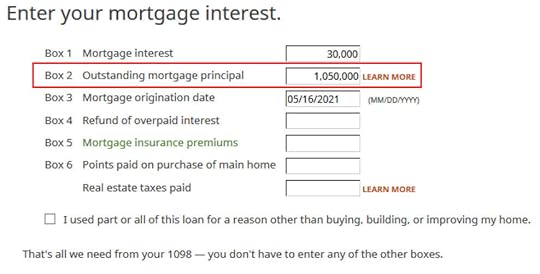

H&R Block offers a Home Mortgage Assistant. Click on that.

After saying we have a 1098 form and entering the name of the lender, we come to this form to enter the numbers on the 1098 form.

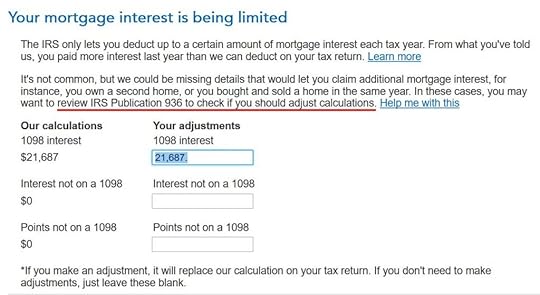

The IRS instructs banks to put in Box 2 your mortgage balance as of the beginning of the year (or your beginning loan balance if you took out the loan during the year) but H&R Block treats it as your average balance during the year. This is wrong and it reduces your mortgage interest deduction.

Calculate Average Mortgage BalanceYou should calculate the average mortgage balance yourself and put it in Box 2.

If you didn’t prepay more than one month’s principal, get the beginning balance and the ending balance. Take an average.If you prepaid more than one month’s principal but your interest rate didn’t change, divide the interest paid by your interest rate.If you prepaid more than one month’s principal and your interest rate changed during the year, get your balance as of the beginning of each month and take an average.Suppose your beginning balance was $1,100,000 and your ending balance was $1,000,000, and you didn’t prepay more than one month’s principal during the year, your average balance using the first method is

( $1,100,000 + $1,000,000 ) / 2 = $1,050,000

You also need to enter the date when you purchased the home in Box 3. This date determines whether you have a $1 million limit or a $750,000 limit for the mortgage interest deduction. If this mortgage was from a refinance and the bank put the refinance date in Box 3, you should overwrite it with the date when you originally bought the home.

Mortgage Interest Deduction

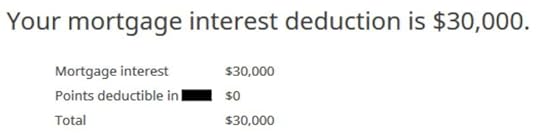

After answering some more questions about points and mortgage insurance premiums, which we don’t have, H&R Block says we can deduct 100% of the mortgage interest paid. This can’t be right. We entered a balance above $1 million on the 1098 form. H&R Block just uses the interest paid number from the 1098 form as if the loan limit doesn’t exist.

You see this when you click on “Finished” after you’re done with all your 1098 forms. H&R Block calculates a mortgage interest deduction subject to the loan limit. You can see it’s using the number from the 1098 form as the average mortgage balance. It would use the larger beginning balance reported by the bank and give you a smaller deduction if you didn’t overwrite the number with the average balance you calculated yourself.

Granted that TurboTax doesn’t cover all situations but at least it makes an attempt to cover the most common scenario (only regular payments without extra principal payments). H&R Block just uses a wrong number without telling you. That’s bad. Although only a small percentage of people deduct their mortgage interest now, among those who can still deduct, many have a mortgage above the limit.

FreeTaxUSAI also checked how the online tax software FreeTaxUSA does it.

FreeTaxUSA puts a small question mark link next to the mortgage interest entry. Clicking on the question mark opens a pop-up, which says toward the end:

If your debt is higher than the limits, use Publication 936 to figure out your deductible home mortgage interest amount and reduce the mortgage interest you enter accordingly.

You’re on your own when you use FreeTaxUSA. It doesn’t tell you clearly that you must do some extra work. You would’ve claimed more deduction that you’re eligible for if you didn’t know to click on that question mark and read the whole pop-up.

***

H&R Block tax software is less expensive than TurboTax but using a wrong number to calculate your mortgage interest deduction can cost you many times more than the price of the software. See another example in How to Enter Foreign Tax Credit Form 1116 in H&R Block. You really have to know where it cuts corners when you use H&R Block software. It works well only when those cut corners don’t affect you. The same also applies to FreeTaxUSA.

Learn the Nuts and Bolts I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read Reviews

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read ReviewsThe post 2023 Mortgage Interest Limit in TurboTax, H&R Block, FreeTaxUSA appeared first on The Finance Buff.

Harry Sit's Blog

- Harry Sit's profile

- 1 follower