How to Manage a Family Member’s Fidelity or Vanguard Accounts

When you have a joint account, either person on the account can transact in the account. As part of our estate planning package, my wife and I created a trust with both of us as co-trustees (see Will and Trust Through Employer Legal Plan). We stated in the trust that each trustee can act alone. Our trust account is set up as such, similar to a joint account.

Table of ContentsNo Joint IRA or Joint HSAPower of Attorney May Not Be RecognizedNot Limited to SpouseNo Sharing Login and PasswordVanguardFidelityBidirectional PermissionsNotarized SignaturesNew AccountsRevoke AuthorizationTrusted ContactsNo Joint IRA or Joint HSAHowever, our IRAs and HSAs can only be in our individual names. It’s not possible to have a joint IRA or a joint HSA.

We have named each other as the beneficiary of our IRAs and HSAs, but the beneficiary only becomes relevant after the account owner dies. When your spouse is living, you don’t have any authority over their IRA or HSA unless they specifically grant you permission.

Power of Attorney May Not Be RecognizedWe also executed a Durable Power of Attorney (DPOA) in our estate planning package. We granted the authority to act on behalf of each other in case we aren’t capable to act ourselves, but we also learned that financial institutions often don’t recognize these generic Powers of Attorney. They want their own language specific to accounts at their institution.

It’ll be a bummer if you’re only told they don’t accept your Power of Attorney when you really need to use it. Most financial institutions have a process to get authorization from someone to transact in their accounts. It’s better to be prepared and go through the process before you need to act on someone’s behalf.

Not Limited to SpouseAlthough it’s most common to get authorization from your spouse, the authorization process doesn’t limit it to a spouse. The account owner can grant authorization to anyone — a sibling, an adult child, or even a non-family member.

Except for a married couple, it’s better in many situations to only get authorization to manage the accounts and not become a joint owner (you can’t be a joint owner of a retirement account anyway). You may be responsible for part of the taxes if you’re a joint owner.

No Sharing Login and PasswordGoing through the official authorization process is the right way to do it. Using another person’s login and password can weaken their protection from the financial institution. It can also put you in a position where you can be accused of identity theft or hacking.

After the account owner gives authorization, you should log in with your own username and password when you manage their accounts.

VanguardWe have IRAs at Vanguard. Vanguard has a process for an account owner to authorize another person to act on their behalf over their accounts. They call it agent authorization or account permissions.

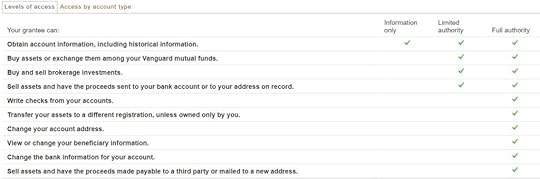

Vanguard allows three levels of access.

If you have Information Only access, you can monitor the account but you can’t do anything.If you have Limited Authority, you can transact within the account or send money out to an already-linked bank account or the address on file. If you have Full Authority, you can do a number of other things.The process has to be initiated by the account owner.

You can grant the Information Only or Limited Authority permission online. It’s not clear how you can grant Full Authority. It looks like there used to be an Agent Authorization form but all the links to the form are dead on Vanguard’s website. Please contact Vanguard customer service to get the form for Full Authority.

Here’s how to grant Information Only or Limited Authority permission online:

After logging in to Vanguard, click on “Profile & account settings” at the top. Then click on the Security tab and “Account permissions.”

The grantee must also have a Vanguard account. The account owner needs one of the grantee’s Vanguard account numbers. Vanguard will send an email to the grantee to confirm that they will accept the authorization. The permissions are effective only after the grantee accepts. The grantee will see additional accounts listed when they log in.

FidelityWe also have IRAs and HSAs at Fidelity. Fidelity has a similar process for the account owner to grant permissions. They have a clear explanation and a video about their four levels of access:

The account owner can follow the link in the explainer above to start the process to authorize access to their accounts.

Similar to Vanguard, Fidelity will send an email to the person receiving the authorizations. The authorizations are effective only after the grantee accepts.

The grantee will see additional accounts listed when they log into their Fidelity account. The additional accounts will be under a separate account group. They can customize the display name of each account to something that makes more sense to them.

Bidirectional PermissionsIf a married couple would like to grant permission to each other, they need to go through the process separately from each direction.

Notarized SignaturesGranting the highest level of authorization — Full Authority in Vanguard and Power of Attorney in Fidelity — requires notarized signatures from both parties and witnesses. If you’d like to grant access at the highest level, you can grant at the second-highest level online first while you work on the paperwork for the highest level.

New AccountsThe authorizations are for specific accounts. They don’t automatically apply to new accounts. Remember to go through the authorization process again for new accounts.

Revoke AuthorizationThe account owner can revoke the permission at any time. Follow the same process of granting authorization to revoke prior authorizations.

Trusted ContactsIn light of elder financial abuse and scams, new regulations require financial institutions to offer the ability to designate trusted contacts. When a financial institution suspects that a customer is being scammed or the customer has displayed diminished mental capacity, they will reach out to the trusted contacts to make sure the transactions are legit or alert the trusted contacts of potential issues.

Adding a trusted contact by itself does not give the trusted contact any permission to access the accounts but it can be used in conjunction with account access permissions. For instance, if an elderly parent adds an adult child as the trusted contact in addition to giving the adult child permission to view the accounts, the adult child can monitor the parent’s accounts and receive alerts from the financial institution for suspicious activities.

To add trusted contacts:

Fidelity: How to add a trusted contactVanguard: Profile & account settings -> Trusted ContactLearn the Nuts and Bolts I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read Reviews

I put everything I use to manage my money in a book. My Financial Toolbox guides you to a clear course of action.Read ReviewsThe post How to Manage a Family Member’s Fidelity or Vanguard Accounts appeared first on The Finance Buff.

Harry Sit's Blog

- Harry Sit's profile

- 1 follower