H.J. Chammas's Blog, page 6

July 21, 2020

Why Do Wannabe Real Estate Investors Fail?

Interest in real estate investing has never been stronger. More and more people are catching on to the amazing benefits of this lucrative investment. However, it also comes with some risks, especially if you don't know what you're doing.

You don't just buy any property (with no clear set of criteria), without proper financing, and then sit and pray for money to roll in!

It's important that any starting investor understands what makes a good rental property, how to find it, and how to make profit going in. If you aren’t equipped with the right knowledge and process, you can easily lose your time and money on mistakes that could have been easily avoided.

In this article, we’ll cover 5 of the most common pitfalls that real estate investors fall into and how to avoid them.

5 Pitfalls of Buying an Investment Property to RentBefore you consider buying an investment property to rent, take a look at these common pitfalls:1. Failing to Get Your Finances in OrderMost novice investors jump on the real estate wagon without even carefully examining their personal finances. They put a down payment on a property and then get surprised that their financial situation is not fit and that they are not eligible for loans to finance the large sum of capital required to purchase properties. The end result is they lose their down payment, which could be their lifetime saving.

Investment in rental property starts with carefully examining one's financial position and then by getting a loan pre-approval. This helps having a budget on hand, which is one of the main criteria for selecting the right property that's fit for your investment goals.

Related: Getting pre-qualified for bank loans

2. Failing to Set Your Investment CriteriaOne of the most common real estate mistakes made by novices is buying an investment property to rent without a clear set of criteria. The end result might be purchasing something that puts money in other people's pockets at the loss of the investor.

For instance, in a hot market, it’s not surprising to see people on a property buying frenzy and deciding afterward what to do with them. Those investors get hooked with sales pitches of fast-talking real estate brokers promising them of quick profits, as if they have a crystal ball.

I've seen many wannabe investors fall victim of buying off-plan, parking their money for years to come, and praying to be able to sell for a profit before they register the title in their name. Many of those investors don't even have enough capital to fund the full tag price of those properties, should the bank not lend them when the property becomes ready few years down the line. Then they fail, lose their shirt, and start complaining about how risky is real estate investing.

It’s tough to succeed in any investment if you don’t know what you are looking for and what you are hoping to accomplish. Below are the main investment criteria one shall be considering when prospecting for investment properties.

All those criteria are discussed at length in The Employee Millionaire; however, it’s important to impress on you some very important points, which most starting investors fail to consider.

Location determines the price of a property, all other things being equal. The wise investor chooses a location first and then picks a property. Getting clarity on location enables the investor to narrow down the search criteria. Investors, who become experts in a certain community, will be able to compare local property values and rental rates, which will enable them to identify great deals from the average ones. Communities that are the best picks for real estate investors are those that are emerging and have an established reputation as desirable. Communities that are sought after by end users who want to live there are often close to work, schools, hospitals, retail, and recreational centers.

Related: What Does "Location Location Location" Really Mean in Rental Properties Investing

The second defining selection criterion is whether the property is finished (with a ready title deed) or still under construction. The employee millionaire strategy focuses on rental properties and therefore, by default, investing for cash flow requires properties that are finished and ready to be occupied by tenants who will pay rent. It is quite a simple and straightforward strategy. Once you understand the demand for rent and the rental rates in a certain community, it doesn’t require a crystal ball to forecast the future rental income, the expenses, and the net cash flow. This criterion is the most often overlooked by starting investors who only invest for capital gain. They end up locking their money in a property that doesn’t generate any cash flow until its construction is complete before they can sell it for a profit in the event they were lucky enough to have the market on their side.

Having a clear picture of what type of residential property, you are looking for in your defined location narrows down your search even further. The two broad decisions you will have to make here are whether you are looking for single-family homes or multifamily properties. The common wisdom is to start investing in single-family houses with less capital and less risk. Then you can grow into multifamily properties over time.

Property features are those basic descriptors used by any end user who occupies a property. Features describe the age of the property, built-up area (BUA), number of bedrooms, number of bathrooms, and number of parking lots. Features are what tenants will look into before signing the rental agreement. Assuming the property is in good condition, features will have a major impact on the rental rate and eventually on the investor’s cash flow. The good thing is that those features enable investors to easily compare both the purchase price and the rent with other properties on a like for like basis.

Amenities relate to the pleasantness or attractiveness of a property. They are the features of a property that provide comfort, convenience, or pleasure. Examples are a fireplace, central air-conditioning, a terrace, a view, a swimming pool, or a complimentary access to the community gym. Such amenities could be the competitive advantage that differentiates your property from others with similar features, and as a result, may justify higher rental rates.

In the ideal scenario for the employee millionaire, given that each has a job and limited time to spend on repairing a property, investors want to find discounted properties that require no repair. Properties in good condition can be listed for rent from day one, which means your invested capital will start to generate returns as fast as they get rented out. On the other hand, many properties require minor cosmetic repair, causing a large discount from market price. Those fixer-uppers represent opportunities with discounted prices, which can have a big impact on the return on invested capital. An investor should have a good understanding of both the estimated cost of repair and the estimated time of repair before deciding whether a fixer-upper will be a good or a bad investment choice.

All those investment criteria could be grouped into one template that will allow you to compare properties based on a definite set of criteria.You can download a free copy of this template here.3. Not Running the NumbersAnother common pitfall of buying an investment property to rent is basing your investment decisions on emotions and guessing rather than numbers. As a beginner real estate investor, you should resist the temptation of becoming emotionally attached to a house. You should do a rental property analysis to make sure that buying the property makes financial sense.

“Numbers don’t lie. It’s better to miss a good deal than buy a bad deal. Conversely, do not walk away from a good deal.”

Consider investment properties for sale that will generate positive cash flow and the best return on investment. The Employee Millionaire Rental Properties Price Evaluator is the best real estate investment tool for performing investment property analysis. With this tool, you will be able to avoid buying rental property that would end up being a money pit.

Download Your Free Copy of The Rental Properties Price Evaluator

4. Failing to Perform Due DiligenceDue diligence is about doing a thorough physical and document inspection of a property to make sure it’s a good fit to be part of your property portfolio. Think of it like a major checkpoint done more professionally to double check the property’s title, its physical condition, and documents related to its rent and operations.

Three different types of inspection during due diligence go hand in hand simultaneously:Physical inspectionDocument inspectionFinancial inspectionPhysical InspectionThe physical inspection of a rental property is about uncovering things that may become a problem in the future. Those potential problems may have major financial implications on the buyer, which could be avoided if discovered before the final commitment. Any major foreseen expense can be brought on the table in the negotiation process.

At that stage, even before you have submitted your letter of intent to the seller, you should have walked through the property. Likely your eyes are not trained like those of a professional inspector, who can reveal problems that are hidden below the nicely-painted walls.

As an investor, the inspection report can help you identify potential problems or upgrades related to safety and fire, roof, structural integrity, electrical system, plumbing system, HVAC systems, walls cracks, and potential environmental hazards.

A typical report will include all the areas covered in this section, with photos to illustrate the finding, and a professional opinion whether each problem is a safety issue, major defect, or minor defect. The report also determines which items need replacement and which should be repaired or serviced. This makes it easier to determine the cost of repair and maintenance by asking a few contractors to quote for the job.

Once physical inspection is completed, the buyer usually goes back to the seller and either gets more clarity on some of these items, asks for certain things to be remediated, negotiates for a discount, or in case of structural and other major problems, walks away from the deal.

The golden number that will be part of the inspection report is the appraised market value of the property, which is one of the major requirements by the lender to ensure that the property is worth more than the mortgage amount to be lent to the borrower.Document InspectionThis is one the most straightforward parts of due diligence. In the inspection clause of the letter of intent, the buyer usually requests specific documents to be reviewed. The most common documents include a copy the title deed of the property, copies of rental agreements, a recent real estate tax bill, a copy of the insurance policy, existing service agreements, HoA or master developer rules & regulations, and copies of receipts of repair and maintenance done on the property. Document review should not take more than a day or two to be accomplished once the documents have been received by the buyer.Financial InspectionWhen you analysed the property’s rental income and operational expenses to compute its NOI (net operating income), many of the numbers were forecast to the best of the buyer’s knowledge based on the available information and based on some common industry practices. The financial inspection part of the due diligence allows a thorough financial analysis based on the real numbers before the final commitment and signing the purchase and sale agreement. If the numbers still add up and the real picture is similar to or better than the forecast one, the buyer can move on with the deal.

In essence, a financial inspection allows the buyer to validate all the numbers, from rental income to operational expenses, which were previously shared by the seller or their agent.Rental income reviewProperty/Real Estate taxesProperty insuranceProperty utilitiesMaster community feesProperty management feesProperty maintenance and capital expenses

5. Getting the Wrong FinancingInvesting in rental properties for beginners is usually a challenge due to a lack of capital to fund those properties. Very few people can actually afford to buy investment properties with cash; and therefore, investors usually resort to property loans, which is an integral part in owning a portfolio of properties.

The caveat is very few beginners research the different financing options available and run the numbers to see whether the investment property will product positive cash flow or the investor will be struggling to keep up with the loan installments.

Related: Decoding The Process of Financing Your Real Estate Investment

The Bottom Line - Follow A Proven ProcessIf done right, investing in rental properties can be one of the smartest financial decisions you'll ever make in your life. Such an investment vehicle both pays you passive income (from the rent) and builds wealth, so that you can start planning for your retirement.

There are several pitfalls that can derail your career in real estate investing before it starts. You ought to be aware of these pitfalls ahead of time and follow a proven process to avoid them. By avoiding the common real estate mistakes, you’ll be able to maximize your return on investment.

July 8, 2020

9 Simple Hacks That Will Help You Reach Financial Freedom

Don’t you just wonder what it would be like to have enough:

Money to buy what you want when you need it?Time to spend it with your family, beloved ones, and friends, or just travel the world?Choices in life to stay in a job or career that fulfills you or just leave a boring nine-to-five job that you dread?Well, you are not alone in this. One thing we all have in common is our desire to be financially independent, but the most important is your reasons why you need to have enough money.

Very few people realize that money is only an enabler for you to have the non-money related things you want in life – your “Big Why” list.

Read related article: What is Your "Big Why"?

Having enough money in your account does not mean you have attained financial freedom. You could have a million dollar in your bank account, and yet not be financially independent. What you need to focus on is having multiple streams of income, not from your job, that are in excess of your expenses, while maintaining your current lifestyle, to become financially independent.

Financial freedom sounds like a far fetched theory, but anyone can achieve it, with the right habits and mindset. Regardless of the financial trouble you may have today, with the right financial habits you can live a stress-free life and improve your personal finances.

What Does Financial Freedom Really Mean?Financial freedom is simply the degree to which your finances enables you to live your life the way you want it. Financial freedom goes beyond just having money. It is the independence to take ownership of your finances and afford the lifestyle you want, without the need to work for money. This is the state where your money works for you and earn you Unearned Income for every month for the rest of your life. This kind of wealth can also be passed on to your children.

Financial freedom is not a destination but a journey. It is often difficult to spend less when there are all forms of temptations and distractions around you. However, when you actively plan for your long-term financial situation by making smart money decisions daily, you’ll get closer to financial freedom. Although several issues may try to thwart your effort, including having financial emergencies, paying off bad debts, and retirement plan, among several others. However, that is not the end of the journey, but a progression.

There is no “one size fit all” to financial freedom. If that is what you are looking for, then I’m afraid you’ll keep searching for the impossible. What Mr. A needs may be totally different from what Mrs. B needs. There simply isn’t a single approach to financial freedom. What you need to know is that you have a choice, and that choice can make or mar your financial freedom.

How to Achieve Financial Freedom: The 10-Step FormulaAdopting the following 10 habits will help you accumulate more wealth, live a stress-free life and ultimately achieve the financial freedom you need.

1- Having a Positive Money Mindset HelpsDebt, specifically bad debt, can be disheartening. Research has shown that people feel ashamed when they don’t make enough money, while at the same time are drowned in piles of debt and bills.

Sometimes when you can’t make head or tail about such a financial situation, but having a positive money mindset about money may just be what you need to get you started. Your healthy mindset would motivate to you to take proactive steps in fixing your financial challenges.

You can’t make the right decisions about your finances and money if your emotions are all over the place. Having a positive money mindset is like one of those strong main pillars to accumulating wealth. Remember that money is good if it's put to work for the things that matter in your life - your "Big Why" list.

Change that notion that money is evil. Money is just an enabler to get the things you want and need. That's it! We make it good or evil, depending on what we do with that money.

Cultivate the habit of believing and getting thrilled about being wealthy. Improve your financial education and learn more about how to better invest your time and money for wealthy return on investment. That way, you will start to identify those opportunities, which has always been there but not visible to you.

2- Set GoalsMoney becomes meaningless when you don’t understand your motivation for wanting it.

Ask yourself these questions, “Why do I want to make money?” “Do I want to get rid of debts? “Are you saving for a major event like a wedding, a house, or a retirement? Do you simply want to be your own boss and escape the nine-to-five routine? Do you want to go for a vacation alone or with your family?

Having a general desire to make money is not enough. You need to set financial goals. Write down your goals and review them often to monitor your progress. The more specific your financial goals are, the easier it is to achieve them. You may not achieve all you want but you’ll get to cross off a lot from your list.

3- Have an Extra Source of IncomeHere is a free eBook that gets you started on setting your financial objectives.

If you really want to have the freedom to spend money the way you want, then your nine-to-five job may not be enough. You need to find additional sources of income. You can either turn that hobby into a profitable business or start investing your money to make it work for you.

You need to create multiple streams of income to an extent that the accumulated passive income will carry all your expenses while maintaining your current lifestyle.

Note that trading your time for money is not the ideal solution. This cannot be scalable. You need streams of income that pay you passive income and that keep on building your wealth. Investing in rental property is one of the most solid assets that pay you passive income and grow your wealth.

4- Stop That Consumer MindsetWe all have different triggers for spending more than we need. Some people spend more money after a breakup, some spend more when they are sad, while others spend money when they think they have just enough in their accounts. Understanding your emotional triggers and controlling them will help you curb unnecessary spending.

In the early stages of building wealth, you need to limit the unnecessary expenses, the discretionary spending. In that way, you spend on the essential expenses, and the saved money will be put in a separate account that will be used for investing later on.

Withdrawing cash before you go shopping can also help curb your spending. It is very difficult to walk away from a full store with several products that you think you need when you have your credit cards and other forms of payments. However, when you go shopping with just enough cash, you only buy what is on your list or the vital items.

5- Be Financially LiterateFinancial literacy is the knowledge, information, understanding, or training you acquire and use on the most successful and effective money practices. Financial literacy is crucial not just for organizations but for individuals as well. For you to make wise money decisions you must be able to effectively understand taxes, personal finances, comprehend the notion of debt management and budgeting, and know how to make your money work hard for you.

So keep yourself up-to-date about financial news, tax laws, and developments in the stock market, and make appropriate changes to your investment portfolio where necessary. Financial knowledge is key to attaining financial freedom and avoiding people who exploit ignorant investors.

6- Invest in Income-Producing AssetsYou don’t need to accumulate a staggering amount of wealth before you can invest. Regardless of the amount you earn, you can always find a suitable investment. Your money can only work for you when you invest it in assets that pay you passive income.

Learn to also invest in yourself and in your financial education. Listen to financial audio books, purchase relevant investing courses, and read books on financial management and investing.

You should also invest in your future by setting aside money for emergencies. You can have emergency funds, have a retirement plan, and other investments. By having these funds set aside, you’ll be less likely to fall back into financial problems.

7- Do Not Misuse Your Credit CardsIf you think adding just about anything to your credit card is not an expensive habit, then you are absolutely wrong. It can be costly when you don’t pay off your debts when they are due. Don’t spend the money you don’t have. Learn to automate your payments, so you don’t end up paying ridiculous amounts of interests on your credit cards. When you automate your payments you avoid debts and avoid spending it on something less important.

The psychological implications of misusing your credit cards are endless. For one, your credit score can determine if you’ll get a car insurance, life insurance premiums, or even a job. The perception is that a person who is irresponsible with his/her finances would likely be irresponsible in other areas of his life. You see why you cannot afford to be reckless in your spending. Ensure you get consistent credit card report to avoid tarnishing your reputation.

8- Have a Budget and Monitor Your ExpensesThis point is closely related to the goal setting formula. Set a budget for your monthly household expenses and stick to it religiously. This way you can ensure that all your bills are paid on time and your savings are on the right track. Having a budget would restrain you from overspending and you’ll achieve your goals easily.

You can monitor your expenses automated tools that would help you keep track of how much you’ve spent, what you’ve spent your money on, how much you have left, and even how much you owe. With these tools you can monitor your goals and know how close you are to achieving them. It can be dangerous to spend money without having something that serves as a check-and-balance to control your expenses.

9- Seek Financial Advice

The last but most certainly not the least step to take is to get the right financial advice. You need a capable and credible financial advisor or a coach to help you fix your personal finances, invest in income-producing assets, and grow your wealth. He/she would be there to enlighten and coach you on how to make certain decisions that may affect your financial freedom.

Finally

Reaching the point where your finances do not influence your decisions is not an easy process, when you have debts to pay, medical bills and other bills, and emergency situations, among others. However, financial freedom can be reached through cultivating the right financial attitudes and habits and carefully planning how to achieve your financial dreams.

Discover More...

June 28, 2020

Should You Buy An Investment Property With Cash Or Mortgage?

When purchasing rental property for investment purposes, there are two schools of thought. Most investors would benefit from leverage and would opt to purchase properties through a mortgage loan; whereas, some other investors still prefer to purchase their investment property on all cash basis.

For those investors who would choose to finance their rental property purchases through a mortgage or a loan, not all of them would prefer the highest possible loan to value (LTV), so that they pay as little from their own capital. There are many investors who would prefer a 50% LTV over the standard 75 - 80% LTV or the maximum LTV of 100%.

Which financing option is the right one? Well, there is not correct or wrong answer... the sweet spot varies by investor, depending on their objectives, which could be cash flow or a high return on investment.

Financing a Property on an All-Cash BasisThe topic of purchasing a rental property on all-cash basis appears as counter-intuitive to the benefits of leverage and investing for maximum returns.

All-cash basis is only a term used for purchasing a property out of the buyer’s own funds. In reality, there is no cash money being traded. All the transactions take place in the form of checks or bank wire transfers.Reasons for Buying Rental Properties on All-Cash BasisThe most common reasons to purchase rental properties on an all-cash basis, if the person can afford it, are:Avoiding risk of defaulting on mortgage instalments, which could lead to the lender foreclosing on the property. Investors of that type are risk averse and think that although they have cash now, they are not sure what the future might hold for them.Investing for a higher cash flow, which means for a higher unearned income. For those investors, all that matters is how much net cash they receive per month. They understand that this high amount of net cash flow could not be the best ROI for their money, but they are quite happy with this equation. For them this could be their retirement plan, where fewer rental properties could secure them unearned income for life and without the risk or hassle of having a mortgage. For those investors, buying on all-cash basis is the right choice.Paying all cash is a step before owning the property with no or little cash later. This could be a short-term approach for investors who have the cash before financing through a mortgage loan at a later stage. This strategy will result in the investor owning a property with zero or little down payment from his or her own pocket. Discover more about how it can be done and how an investor could access the required cash to do so on The Employee Millionaire program.

Drawbacks of Purchasing on an All-Cash BasisPurchasing a property for cash only can have its advantages from a high cash flow perspective and more peace of mind from not owing any money to any lender, but it also has its own drawbacks. Although I love leverage in the form of good debt, I am not trying to convince you to use it. But I owe it to you to share some of the drawbacks of purchasing a property on all-cash basis.Reduced return on invested capital.Fewer properties that can be purchased.Increased risk of litigation by other non-well-meaning individuals who are just greedy and looking for prey with enough fat. Owning a property free and clear is a sign that the landlord has too much fat, and this makes litigators open their eyes wide for a hefty prey.Getting a Mortgage LoanConventional loans are the most common standard loans that can be obtained from a bank or a mortgage broker. Getting a mortgage loan on a rental property is no different from getting a loan on a primary residence. Such loans do enjoy low and favourable interest rates, which makes them the most attractive types of loans.

As a lender that wishes to manage risks associated with a mortgage loan, the bank will ask the borrower to put a sizable down payment of 20 to 25% of the appraised market value of the property. In turn, the bank will lend out the balance of 75 to 80% of the property value to the borrower. This ratio of the loan to the value of the property is commonly referred to as loan-to-value (LTV).

Their main advantages are:Most competitive interest rates among loan types.Long terms of up to twenty-five or thirty years on residential properties.Watch-outs:Conventional lenders might set a cap on the number of mortgage loans a borrower can have.The central bank could set a cap on the number of mortgage loans a borrower can have.The loan-to-value (LTV) might go down with an increasing number of mortgage loans.Even if the borrower qualifies for a loan, the bank can disapprove a property due to its condition.

If you need to find which strategy is best for you and how to go step by step for the strategy that's a great fit for you, head over the The Employee Millionaire and start paving your way to building wealth.

May 11, 2020

Why You Might Get Hit By Recession, If You Buy Real Estate On The Promise of "Price Appreciation"

Almost everyone of us have heard of stories from our parents or other senior family members about how their home is now worth five times more the original purchase price from fifteen years back. Without using any technical jargon, they are simply referring to price appreciation, which is the increase in the value of an asset over time.

Those kind of stories gave insights to property developers and their real estate agents to push the sales of their properties with the promise of capital gain - which is another technical jargon used to describe the rise in the value of an asset (such as real estate) that gives it a higher worth than the purchase price.

Most major cities around the world have witnessed sales pitches with promises of buying properties off-plan and then enjoy capital gains with 30%, 50%, 100%, and even whopping 300%.

Many inexperienced investors have fallen in this trap of the false promise of a guaranteed price appreciation, for the simple reason they only looked at the long term numbers... which in a way is true, since the long term masks the ups and downs of the short term. They simply thought everything goes up in a straight line!

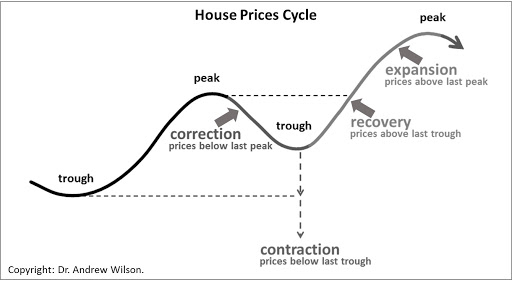

The long-term increase of house prices over time is often referred to as natural appreciation. Although the overall direction has always been up in the recorded history of property prices, prices might go up and down in the short term. The reality is that property prices never go up in straight line ... and it's here where most investors lose their shirt!

The price cycle of properties is well presented by Dr. Andrew Wilson, one of Australia’s leading housing market experts, in the figure above. In principle, the house price cycle is typically depicted in four stages:a boom (peak),followed by a downturn (correction),followed by a recovery phase,which leads to an upturn (expansion) that sets us up for the next boom (a higher peak).

This house price cycle explains why it is risky to purchase a property on the promise of appreciation and with the objective of flipping the property in a few weeks, months, or years. Markets always go in up and down cycles on the short term, which could make an investor wanting to flip houses lose money if the cycle was going downward in a correction phase.

This is the simple reason why you shall look at appreciation as the cherry on top of the cake, whereas cash flow is the cake itself. Check out this related article on how investors can avoid losing it all to the false promises of capital gain. It also discusses risk management in rental property investing.

The caveat when prices go up is that all this price appreciation or capital gain is only realized when the asset is sold, which means this is only paper gain (or unrealized gain). The same applies when prices go down and the investor does not sell the property - it's paper loss.

By the way, our Employee Millionaire Course covers the mistakes real estate investors make that causes them to take months or years to get started or to fail after starting. This course will cover the insider secrets, so you can complete your first rental property investment in just few weeks and with little starting capital.

The magic of investing in real estate is that you can force the asset to appreciate. This concept is called "forced appreciation", which is increasing a property’s value by improving it such as by converting free, unused space in a home into an additional bedroom or bathroom. This strategy is used often by investors who make profit by improving houses and flipping them. This strategy might work well for some, but it is not the strategy that someone with a full day job willseek in building wealth and achieving financial freedom through rental properties, since this strategy requires a lot of time—and time is a scarce resource for employed investors.

April 17, 2020

How Not To Lose Money With Rental Properties During An Economic Downturn

Regardless of your level of experience in real estate, weathering a financial downturn can be a challenging task. As an investor in rental properties, you will need to protect the positive cash flow from the rent by keeping the rent steadily coming in, while controlling your operational expenses.

During economic downturns, like the one the world faced with the COVID-19 epidemic, cash money becomes scarce and the pool of buyers dwindles. This decrease in demand brings the price of real estate down a roller coaster. This is when you start reading and hearing about the term " distressed sale " in your community.

Here is the catch! Is this a good or bad situation for real estate investors?

My experience from the 2008 global financial crisis taught me that great deals are found when the economy is going down. This is where you will find great deals at huge discount. Look at it like going to the mall and everything is for sale!

But, I am not saying that there are no potential pitfalls that can make current real estate investors (who previously bought their properties at higher price tags) lose money if they don't follow sound investment strategies... which we will cover in this article.

Big Opportunities For Investors Who Will Buy Distressed Deals!Before we cover how existing investors can protect their money and their profit during a financial crisis, I can't stress enough the huge opportunities such distressed deals can bring to investors who will buy properties at rock-bottom prices. This strategy follows the principle of going in when everyone else is going out.

Implementing sound real estate investment strategies during an economic downturn pays off handsomely for those who will buy distressed houses with cheap leverage, and then rent those properties out at a rate that covers all expenses (including loan installments).

Let's dive a bit deeper into this scenario...

During an economic crisis, there are very few buyers out there (those are usually the investors).This makes the prices of real estate tank.In parallel, central banks wanting to boost their economies will start offering very cheap loans (at very low interest rates).This is when the real estate investors get warmed up, open their eyes, and get pumped up to scoop real estate at reduced prices and at very cheap mortgage rates. They think of it like paying pennies for the dollar!When few people are buying properties, the demand for rent will increase. This means, those investors will not find it hard to rent those properties and start earning from the rent.The next question on your mind would be: wouldn't rental rates be affected during an economic crisis?

The short answer is "yes"... and this is what stops most people from investing in rental properties, whereas (at the same time) professional real estate investors will be jumping in.

The more appropriate answer is that rentals do tend to come down when the economy goes down, but remember those investors are buying at the current market condition (where both property prices and rental income are down). So, this means they will do the math and determine their returns based on this market reality of low rent and low market price. If the numbers tally, then they will jump in and invest in rental properties that shall pay them handsome returns.

Now that we've covered the positive upside for real estate investors who will invest in properties during an economic downturn, it's time to cover the potential downside for those investors who already own properties already purchased at higher prices.

How to Avoid Losing Money During a DownturnAs the economy continues to suffer during a pandemic or any other financial crisis, investors must hunker down and prepare for potential pitfalls. This is how investors manage risk and avoid losing money in real estate and weather potential recessions.

Let's discuss the steps that rental property investors should take to avoid significant financial loss during a crisis.

As of the writing of this article, while the corona virus is still spreading across the globe, a housing market crash is a very likely possibility. Most economists and analysts predict an economic downturn with effects that will likely echo across a wide range of sectors, the property market included. Any smart real estate investor should prepare for such a crisis.

So how can rental property owners avoid losing money in this uncertain and fluid climate? Here are some effective approaches that you should know about.

1- Don’t Panic and SellIn its efforts to protect us, our mind tends to make us panic and make wrong decisions when it comes to our investments. Earlier in this article we've covered how investors can take opportunities of distressed sales and make a handsome profit. In the case of investors (who own property previously purchased at a higher price) might be tempted to panic sell and lose a large equity in their holdings.

In fact, it is quite common that certain real estate investors might panic when the value of their property falls. This short-sighted reaction often results in losing out on a prime property that is still capable of generating positive cash flow.

Don't fix what is not broken! ... as long as your investment property is still earning rental income, there is no reason to offload it during a financial crisis.

2- Be Prepared To Make Flexible Rent Payments With Your TenantsA financial crisis does not differentiate between a landlord and a tenant. You can bet that both the tenant and the landlord are affected by a crisis.

This is why you must take the financial challenges your tenant might be facing into consideration during crisis. Guess what! by your helping your tenant not default on their rent payment, you are actually helping yourself by not losing money.

If you refuse to renegotiate the lease or the payment terms, you might end up with a vacant property at a time when liquidity is dry. This means you might be forced to accept much lower rent rate with new tenants to avoid having a vacant unit for a long time.

My advice is to try to find a middle win-win ground with your tenant and settle on a rental rate or a rent deferral plan that is fair for both parties.

Now, with this advice of being flexible with your tenants, you might be thinking on how you will be able to still cover to pay the loan installments. This is what we will cover below.

3- Renegotiate Your Mortgage Rates And Terms With Your LenderWhen countries are on the brink of an economic crisis, the usual first reaction by their central banks is to attempt to rescue the economy with quantitative easing. In turn, banks and lenders will offer loans at very low rates and flexible terms.

All what you need to do is approach your current lender and request for a revision of the interest rate on your existing mortgage loans. The chances are in your favor that they will revise down those rates, so that there is no potential scenario of the borrower failing to pay off those installments, which might lead to the bank repossessing a property they don't want on their books.

My advice is to request for a meeting with your mortgage broker or lender, and they will find creative solutions to lower your monthly debt payback. One of those possibilities could be another lender buying off your existing loan and lending you at more favorable terms.

4- Stick To Your Budgeted Operational ExpensesWe've covered so far strategies that will keep you earning rental income and lowering your debt repayment. What about those operational expenses related to the property itself?

Although a professional rental property investor will have a budget and a plan for those operational cost, it pays off to to take a conservative approach and tightly control those expenses.

A wise approach would be to operate on the assumption that the crisis will last a bit longer than what most experts are predicting and determine if those operating expenses are still manageable throughout that period.

If the answer is no, then you should consider cutting or deferring some costs. Here are some solutions to manage your expenses on a tight budget:

Negotiate the service charges or HoA charges imposed by the developer. During crisis, most developers will be sensible about the personal finances of the landlords and will be flexible on a combination of charges reduction or payments deferrals.Get competitive bidding on the urgent maintenance and repair expenses. Contractors out there are also hungry for business and will be more competitive to sign off a deal.Defer those preventive maintenance activities that will not have any impact on the property's condition for the short term. Once the crisis is over or your cash flow can manage such preventive maintenance, then you can have them performed on the property.

5- Convert Your Short Term Rental Property Into Longer Term At Competitive RateShort term rentals are the most affected types of rental properties during a crisis. While this is generally true in any type of economic downturn, the impact has been especially exacerbated during the corona virus pandemic given the lock down measures that most countries have imposed on its citizens and residents.

A quick fix would be to convert your short term lease agreement into a long term rental. You have to be aware that this will mean lower rental rate on a daily, weekly, or monthly basis; however, the income will be steady on a longer term (usually at least one year).

In SummaryLosing money during a crisis is not a given or a certainty. In fact, you can avoid losing money if you properly prepare for it by implementing the simple an actionable strategies outlined in this article.

In the meantime, you can check out my award-winning best-selling program on rental properties by clicking here.

Discover More

April 12, 2020

January 20, 2020

Don't Get Pulled Down By The Crabs ... Jump And Join The Group of Salmons!

Did you ever hear of the Crab Mentality? This idea of the crab mentality is best explained by the phrase: "if I can't have it, neither can you".

The comparison is derived from a pattern of behavior observed in crabs when they are trapped in a bucket. So, while any one crab could easily escape, its efforts will be weakened by others that are pulling it down - ensuring the group's collective failure.

The analogy in human behavior is that members of a group will attempt to reduce the self-confidence of any member who achieves success beyond the others. This could be done out of envy, resentment, nastiness, conspiracy, or competitive feelings to delay their progress.

The thing is that you don’t want to spend too much time around people who will question every investment or entrepreneurial opportunity you may want to take. It could be with all good intentions, and due to their own limited experience and knowledge, they will most probably scare you off to the extent that you will lose energy and hit the brakes leaving the road of financial freedom and making a U-turn towards the old you.

So, you need to detect the crabs in your circle of friends and make sure to stay out of the bucket where they sit getting busy pulling others down towards them.

This simple move of staying out of the Crabs Buckets will allow you to restore your mindset back to a positive and effective state.

Then you need to join this active group of Salmon Fish all swimming upstream against the water flow. with all determination, incentive, and motives until they reach where they want to be.

So, if you think how this can relate to you, one of the best ways to develop a positive mindset is by carefully choosing who you spend your time with.

If you are really determined to become rich and achieve financial freedom, you will need to cultivate friendships with successful people who seek out and talk about opportunities. The more time you spend with those people, the more you will learn from them about how to achieve your financial goals.

Being in the company of positive and like-minded individuals is crucial. Spending time with positive people will boost your energy, esteem and happiness.

I am neither suggesting that you select your friends for their income level or investment acumen nor to lose friends who have selected the route of poverty. In fact, I have friends from both extremes, and each one of them teaches me different lessons.

What I am opening your eyes to is to select with who you wanna spend most of your time with with who do you want to rub shoulders and from who do you want to learn.

This association tactic of going out of the crabs bucket and Joining the group of salmons is easier said than done. It's not an easy thing to face facts about a friend, family member, long-time colleague, but knowing who is pulling you down and limiting your time in their presence is the first crucial step you must take and you will be feeling the positive vibe immediately!

Now you might be wondering about how to detect the crabs around you. Those crabs could be a friend you have known forever, a person who you know through another friend, or a person who you see all the time in a specific area of your life.

No matter how close or far this type of friendship is, I tell you it’s not going to be easy for you spend less time with them. You are going to feel guilty brushing them off because you are used to seeing them all the time.

Here are some questions that will help you detect who those crabs in your circles of friends are:

Do you feel you constantly have to fix this person’s problems?Do you feel you are covering up or hiding for them? Do you feel you dread seeing them? Do you feel you feel drained after being with them? Do you feel you get angry, sad or depressed when you are around them? Do you feel that they cause you to gossip or be mean? Do you feel you feel you have to impress them? Do you feel you’re affected by their problems?

Now grab your note book because I would like you to write down all your friends, and people you interact with constantly. After you finish, take each of them through this set of questions and you will easily find out who is a crab and who is a salmon … who to spend less time with and who to spend more time with and learn from.

Discover More About Millionaire Empowering Beliefs

December 31, 2019

Motivated Money Mindset That Helps

The truth is everyone struggles with one financial challenge or the other. Regardless of how little you earn or how huge your income is, no one is above a financial challenge. The way you train your mind to react to financial situation is very significant.

However, most people attempt to tackle their financial situations in a severely logical manner and get so hard on themselves when savings and budgeting efforts fail. Without a doubt, when dealing with financial struggles it often comes down to numbers, yet applying certain habits and behavioral patterns to backup those mathematical solutions necessitates that we look at other factors that shape our financial lives, including our emotions, point of view, and the overall illogicality that combine together to make us human.

Experiencing a financial challenge can be quite frustrating particularly if you've been battling with the same issue over and again. So, you need to change your money mindset from a poverty-driven mindset to an abundance-driven mindset. This is not so difficult to achieve if you know just what to do. If you’ve been struggling financially, below are some tested formula which you can implement to tackle your financial situation and bounce back financially.

Money Mindset definition Your money mindset is the prevailing attitude you have regarding your finances, which motivates your key financial decisions on a daily-basis. Simply, money mindset is our unique attitudes and perspectives about money and ourselves. The mindset we have about money affect our money relationship and the outcomes we realize. The reason is that, the way we think about a thing informs how we interact with that thing and the type of actions we take concerning it.

Why it is Important to Have a Positive Money Mindset? The way we view money shapes our attitude towards others, whether they are poor or rich. For instance, if you believe that rich people are evil, materialistic, greedy, pompous, and awfully mean, so you don’t want to associate with them. Then this will affect your ability to make money. Similarly, if you believe that being poor makes you virtuous and noble, so you like poor people. This will hinder your ability and motivation to make money.

Why it is Important to Have a Positive Money Mindset? The way we view money shapes our attitude towards others, whether they are poor or rich. For instance, if you believe that rich people are evil, materialistic, greedy, pompous, and awfully mean, so you don’t want to associate with them. Then this will affect your ability to make money. Similarly, if you believe that being poor makes you virtuous and noble, so you like poor people. This will hinder your ability and motivation to make money.Your responses and reactions during financial conversations indicate your money mindset. Do you believe that only the male population should make money? Do you feel confident and in control or do you feel vulnerable and uncomfortable when having a financial discussion?

The human mind is powerful and when used in the right way, it compels certain things to change in our lives. If you are able to adopt a positive money mindset, you are more likely to make better decisions about how to deal with your struggle. According to Fitz Gilbert, we are what we think and having the right attitude towards our finances, will have a positive and direct impact on our financial situations and how we overcome those challenges.

What Shapes Your Money Mindset? Did you grow up around money? Were you told that money is evil and cannot buy happiness? Did your parents make snide remarks about rich people? Were you told that you cannot do better than your predecessors financially?

What Shapes Your Money Mindset? Did you grow up around money? Were you told that money is evil and cannot buy happiness? Did your parents make snide remarks about rich people? Were you told that you cannot do better than your predecessors financially? Most of our mindset about money is usually formed during our early childhood while interacting with money. Our social and family background have great influences on the way we view money. The people we associate with influence our money mindset, including our friends, parents, family, colleagues, and neighbors. Our environment is another factor that influences our perspective about our money, such as school, house, office, and other social environment.Tips to Help You Adopt a Motivated Money Mindset The following are some proven steps that can help you adopt a motivated and positive money mindset, and the good thing is they are quite easy to implement. Understand What Money Means to You The first question to ask yourself is: why do I want to make money? Knowing your motivation for wanting to make money can help your financial situation. Are you afraid of being broke? Do you want to make money to climb up the social ladder? You need to assess what motivates your money decisions, is it fear that if you don’t save more you’ll go broke? Or are you inspired by the rewards that come with making money?

Several factors aside just thinking about money increases cash flow both into your bank account and your hands. You must understand what money means to you to combat your financial situation. You need to milk whatever inspires you to make money, that way, you can be reinforced to keep pursuing your financial aspirations.

Recognize That No Financial Challenge is Unfixable Recognize that there is no insurmountable hurdle anywhere. Every financial challenge has a solution. That you haven’t figured it out yet, does not mean the solution is not out yet does not mean you won’t eventually.

Stop focusing on the enormity of the challenge or what’s wrong, else you won’t be motivated to seek out solutions. Instead start focusing on the benefits of attaining financial independence, living a stress-free life, accumulating more wealth, and how you can spend your money on things that you need, want, or towards a bigger purpose of helping people around you and the community you live in. It’s so much easier to stay motivated and achieve all your financial goals, when you maintain a positive outlook.Change Your Money Outlook It is easy to feel down and depressed when everything is not going the way you want it to. Be positive that everything will work out and keep on trying. Accept that the small steps you’ve taken thus far adds up to the progress. You are solely responsible for your reactions. Having a positive money mindset will help you be more productive and develop a better relationship with money.

Sometimes what you need is a break to refuel when you can’t make head or tail of your finances. Worry has yet to change any situation. You may have to go out with your friends or loved ones, go to the cinema or something.You Don’t Have To Do It Alone You don’t have to go at it alone. Understand that asking for help does not mean you’re weak or a failure. Ask for and accept assistance from others rather than struggling silently.

Seek the help of mentors and coaches, read books and blogs focused on financial education, listen to audio books, attend master classes, and get online courses.

A change of attitude isn’t all that’s required to change your financial situation. You also need to achieve balance in your financial life. If all you think about is how to live a stress-free life, you may not have savings to fall back on in case of emergency situations. Neither will you have an effective retirement cushion if you spend all of your time focused on your budget today. So strive for balance to achieve financial stability.Discover More

November 13, 2019

Are You On Top Of Your Game? Or Sinking Like The Titanic?

Do you believe that you can become a Millionaire without leaving your day job?

What does it take to become successful?

Let me share with you an example that everyone knows about…

I think everyone remembers the disaster that happened in the early morning of 15 April 1912, right?

Well, if not let me refresh your memory guys, on that morning a new page of dark history has been written, and that was THE SINKING OF THE TITANIC.

This resulted in the deaths of more than 1,500 people…I get goosebumps when I think and write about this…

That means lost dreams, lost opportunities, the complete silence of death and nothing else!

The sad reality is that some of them were young, some of them were parents, some of them were children, and some of them had just started out in life...

This might sound bad or outrageous but today’s society looks exactly like the Titanic…

Let me explain why…

In today’s society, people don’t follow their dreams, they don’t want to make a change in the world anymore, they spend their time procrastinating and complaining all the time about everything and everyone, they don’t look for solutions anymore because they have too many “good” excuses to use.

If you take a closer look at them you will realize that they are drowning in piles of debt and bills, credit card debt, personal loans, student loans… exactly like the Titanic sank in the cold waters of the Atlantic Ocean.

But at the same time, they want to live amazing lives and do extraordinary things…

My question is…WHEN???

Time is your worst enemy and your best friend, don't forget that time won’t ever come back again…

It’s your decision whether you start living the life you want and provide for your children a better future...YOU DECIDE if you want to become a Titanic or you will start living the life you were created to live!

Don't forget, the graveyard awaits you in case you forgot…

You might feel like you need a miracle in your life right now…

YOU DON'T NEED MIRACLES... you're alive and that's the biggest miracle you can ever get, now get to work, because dreams won't become reality without taking action!

Yes, yes …I know… you would like to start but you don’t how, where, you don’t have a plan and you’re confused, you want to take action but that feeling of “I DON’T KNOW HOW” makes you feel anxious and nervous, right?

WHAT IF I would tell you that you will have everything you need to start, everything from A to Z so you can easily follow…would you start taking action or you would still be a sinking Titanic?

I know what you need because I've been there many times.Click here to discover how...

I will prove to you that you can become wealthy even if:YOU HAVE A DAY JOB (I also had a job, having a job is good in the process)YOU ARE DEALING WITH FEAR OF FAILURE (I was also paralyzed by fear but this happened because I didn’t had any support)YOU HAVE ZERO KNOWLEDGE (I didn’t have any knowledge when I first started)YOU DON’T HAVE A PLAN (I will share with you my step by step action plan)YOU DON’T HAVE TIME (I will teach you how you can use the time you have in the best possible way) I’m going to teach you the exact same process I’ve used to become a millionaire…

Yes, I know that some people out there claim to be successful and that they will share or reveal things that will change people’s lives but it’s never as they say…unfortunately!

I want you to know that my program, my books and all my materials are FOR THE PEOPLE!

I want to help them since I know what it means to be depressed, anxious, frustrated and broke.

It’s not so pleasing to know that your family depends on you and I’m sure that nobody wants after 15 years to look at their children in their eyes and tell them…”I’m sorry for this situation, don’t worry someday it will get better” and at the same time you know inside of you that it’s not going to get better but you can’t tell that to your 15 year old son…

I barely had money to sustain my family and my life was a complete nightmare. It was horrible…I don’t even want to remember those days but at the same time I’m glad that I’ve been through this since this situation pushed me to find solutions and make a change.

Now I can help others achieve financial freedom exactly like I did, I have the process, I have the tools, I have the knowledge, I have everything you need to succeed!

My work captured the attention of major media like… ABC, NBC, FOX, Yahoo Finance, Market Watch, and… The New York Times Book Review… to name a few.

Even the world’s toughest critics love and recommend my content!

I’ve sacrificed 12 years of my life to create this step by step proven process. It was hard to keep digging and face knock downs, sometimes I wanted to quit…but thanks to my wife who always supported me I kept moving forward!

Basically, I’m going to teach you everything I know, everything I used to become a millionaire and the good news is that you will have everything ready to use. Most importantly…YOU WON’T LOSE TIME, like we all know time is the most valuable resource that never comes back and nothing can STOP TIME!

My content and everything I created is for the people! I'm giving everything; I'm not keeping anything secret!

YOU HAVE THE “WHAT”YOU HAVE THE “HOW”YOU HAVE THE “WHERE”YOU HAVE THE “WHEN”.

You decide if you want to escape the rat race and live the life that you’ve always dreamed of OR stay like this and end up like the Titanic…

EXCUSES never helped anyone with anything.

Discover How!