How To Report 2022 Mega Backdoor Roth In H&R Block (Updated)

[Updated on January 16, 2023 with screenshots from H&R Block tax software for 2022 tax filing.]

A Mega Backdoor Roth is different from a regular Backdoor Roth. It’s done by making non-Roth after-tax contributions to a 401k-type plan and then moving it to the Roth account within the 401k-type plan or taking the money out (with earnings) to a Roth IRA. It’s a great way to put additional money into a Roth account without having to pay much additional tax. Not all plans allow non-Roth after-tax contributions but some estimated that 40% of people can do it.

Suppose you did a Mega Backdoor Roth last year. You should have received a 1099-R form from your 401k plan provider. You’ll need to account for it on your tax return. Here’s how to do it in H&R Block downloaded software. If you use other software, please read:

How to Report Mega Backdoor Roth in TurboTax How to Report Mega Backdoor Roth in FreeTaxUSAUse H&R Block DownloadH&R Block is in general less expensive than TurboTax. It has a downloaded version and an online version. The downloaded version is both less expensive and more powerful.

The downloaded Deluxe + State edition (or the Deluxe Federal-Only edition when you live in a state without an income tax) can handle pretty much everything. It often goes on sale for $20-25 on Amazon, Walmart, or Newegg, sometimes for under $20. It includes five federal e-filing. State e-filing costs extra but you can simply print and mail or file directly with your state on their website (see Free E-File State Tax Return Directly on the State’s Website).

In-Plan RolloverYou can do the mega backdoor Roth in two ways — converting within the plan or withdrawing to a Roth IRA. Converting within the plan is much easier, and many plans automate the process. Withdrawing to a Roth IRA also works. See the previous post Mega Backdoor Roth: Convert Within Plan or Out to Roth IRA?

Let’s first look at converting to the Roth account within the plan. Here’s the scenario we’ll use as an example:

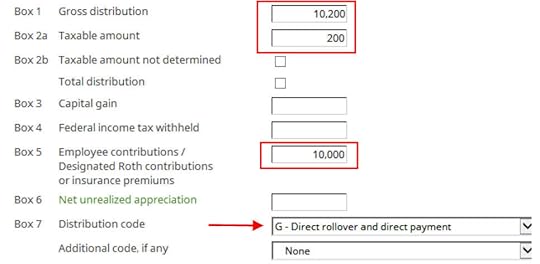

You contributed $10,000 as non-Roth after-tax contributions to your 401(k). By the time you converted the money to the Roth account within the plan, your contributions earned $200. You converted $10,200 to your Roth 401(k) account.

I’m using 401(k) as a shorthand. It works the same in a 403(b). Now here are the entries into H&R Block software.

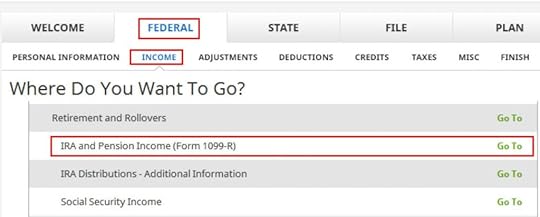

Go to Federal -> Income -> IRA and Pension Income (Form 1099-R). You can import the 1099-R or enter it manually. I’m showing manual entries.

Our 1099-R is a normal 1099-R. Enter the numbers from your 1099-R as-is. Ours looks like this:

The gross amount converted to the Roth 401k account shows up in Box 1. The earnings are in Box 2a. If you didn’t have earnings in your rollover, Box 2a is zero. “Taxable Amount Not Determined” under Box 2b is left unchecked. The amount of your non-Roth after-tax contributions shows in Box 5. Box 7 has code G.

The IRA/SEP/SIMPLE box in Box 7 on your 1099-R should NOT be checked.

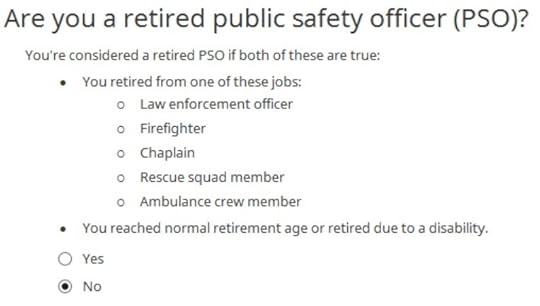

We’re not a retired public safety officer.

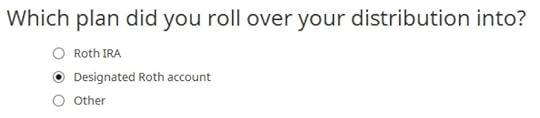

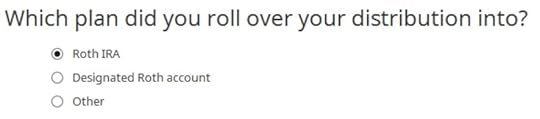

We moved the money within the plan. The Roth 401k account is officially a “designated Roth account” in the plan.

That’s it. It’s as simple as that. Now we verify we’re taxed only on the $200 in earnings, and not on the $10,000 non-Roth after-tax contributions. Click on “Forms” in the top menu bar. Double-click on “Form 1040 and Schedules 1-3” in the forms list.

Scroll down to find Line 5. The gross amount transferred to the Roth 401k account shows on Line 5a. Line 5b shows you’re taxed only on the earnings. If you didn’t have earnings, Line 5b will be zero.

Rollover to Roth IRA

Rollover to Roth IRAIt’s just as easy to report the mega backdoor Roth if you took the money out of the 401k plan and sent it to a Roth IRA. We’ll use the same example as above except you did the rollover to a Roth IRA instead of to the Roth 401k account within the plan.

Enter your 1099-R as-is in the same way as above.

The IRA/SEP/SIMPLE box is still unchecked.

We’re still not a retired public safety officer.

The only difference is we rolled over to a Roth IRA this time.

Now we verify we’re taxed only on the $200 in earnings, and not on the $10,000 non-Roth after-tax contributions. Click on “Forms” in the top menu bar. Double-click on “Form 1040 and Schedules 1-3” in the forms list.

Scroll down to find Line 5. The gross amount transferred to the Roth 401k account shows on Line 5a. Line 5b shows you’re taxed only on the earnings. If you didn’t have earnings, Line 5b will be zero.

Learn the Nuts and Bolts

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read Reviews

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read ReviewsThe post How To Report 2022 Mega Backdoor Roth In H&R Block (Updated) appeared first on The Finance Buff.

Harry Sit's Blog

- Harry Sit's profile

- 1 follower