The Real Term Spread and Recessions

There’s an argument being made that because of the zero lower bound, the standard nominal term spread is unlikely to be as accurate a predictor of recessions as it has in the past. A prominent example of this view circulating now is that forwarded by Deutsche Bank’s Dominic Konstam; his analysis indicates a 60% likelihood of recession (WSJ RTE), in contrast to the estimates obtained from the standard model, ranging in the low teens (see for example this post).

Konstam adjusts the term spread by using the residual of the 10 year-3 month spread on the 3 month spread as a predictor of recessions. This, it’s asserted, removes the bias that comes about from the fact that the short rate has been bound in recent years.

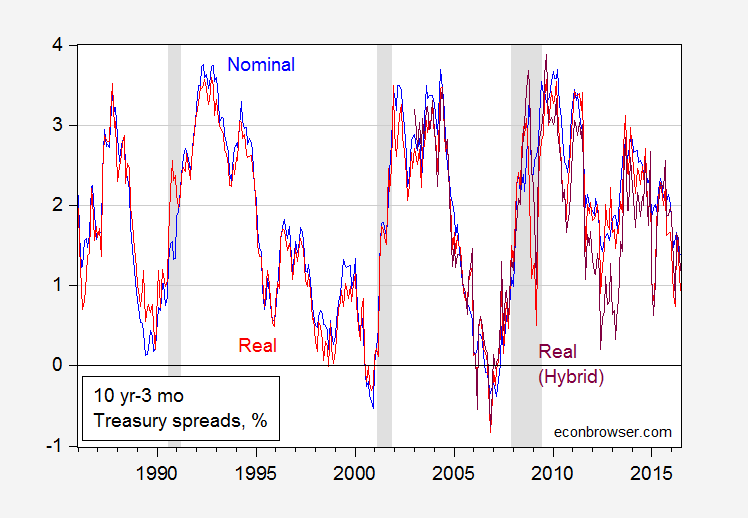

What is true is that the real interest rate, both at short and long horizons, is not bound, so in principle one could examine how the real spread covaries with recessions. Two problems arise: (1) the real rate is unobservable, and (2) for observable proxies for the real rates, the time span is short relative to the number of observed recessions. Consequently, formal analysis is not possible (or, more accurately, not advisable). Still, I think it is of interest to see whether the real spread predates recessions. This is shown in Figure 1.

Figure 1: Nominal ten year (constant maturity) yield minus three month bond yield (secondary market) (blue), nominal ten year minus ten year expected CPI inflation minus three month yield adjusted by one year expected inflation (red), and TIPS ten year minus three month yield adjusted by one year expected inflation (purple). NBER defined recession dates. Source: Treasury yields from FRED, expected inflation from Cleveland Fed, NBER, and author’s calculations.

I’ve plotted the series for the period of the “Great Moderation”; it’s not possible to go much earlier, as the expected inflation series only goes back to 1982.

Observations:

A yield curve inversion need not precede a recession — in the 1990-91 recession both curves nearly invert, but do not.

The nominal and real curves have covaried substantially over the entire sample, with some divergence in 2012-13.

All measures of the 10 year-3 month term spread remain positive.

It would be inadvisable to take too much from these correlations. However, it would seem that an unconstrained measure of the slope of the yield curve is not too different from the constrained version, at the moment (or — more accurately — as of June 2016).

Menzie David Chinn's Blog