J. Bradford DeLong's Blog, page 2153

November 20, 2010

Joe Klein Has Really Eaten His Wheaties Today

Joe Klein:

Obsessed with the Deficit — and Ignoring the Economic Mess: Why are we spending so much time and effort bloviating about long-term deficits and so little trying to untangle the immediate economic mess that we're in?

Perhaps it isn't a coincidence that so many of the people whinnying the loudest are prominent members of the financial community, the sector that has had the most to do with hollowing out our manufacturing base and creating the Ponzi scheme in housing that caused the 2008 bust. After all that uncreative destruction, they need to polish their high-minded credentials. (See how some Americans are facing the prospect of long-term unemployment.).

There is, for example, Glenn Hubbard, who was featured on the New York Times op-ed page recently in defense of the deficit commission, describing the problem this way: "We have designed entitlements for a welfare state we cannot afford." This is the same Glenn Hubbard who served as George W. Bush's chief economic adviser when Dick Cheney was saying that "Reagan proved deficits don't matter." One imagines that if Hubbard was so concerned about deficits, he might have resigned in protest from an Administration dedicated to creating them. But, no, he's here to speak truth to the powerless — to the middle-class folks whose major asset, their home, was trashed by financial speculators, thereby wrecking their retirement plans and creating the consumer implosion we're now suffering. Hubbard is telling them they now have to take yet another hit, on their old-age pensions and health insurance, for the greater good.

The obsession with long-term deficits is not limited to conservatives. Exuberantly wealthy center-left types who staged a leveraged buyout of the Democratic Party's economic policies in the 1980s — people like the deficit commission's Democratic co-chair, Erskine Bowles — have been reliable foghorns for long-term middle-class sacrifice. They tended to be big supporters of the irresponsible federal lenders Fannie Mae and Freddie Mac, and most egregiously, they shepherded the deregulation of the financial sector through Congress in the late 1990s. But unlike the Republicans, they trend toward fiscal responsibility. Pete Peterson, a nominal Republican who is a leader of this group, is in favor of higher taxes for the wealthy, means testing for Social Security and Medicare, serious cuts in the defense budget — and even a provision that would tax the profits of private-equity moguls as regular income instead of capital gains, a proposal that his former partner at the Blackstone Group, Stephen Schwarzman, compared to Hitler's invasion of Poland in 1939...

Darrell Issa Before Congress

From Wikipedia: Darrell Issa:

Issa was born in Cleveland... describes himself as having been "a rotten young kid." Issa dropped out of high school and at 17 enlisted for a three-year tour in the Army, serving as a bomb disposal technician. Issa further recounted being part of the security entourage for President Nixon during the 1971 World Series, despite Nixon never having attended the event. Issa left the Army nearly two years early after being stripped of his duties as a bomb specialist.

A retired Army sergeant claimed that Issa stole a Dodge sedan from an Army post near Pittsburgh in 1971. The sergeant said he recovered the car after confronting and threatening him. Issa denied the allegation and no charges were filed. In 1972, Issa and his brother allegedly stole a red Maserati sports car from a car dealership in Cleveland. He and his brother were indicted for car theft, but the case was dropped. That same year, Issa was convicted in Michigan for possession of an unregistered gun. He received three months probation and paid a $204 fine.

He attended Kent State University at Stark in North Canton, Ohio and Siena Heights College in Adrian, Michigan, on an ROTC scholarship, earning a bachelor's degree in business administration in 1976. Upon graduation, he was commissioned as an officer in the United States Army, serving as a tank platoon leader and a computer research and development specialist, among other command roles. He left the Army in 1980 with the rank of captain. He later moved to Vista, California, a suburb of San Diego, where he now lives.

On December 28, 1979, Issa and his brother allegedly faked the theft of Issa's Mercedes Benz sedan. Issa and his brother were charged for grand theft auto, but the case was dropped by prosecutors for lack of evidence. Later, Issa and his brother were charged for misdemeanors, but that case was not pursued by prosecutors. Issa accused his brother of stealing the car, and said that the experience with his brother was the reason he went into the car alarm business.

A day after a court order was issued, giving Issa control of automotive alarm company A.C. Custom over an unpaid $60,000 debt, Issa allegedly carried a cardboard box containing a handgun into the office of A.C. Custom executive, Jack Frantz, and told Frantz he was fired. In a 1998 newspaper article, Frantz said Issa had invited him to hold the gun and claimed extensive knowledge of guns and explosives from his Army service. In response, Issa said, "Shots were never fired. ... I don't recall having a gun. I really don't. I don't think I ever pulled a gun on anyone in my life."

Issa made his fortune through his company, Directed Electronics Incorporated, that is most famous for its flagship product, the "Viper" car alarm. It bears a siren that is a recording of Issa's voice saying, "please step away from the car." As of 2004, Directed Electronics was North America's largest aftermarket automotive electronics manufacturer. Issa divested personal interest in Directed Electronics after being elected to public office, but he is the richest member of the House and the second richest in all of the 111th Congress. He is worth an estimated $251 million.

Liveblogging World War II: November 20, 1940

Hungary joins the Axis of Evil:

The Axis Pact between Japan, Germany, and Italy, 1940:

The Governments of Japan, Germany, and Italy consider it as the condition precedent of any lasting peace that all nations in the world be given each its own proper place, have decided to stand by and co-operate with one another in their efforts in Greater East Asia and the regions of Europe respectively wherein it is their prime purpose to establish and maintain a new order of things, calculated to promote the mutual prosperity and welfare of the peoples concerned. It is, furthermore, the desire of the three Governments to extend cooperation to nations in other spheres of the world that are inclined to direct their efforts along lines similar to their own for the purpose of realizing their ultimate object, world peace. Accordingly, the Governments of Japan, Germany and Italy have agreed as follows:

ARTICLE 1. Japan recognizes and respects the leadership of Germany and Italy in the establishment of a new order in Europe.

ARTICLE 2. Germany and Italy recognize and respect the leadership of Japan in the establishment of a new order in Greater East Asia.

ARTICLE 3. Japan, Germany, and Italy agree to cooperate in their efforts on aforesaid lines. They further undertake to assist one another with all political, economic and military means if one of the Contracting Powers is attacked by a Power at present not involved in the European War or in the Japanese-Chinese conflict.

ARTICLE 4. With a view to implementing the present pact, joint technical commissions, to be appointed by the respective Governments of Japan, Germany and Italy, will meet without delay.

ARTICLE 5. Japan, Germany and Italy affirm that the above agreement affects in no way the political status existing at present between each of the three Contracting Powers and Soviet Russia.

ARTICLE 6. The present pact shall become valid immediately upon signature and shall remain in force ten years from the date on which it becomes effective. In due time, before the expiration of said term, the High Contracting Parties shall, at the request of any one of them, enter into negotiations for its renewal.

David Beckworth on Charles Calomiris

With respect to Charles Calomiris's claim that it is inappropriate for the Federal Reserve to aim for a short-term nominal GDP growth rate above 5% per year no matter how high the unemployment rate...

David Beckworth writes:

Macro and Other Market Musings: A Defection from the "Open Letter to Bernanke": Over at FrumForum, Noah Kristula-Green gets some of the Open Letter to Ben Bernanke signers to discuss their motivations for doing so. One of the signers, Charles W. Calomiris, looks like he does not belong on that letter:

There are many reasonable alternative views on how to target monetary policy. I favor Ben McCallum’s proposal to target nominal GDP growth at about 5%. Since we were on track with that target before QE II, at least for the moment, I would neither be raising or lowering interest rates....

If Calomiris believes in level targeting rather than growth rate targeting he definitely does not belong on that letter. Below is a figure showing the level of nominal GDP, its trend, and its forecast through the end of 2011. (Click on figure to enlarge.) The gap between actual and trend nominal GDP in this figure is troubling, but more so is the fact that it is projected to grow over the next year. And yet folks are upset overQE2! Nominal GDP is nothing more than total current dollar spending. This is something the Fed can and should stabilize. That real problem with the Federal Reserve is not that its doing QE2, but that it is failed to stabilize nominal spending in the first place.

But David has the wrong title. Charlie is not a defector from the anti-Bernanke letter. He signed the thing--and he clearly believes not in level-of-nominal-GDP targeting or in a mix but in growth-rate-of-nominal-GDP targeting alone.

God knows why anybody would ever believe that. But he does.

Paul Krugman on the Axis of Depression

Paul Krugman:

Axis of Depression: What do the government of China, the government of Germany and the Republican Party have in common? They’re all trying to bully the Federal Reserve into calling off its efforts to create jobs.... It’s not as if the Fed is doing anything radical. It’s true that the Fed normally conducts monetary policy by buying short-term U.S. government debt, whereas now, under the unhelpful name of “quantitative easing,” it’s buying longer-term debt. (Buying more short-term debt is pointless because the interest rate on that debt is near zero.) But Ben Bernanke, the Fed chairman, had it right when he protested that this is “just monetary policy.” The Fed is trying to reduce interest rates, as it always does when unemployment is high and inflation is low.... So the case for Fed action is overwhelming....

But there are reasonable people — and then there’s the China-Germany-G.O.P. axis of depression.

It’s no mystery why China and Germany are on the warpath.... Both nations are accustomed to running huge trade surpluses.... The Fed’s expansionary policies... have the side effect of somewhat weakening the dollar... paving the way for a smaller U.S. deficit. And the Chinese and Germans don’t want to see that happen....

But why are Republicans joining in this attack?

Mr. Bernanke and his colleagues seem stunned to find themselves in the cross hairs. They thought they were acting in the spirit of none other than Milton Friedman, who blamed the Fed for not acting more forcefully during the Great Depression — and who, in 1998, called on the Bank of Japan to “buy government bonds on the open market,” exactly what the Fed is now doing.

Republicans, however, will have none of it, raising objections that range from the odd to the incoherent. The odd: on Monday, a somewhat strange group of Republican figures — who knew that William Kristol was an expert on monetary policy? — released an open letter to the Fed warning that its policies “risk currency debasement and inflation”... [not[ explain[ing] why we should fear inflation when the reality is that inflation keeps hitting record lows.... Two Republicans, Mike Pence in the House and Bob Corker in the Senate, have called on the Fed to abandon all efforts to achieve full employment and focus solely on price stability. Why? Because unemployment remains so high. No, I don’t understand the logic either.

So what’s really motivating the G.O.P. attack on the Fed? Mr. Bernanke and his colleagues were clearly caught by surprise, but the budget expert Stan Collender predicted it all. Back in August, he warned Mr. Bernanke that “with Republican policy makers seeing economic hardship as the path to election glory,” they would be “opposed to any actions taken by the Federal Reserve that would make the economy better.” In short, their real fear is not that Fed actions will be harmful, it is that they might succeed.

Hence the axis of depression.... China and Germany want America to stay uncompetitive; Republicans want the economy to stay weak as long as there’s a Democrat in the White House...

Indeed, it is now clear that the right-wing objection to the policies of the Obama administration was not an objection to fiscal policy as an inappropriate policy modality for stabilizing nominal spending. It was, instead, an objection to the very idea that the government should try to serve as a stabilizing macroeconomic balance wheel.

The flow of economy-wide spending is low. Thus Ben Bernanke's Federal Reserve is moving to boost the flow. It is doing so by changing the mix of privately-held assets as it buys government bonds that pay interest in exchange for for cash that does not.

That is totally standard.

There is only slightly nonstandard thing. The bonds that pay interest the Fed is buying are not the usual three-month Treasury bills but seven-year Treasury notes instead. The Federal Reserve has to do this, because those are the shortest-duration Treasury bonds that now pay interest. It cannot reduce short-term interest rates below zero, and so it is attempting via this policy of “quantitative easing” to reduce longer-term interest rates.

And the right wing objects to this.

For decades I have confidently taught my students about the rise of governments that take on responsibility for the state of the economy. Governments pre-WWI and even more so pre-WWI did not take on the mission of keeping unemployment from rising high in economic downturns. Why not? There were three reasons, all of which vanished by the end of WWII.

There was then a hard-money lobby: a substantial number of very rich, socially influential, and politically powerful people whose investments were overwhelmingly in bonds. They had little--personally--at stake in a high level of capacity utilization and a low level of unemployment. They had a great deal at stake in stable prices. They wanted hard money above everything.

Back in those days the working classes that was hardest-hit by high unemployment did not generally have the vote. Where they did have the vote, they and their representatives had no good way to think about how they could benefit from stimulative government policies to moderate economic downturns, and they had no way to reach the levers of power in any event.

Knowledge about the economy was in its adolescence. Knowledge of how different government policies could affect the overall level of spending was closely held. It was--the American Free Silver Movement excepted--not the subject of general political and public intellectual discussion.

Today we have next to no hard-money lobby, for nearly everybody has a substantially diversified portfolio and suffers mightily when unemployment is high and capacity utilization and spending are low. Economists today know a great deal--albeit not as much as we would like--about how monetary, banking, and fiscal policies affect the flow of nominal spending, and their findings are the topic of a great deal of open and deep political and public intellectual discussion. And the working classes all have the vote.

But here we are, with Austerians. So cui bono? Who benefits from austerity in the U.S.? How in the North Atlantic can we have a large political movement pushing for the hardest of hard-money policies when there is no hard-money lobby with its wealth on the line? How is it that the unemployed, and those who fear they might be the next wave of unemployed, do not register at the electoral polls? Why are politicians not terrified of their displeasure? And why are principles of nominal income determination that I thought had been largely settled since 1829 now not settled? Why is the idea, common to John Maynard Keynes, Milton Friedman, Knut Wicksell, Irving Fisher, and Walter Bagehot alike, that the first task of the government is to undertake strategic interventions in financial markets to stabilize the flow of economy-wide spending now a contested one?

Paul sees a material interest link: he sees German and Chinese governments that seek a continued large U.S. trade deficit to allow their export surpluses, Republican politicians who think trashing the economy is the way to majorities, and economists who think that supporting Republican politicians is the road to influence. I don't think that can be a complete explanation: very few people are comfortable living with the idea that they are villains wreaking destruction on the world for their own narrow advantage.

Thus I read Charles Calomiris's claim that it is inappropriate for the Federal Reserve to aim for a short-term nominal GDP growth rate above 5% per year no matter how high the unemployment rate, and I am simply bewildered...

The importance of a Nominal Anchor to the Price Level II

J. Bradford DeLong (1999), "Should We Fear Deflation?" Brookings Papers on Economic Activity 1999:1 (Spring), pp. 225-252:

[...]

J. Bradford DeLong and Lawrence H. Summers (1986), "Is Increased Price Flexibility Stabilizing?" American Economic Review 76:5 (December), pp. 1031-1044:

James Tobin (1975), "Keynesian Models of Recession and Depression," American Economic Review 65:2 (May), pp. 195-202:

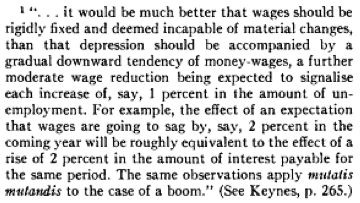

John Maynard Keynes (1937), The General Theory of Employment, Interest and Money (London: Macmillan):

The Importance of a Nominal Anchor to the Price Level...

Gauti B. Eggertsson and Paul Krugman:

Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach: In this paper we present a simple New Keynesian-style model of debt-driven slumps – that is, situations in which an overhang of debt on the part of some agents, who are forced into rapid deleveraging, is depressing aggregate demand. Making some agents debt-constrained is a surprisingly powerful assumption: Fisherian debt deflation, the possibility of a liquidity trap, the paradox of thrift, a Keynesian- type multiplier, and a rationale for expansionary fiscal policy all emerge naturally from the model. We argue that this approach sheds considerable light both on current economic difficulties and on historical episodes, including Japan’s lost decade (now in its 18th year) and the Great Depression itself.

November 19, 2010

The Topic of Depression Economics in a Nutshell

From my September 15, 2010 Econ 1 lecture:

Let me, once more, present to you how you should think about the topic of “depression economics.” This time, however, let me just provide you with the spine of the subject.

The US employment to population ratio over the last three years has crashed from 63.4 down to 58 point something percent of American adults. This collapse is not because we have forgotten how to make things. It is not because we’ve all decided we want to take longer vacations, or go back to school, or get in touch with our inner selves. It is not because our capital goods have mysteriously rusted away. This collapse in employment is the result of a collapse in spending, a generalized deficiency of aggregate demand, an excess of aggregate supply, pretty much everywhere in the economy.

There is only one sector I am aware of that is still at capacity: high-end restaurants within a mile of the capital in Washington DC. Those still appear to be at full employment and at full capacity. Nothing else in the economy is.

The question of why this should happen is an important one. Why should there be such crashes in the level of employment? How can it be that there is not enough spending, not enough demand in the system to put everyone who wants to work to work productively? Back in 1803 Jean-Baptiste Say observed that nobody makes except to use or to sell. and nobody sells except to buy. Thus, he argued there can be particular shortages of demand in some commodities balanced by excesses of demand for others. But “overall excess demand” is self-contradictory because everybody’s spending is someone else’s income and everyone’s income is then spent sooner or later on something. How is it that the economy can wedge itself into a position like it is in today? That is an important question.

And this question has an answer. The answer is that what we try to spend our money on does not have to be currently produced goods and services. Say’s Law says that if there is excess supply for something there has to be excess demand someplace else in the system is sound. But the excess demand does not have to be for currently-produced goods and services. The excess demand can be for financial assets. People can be trying to switch their spending away from currently-produced goods and services in order to build up the amount of financial assets they have.

That is what gets the economy wedged in a position of high unemployment—like it is today.

This is bad news for Say and good news for us. It is bad news for Say because it means there is a hole in his logic that the market system would always work well on a macroeconomic level. It is good news for us because it suggests a way to cure even a big down turn in employment and production. Such a downturn should have a cure in the form of a strategic financial intervention by the government. Find a way for the government to fix the excess demand in financial markets, and you fix the deficient demand for currently-produced goods and services—you fix the economy.

Historically, we have had three types of excess demand for finance that have produced big downturns in economies.

First, we have seen excess demand for bonds—for the pieces of paper corporations and the government issue that pay interest and eventually return your principal—for the savings vehicles that enable you to take your purchasing power, store it up, and use it in the future, with interest. When there is an excess demand for bonds—when planned savings is greater than planned investment—we then have downward pressure on the flow of currently-produced goods and services as individuals try to build up their stock of savings vehicles beyond what is possible. How large a downturn? We have a master equation from the income-and-spending approach to enable us to calculate how far the level of production will fall. We fix this kind of downturn by having the government do something to restore balance in the market for savings vehicles, the market for bonds. If it can reduce the demand for bonds or increase the supply, it can fix the excess demand for bonds and thus the deficient demand for currently-produced goods and services.

That is the type of downturn we saw in 2002. It is not the kind we have now. If it were, then bonds would be expensive—there would, after all, be high and excess demand for them. But right now risky bonds are cheap.

Second, we have also seen in history excess demands for liquid cash money. Such an excess demand produces a monetarist downturn as nearly everybody cuts back on their spending on currently-produced goods and services in order to try to build up their holdings of liquid cash money above what is possible. It is possible to tell when there is monetarist downturn: since everybody is trying to build up their stocks of liquid cash money, everybody is selling their other financial assets and thus their prices—stocks, bonds, whatever—and all their prices are low. That is not the kind of downturn we have today: today the prices of some financial assets—the liabilities of credit-worthy governments, for example—are very high.

In a monetarist downturn there is also a master equation to calculate the size of the fall in production: the quantity theory of money equation.

And here again we know how to fix the problem with the economy. If the Federal Reserve increases the stock of liquid cash money in people’s pockets enough by buying short term government bonds for cash, it relieves the excess demand for cash and so cures the deficient demand for currently-produced goods and services. That is the kind of downturn we saw in 1982.

Today, however, we have a third kind of downturn: a different kind of downturn than one generated by a shortage of money or of bonds, than a monetarist or a Keynesian downturn. We know we do not have a monetarist downturn because the prices of a number of non-money financial assets are very high. We know that we do not have a Keynesian downturn because the prices of some savings vehicles are very low. So what do we have?

We conclude that the excess demand in financial markets right now on the part of investors is an excess demand for safety: for high quality AAA-rated assets for people that hold in their portfolios. Prices of risky financial assets are low—there is no excess demand for them. Prices of safe financial assets are high—there is an excess demand for them.

Thus businesses and households have cut back on their spending on currently-produced goods and services as they all have concluded: “We don’t have enough safe assets in our portfolios. We need to stop spending so much until we build up our holdings of safe assets to a higher level.” And the fact that they cannot do so because there is a shortage of safe assets in the economy is what is keeping us wedged in this current situation of high unemployment and low capacity utilization.

Where did this excess demand for safe assets come from?

It came as a consequence of the deregulation of finance and of the securitization of mortgages, from the housing bubble and the crash, from the fact that then it turned out that investment banks that had created brand new derivative securities based on mortgages had not originated-and-distributed them but had, to a remarkable and astonishing degree, originated and kept them. They were supposed to sell off all the pieces o real estate risk in small bundles to savers all over the world. They did not.

When it turned out that these mortgage-backed securities were actually a lot riskier than had been claimed, the natural response was to fear. For not only were those securities exceptionally risky, but all debts of any financial organization thought to be holding any significant amount of mortgage-backed securities became risky as well. Thus the economy-wide supply of safe assets fell massively just at the very point in time when increasing uncertainty and the coming recession made everyone wish to hold more safe assets in their portfolios.

So what do we do now?

Cutting-edge macroeconomic theory—the theory of Say (1803) and Mill (1829)—tells us that we can fix the real-side economic downturn if we fix the excess financial market demand for safe assets. Successfully doing that would be a neat trick. Figuring out how to regulate financial markets so that we can keep it from happening it again would be an even neater trick.

So how is the government doing at this task?

There are two ways to look at it: half-full and half-empty.

The half-full way is that of Alan Blinder, adviser to the Obama campaign, and Mark Zandi, adviser to the McCain campaign. They have a paper claiming that if the government had simply stepped back in the fall of 2008 and let the economy “liquidate” itself, that right now our unemployment rate would be 16%.

The fact that the unemployment rate now is only 9.6% rather than 16%—Henry Paulson who was Bush’s secretary of the treasury and Tim Geithner who is Obama’s secretary of the treasury take pride in that as a substantial accomplishment: their policies have kept 6.5% of the American labor force from becoming unemployed.

The half-empty way is to say: “Wait a minute. The unemployment rate ought to be 5%. Even an generous estimate of how much extra structural unemployment there is in America today the unemployment rate should still not be much above 6%. But it is 9.6%. It is way above where it ought to be if the market were working smoothly and well. Policy simply has not done enough.”

That is the spine of the topic of depression economics.

October 29 Conference: "New Deal or No Deal?"

New Deal or No Deal?: 3:30‐5:30 – Late Afternoon Session – STIMULUS & RESPONSE: Chair: Neil Fligstein, UCB:

Bailouts & Financial Reform – Dean Baker, Center for Economic Policy Research, W.D.C.

Is a New Financial Order Possible? – Barry Eichengreen, Economics, UC Berkeley

Battered but Not and Beaten – Brad DeLong, Economics, Berkeley

Job Creation & Destruction – Jesse Rothstein, Public Policy, UC Berkeley

Liveblogging World War II: November 19, 1940

From Time:

BATTLE OF BRITAIN: Laws of War: Home Guardsman Harry Foulds was haled before the magistrates of Chatham, Kent, charged with theft from the Crown of a pistol, ammunition and a helmet which he had taken from a bailed-out German airman. Defense Counsel Gerald Thesinger based his case on Rex v. Broom, in the reign of William III, which was based in turn on a case tried during the reign of Henry VIII. These cases upheld the right of any British subject to retain any property he may be able to seize from "the King's enemy." "Therefore," argued Thesinger, "the property was never vested in the Crown."

Clerk of court: "Under your argument, Home Guards capturing tanks would be able to keep them?"

Thesinger: "Yes, subject to a military law which may apply to the capture of fortresses."

The magistrates upheld the 260-year-old decision of Rex v. Broom and freed Foulds, who was carried from the court by cheering crowds.

J. Bradford DeLong's Blog

- J. Bradford DeLong's profile

- 90 followers