How To Enter Mega Backdoor Roth in FreeTaxUSA: A Walkthrough

I did a walkthrough of how to report backdoor Roth in FreeTaxUSA in a previous post. A reader asked me to do another walkthrough for how to report a mega backdoor Roth in FreeTaxUSA.

A mega backdoor Roth is different from a regular backdoor Roth. It’s done by making non-Roth after-tax contributions to a 401k-type plan and then taking the money out (with earnings) to a Roth IRA or moving it to the Roth account within the 401k-type plan. It’s a great way to put additional money into a Roth account without having to pay much additional tax. Not all plans allow non-Roth after-tax contributions but some estimated that 40% of people can do it.

FreeTaxUSA is inexpensive online tax software. It uses the freemium pricing model. Federal tax filing is free regardless of the complexity of the return. After you are done with federal, if you need to file a state return, it costs $12.95. They also offer an optional deluxe upgrade for $6.99, which includes audit assist, priority support, and amended returns. All told, with or without the deluxe upgrade, the total cost is under $20 and it includes e-filing for both federal and state.

Suppose you did a mega backdoor Roth last year. You’ll receive a 1099-R form from your 401k plan in January. You’ll need to account for it on your tax return. FreeTaxUSA makes it quite straightforward. Here’s how to do it in FreeTaxUSA.

In-Plan RolloverYou can do the mega backdoor Roth in two ways — rollover within the plan or withdraw to a Roth IRA. Rolling over within the plan is much easier, and many plans automate the process. Withdrawing to a Roth IRA also works. See the previous post Mega Backdoor Roth: Convert Within Plan or Out to Roth IRA?

Let’s first look at rolling over to the Roth account within the plan. Here’s the scenario we’ll use as an example:

You contributed $10,000 as non-Roth after-tax contributions to your 401(k). By the time the money was rolled over to the Roth account within the plan, your contributions earned $200. You rolled over $10,200 to your Roth 401(k) account.

I’m using 401(k) as a shorthand. It works the same in a 403(b). Now the entries into FreeTaxUSA.

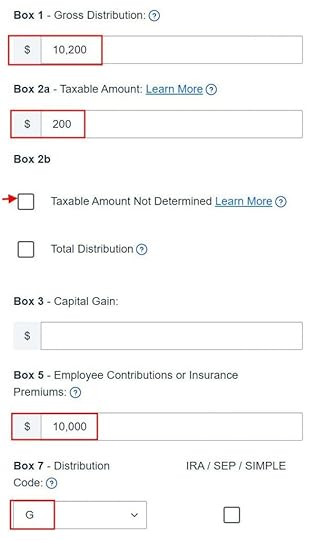

Go to Income -> Common Income -> Retirement Income (1099-R). Enter the numbers from your 1099-R as-is. Ours looks like this:

The gross amount transferred to the Roth 401k account shows up in Box 1. The earnings are in Box 2. Box 2a is left unchecked. The amount of non-Roth after-tax contributions shows in Box 5. Box 7 has code G and the IRA/SEP/SIMPLE box is unchecked. Leave the rest at default unless your 1099-R has values in other boxes.

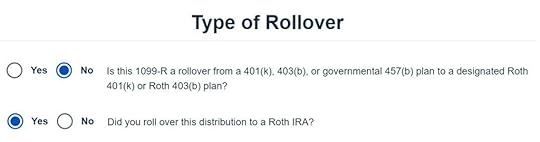

When it asks whether it was a rollover to a Roth 401(k) account, we say yes.

That’s it. It’s as simple as that. Now we verify we’re taxed only on the $200 in earnings, and not on the $10,000 non-Roth after-tax contributions.

Click on the “View Form 1040” link on the right-hand side.

A draft 1040 form pops up. Look at Line 5. Line 5a shows the gross amount transferred to the Roth 401k. Line 5b shows we’re taxable only on the $200 in earnings. If you didn’t have earnings in your rollover, Line 5b will be zero.

Rollover to Roth IRAIt’s just as easy to report the mega backdoor Roth if you took the money out of the 401k plan and sent it to a Roth IRA. We’ll use the same example as above except you did the rollover to a Roth IRA instead of to the Roth 401k account within the plan.

Enter your 1099-R as-is in the same way as above.

When it asks how we did the rollover, answer ‘No’ to the first question and ‘Yes’ to the second question.

That’s it. Verify that you’re taxed only on the earnings in the same way as above. Look at Line 5 in your draft 1040 form.

The post How To Enter Mega Backdoor Roth in FreeTaxUSA: A Walkthrough appeared first on The Finance Buff.

Harry Sit's Blog

- Harry Sit's profile

- 1 follower