J. Bradford DeLong's Blog, page 1152

September 10, 2014

Over at Equitable Growth: What Is Special About Recessions in a "Monetary Economy": Trollng Nick Rowe

Over at Equitable Growth: Nick Rowe has a nice, intuitive, monetarist take on the core of macroeconomics. But he keeps failing to convince me completely. And I keep failing to make my objections clear in a way that convinces him I have a point rather than simply being a Crazy-Old-Keynesian-Yelling-at-Clouds. Let me try it again:

The way Nick sees it, The key is money demand and money supply (at full employment). When money demand is greater than money supply, people try to cut their spending hello their income in order to build up cash balances. The problem, of course, is that one person spending is another person's income. So everyone's income falls until everyone's income is so low that people in aggregate no longer wish to build up their cash balances right now. And there the economy sits, depressed, until something happens to balance money demand and money supply (at full employment). [READ MOAR:]

This story of Nick Rowe's is all well and good. But it has one big hole. It strongly suggests that when depressions happen all other assets go to discounts vis-a-vis cash: people are, in addition to trying to cut spending below income, hoping to dump other assets for cash as well. Yet some depressions happen when savings vehicles are not at a discount but at a premium vis-a-vis cash. And other depressions happen when not all but only safe savings vehicles are at a premium vis-a-vis cash.

This suggests that simply characterizing a general glut as a time of excess demand for cash is not exactly wrong but in some way inadequate and incomplete.

Let's start over. Let's start again, with Walras's Law: the sum of planned excess demands for all commodities must sum to zero. And let's start with a two-commodity economy in equilibrium: lattes and yoga lessons. Suppose there is a shift in preferences so that people want to drink more lattes and take fewer yoga lessons. What happens? On the market day after the shift, the latte-pullers and yoga teachers show up to their jobs. The latte-pullers discover a zoo: more demand than they can possibly meet. Some ration by raising their price. Others ration by rationing. Some customers buy at the price they expected. Some buy at an unexpectedly high price. Some do not get to buy.

The yoga market, by contrast, is slack: some fill up their capacity by cutting their prices, and some wind up with small classes and few classes and sit idle some of the time. In the following days, weeks, and months, the markets for lattes and yoga lessons adjust. Yoga teachers exit the market, retrain as baristas, and start pulling lattes.

On the boom side, the fact the market for lattes is not characterized by long-term fixed-price contracts means that the rationing is quickly ironed out: the price of lattes rises to balance supply and demand, and then gradually falls as retrained yoga instructors show up and add to supply. On the slump side, earnings of yoga instructors are meager and prices of yoga lessons are low until the excess suppliers have exited. Depending on the market structure, there may or may not be something that looks like "involuntary unemployment".

And as long as the worker migration from yoga instructor to barista is in progress, there will be macroeconomic consequences. The high earnings of the baristas are unlikely to be exactly large enough to offset the low earnings of the yoga instructors, But that is a second-order consequence: the first-order process is the excess demand for lattes balanced by the excess supply of yoga lessons and the necessary process of structural adjustment thus triggered.

OK. Now let us add a third commodity: gold. And let us rerun the scenario, but this time with a shift in demand from yoga to gold: The story would seem to be the same: a structural depression in the yoga lesson industry and a structural boom in the gold mining industry. To the extent that it is more difficult to retrain yoga instructors as gold miners the process of adjustment takes longer. To the extent that gold is a durable good that does not wear out The shift of labor into gold-mining to meet the demand has to be followed by a shift back into yoga once the additional stock demand is satisfied info and returns to its previous level. To the extent that human psychology leads yoga instructors to have a mental block against cutting the prices they charge in gold terms, the disequilibrium sectoral depression and yoga has higher prices, lower quantities, and something that looks very much like "involuntary unemployment". To the extent that gold is not only a commodity for which there is a stock demand but also a unit of account, a fall in the gold price and quantity of yoga lessons may lead to a wave of costly and pointless bankruptcies that will have other macroeconomic effects. But the fact that the demand for the stock of gold is a demand for a medium of exchange does not seem to be of the essence--the things that make this a macroeconomic problem rather than a sectoral depression, disequilibrium, and structural adjustment problem are (a) downward price stickiness and (b) the unit of account-bankruptcy-credit-channel complex.

OK. Now eliminate the gold: replace it with fiat paper money issued by a central bank. And the shock is that something happens that increases demand for the fiat cash. The story seems to be somewhat different. Instead of the process of meeting the demand for gold being lengthy and painful as labor makes its way from yoga studio to gold mine, there is no high-value alternative for displaced unemployed yoga instructors to shift to. In the presence of yoga lesson price rigidity, there is no market adjustment of the quantity of money. The central bank has to choose to follow the right monetary policy to avoid grinding deflation, or not.

Now let us remove fiat money, but add banks that make loans and accept interest-bearing deposits--they can invest their extra deposits in fruit trees if they wind up with positive deposits. The shock this time is a jump in demand for savings vehicles--for interest-paying deposits. When the shock hits, the interest rate falls--buying a share of a fruit tree becomes more expensive--and we have a depression in the yoga sector and a boom in the fruit-tree planting sector: it looks a lot like the gold-mining boom.

How exactly does the specificity of a "monetary economy" manifest itself in these potted examples? There seems to me to be a continuum between sectoral adjustment (with macroeconomic consequences) in the cashless yoga-latte economy to sectoral adjustment (with macroeconomic consequences) in the yoga-latte with monetary gold economy (in which the demand for gold comes not because it is shiny and pretty but because it was money) to pure macroeconomic distress in the yoga-latte with fiat money economy to pure macroeconomic distress in the cashless yoga-latte-fruit trees economy...

Where am I wrong here?

Over at Equitable Growth: Hoisted from the Weblog Archives, Reading Which Breaks My Heart, from Five Years Ago: Generating a Robust Recovery

Over at Equitable Growth: Hoisted from the Archives from Five Years Ago: [Generating a Robust Recovery}(Generating a Robust Recovery) Economic Policy Institute:

Macroeconomic Policy for a Stronger Recovery

J. Bradford DeLong

Professor of Economics, U.C. Berkeley

Research Associate, NBER

September 30, 2009

A Little Background

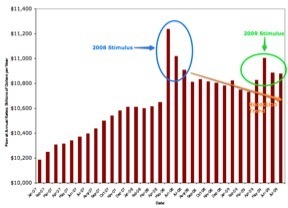

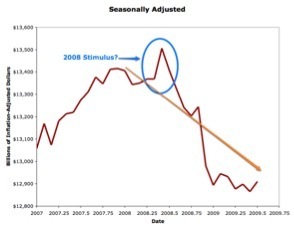

About a year and a half ago—in the days after the forced merger of Bear Stearns into J.P. MorganChase, say—there was a near consensus of economists that an additional dose of expansionary fiscal policy was unlikely to be necessary. The Congress had passed a first round of tax cut-based stimulus, the impact of which in the summer of 2008 is clearly visible in disposable personal income and perhaps visible in the tracks of estimated monthly real GDP. The near-consensus belief back then, however, was that that was the only expansionary discretionary fiscal policy move that was appropriate. READ MOAR

With the Bear Stearns forced merger it appeared that the Federal Reserve and the Treasury had settled on a policy: they would punish as severely as they could the shareholders of and the managers at institutions too-big-to-fail that required rescue, but that they would insulate bondholders and counterparties. The incentives to avoid bankruptcy would thus be concentrated on those who actually had power to do something to manage organizational risk. As for the rest—well, the markets interpreted the forced merger as the Federal Reserve guaranteeing and making riskless essentially all the unsecured debt of all the large commercial and investment banks in the country.

Figure 1: (Nominal) Disposable Personal Income

Figure 2: Monthly Real GDP Estimates from Macroeconomic Advisors

The resulting “approaching liquidity tsunami,” as more than one senior policymaker described it to me, meant that the risk of a deep recession was very low—or so the situation looked in the spring of 2008.

Late 2008’s Need for Expansionary Fiscal Policy

By the late summer of 2008 things looked significantly different. The tax-based expansionary fiscal policy of early 2008 had had less than the desired effect—perhaps it had prevented a decline in the economy and kept things marching in place, but it effect was not overwhelming and not entirely obvious. It was clear that the formal announcement that the economy had fallen into recession was only a matter of time.

By August 2008 Lawrence Summers was writing of a gap between actual and sustainable production of $300 billion at an annual rate, forecasting that that gap was likely to more than double over the following year, and predicting sustained weakness thereafter—“unemployment peaked nearly two years after the end of the last recession, output and employment are likely to remain below their potential levels for several years in the best of circumstances…” in a time when “the remaining scope for monetary policy to stimulate the US economy is surely very limited…”[1] Take an initial output gap growing from $300 to $600 billion over the first year and then declining to zero over the next three and you have a cumulative output gap of $1,350 billion in a situation in which monetary policy on it own can do little to correct it. Suppose that a prudent use of fiscal policy would be to enlarge the government’s budget deficits by a third of the forecast output gap, and you have an estimate of the appropriate size of expansionary fiscal policy as the situation looked in August 2008: $450 billion in cumulative deficit spending spread out over the next four years.

Then came the nationalization of Fannie Mae and Freddie Mac on September 7, 2008; the bankruptcy of Lehman Brothers on September 15, 2008; and the nationalization of AIG on September 22, 2008. In the aftermath it was immediately clear that the recession problem was at least twice as bad as it had looked in August, and over the next four and a half months until the February 17, 2009 signing of the ARRA the magnitude of the likely cumulative output gap doubled again as the magnitude of the financial crisis’s impact on the real economy became clear.

If $450 billion was the appropriate size of a short-term deficit-spending program for the $1,350 billion cumulative output gap anticipated as of August 2008, then simple extrapolation suggests that the appropriate size of the boost to short-term deficit spending as of February 2009 was $1.8 trillion (over three to four years).

What we got was a cumulative number of $600 billion—roughly 1/3 aid to states, 1/3 tax cuts (in a good-faith effort by the Obama administration to propose a bipartisan plan that legislators of both parties could sign on to), and 1/3 infrastructure and other direct government purchases intended not so much to slow the decline as rather to boost the recovery. We also got an extension of the AMT and other measures that no economist I have talked to believes are properly counted as part of an effective fiscal boost under any currently-live theory of how the economy works. Figure an increase in deficits of $200 billion per year spread out over the next three years. At the technocratic level, the disproportion between the size of the response and the magnitude of the need is obvious.

Today’s Arguments Against More Fiscal Expansion

Now if you go outside and, addressing the air, ask why it is that we did not pass a larger short-term deficit-spending fiscal boost program of $1.2 or $1.8 trillion last January and February and why we are not acting to boost it now, I hear four different answers coming back on the wind:

This was the most that the Obama administration could get sixty senators to vote for—and with a Senate that, in Majority Leader Harry Reid’s words, takes forty-eight hours to flush the toilet it needs to spend its time on legislative initiatives that might pass, rather than on those that certainly will not.

Further expansionary fiscal policy would be counterproductive in this current situation because of the long-run U.S. budgetary and global balance-of-payments imbalances. More short-run deficit spending would require the U.S. to issue more debt which would cause a sharp spike in U.S. long-term interest and a flight from the dollar that would generate a much bigger crisis and deeper depression—as Austria’s issuance of huge amounts of additional debt in 1931 set off the wave of crises that turned the recession of 1929-1931 in Europe into the European half of the Great Depression.

Further expansionary fiscal policy would be counterproductive because it never works—because it is theoretically impossible for it to work—because it is a “fairy tale.”

The ARRA is only one of a large number of initiatives to stimulate the economy outside of the normal open-market operations monetary expansion framework. When you include the likely effects of all of the acronyms—TARP, PPIP, MMIFL, TALF, CPLF, TAC, etc.—you find that even though there is only $600 billion of cumulative expansionary fiscal policy, there is much more in terms of total non-standard-monetary stabilization policy.

Argument #1 I will pass over. I understand why Rhode Island and Delaware have as many senators as New York or Florida or Texas or California: it seemed a reasonable price to pay back in 1787 to keep not just Montreal but also Providence and Wilmington from becoming British imperial fortresses and bases on the North American continent. I understand that a “cooling” chamber might wish to have an effective supermajority requirement. I don’t understand why in a good system it takes the votes of 60% of senators rather than of senators representing 60% of the people to actually get an up-or-down vote. But that is not my area.

Argument #2 is, I think, a genuine thing to fear. But if that fear were to cease being a nameless dread and instead take a shape and a name, the first sign would be an unwillingness on the part of global investors to hold U.S. Treasury debt. But right now the U.S. government can borrow for ten years at 3.34% in nominal dollars—much less than the projected growth rate of nominal GDP over the next decade at between 5% and 6% a year. The time since the summer of 2007 has seen a collapse in the value of private securities and a substantial elevation in the price of U.S. government securities. The first rule of the market is that the market’s prices are there to signal what things are more valuable and that we should make more of. Right now the market is sending us a very strong signal that it really wants us to make more U.S. Treasury debt—to undertake more short-term deficit spending. And when argument 2 ceases being a nameless dread but takes form and shape in an upward trend in interest rates on long-term U.S. Treasuries, I will be the first to say that the global bond market is cutting off our running room for more expansionary fiscal policy. Right now, however, it is not.

Argument #3—that there is some deep principle in economic theory somewhere that says something that prevents debt-financed government spending from boosting employment and output—is an argument that, by this stage, I can do nothing but laugh at. When the venture capitalists of Silicon Valley decided to give their money to high-tech engineers in the 1990s so they could spend it trying to figure out how to make money off of the internet, employment and production rose (even though few of them figured out how to do so). When the financial engineers of Countrywide in the 2000s decided to give investors’ money to construction companies to build more houses, employment and production rose (even though the promises to investors of healthy returns with little risk were wrong). Milton Friedman’s quantity-theory-of-money monetarism says that the reason open-market operations that expand the money stock boost spending and employment is because once people have more money in their pockets they step up their spending. Boosts to employment and production come when any group with substantial money in an economy decides to boost its rate of spending—and, at this level, the government’s money is as good as anybody else’s.

And when I try to read the arguments of those making Argument #3, my head explodes. The kindest thing I can say is that they must not have spent even half an hour thinking about the issues. John Cochrane of the University of Chicago writes that models in which fiscal policy affects anything are logically inconsistent because they require that people’s plans of how much to spend exceed what their incomes actually turn out to be. But Chicago models of an earlier generation like Milton Friedman’s are full of situations in which planned expenditure is greater than or less than income as people try to run down or build up their cash balances. Eugene Fama of the University of Chicago writes that any increase in government purchases must be automatically offset by an equal decrease in business investment or household consumption spending—a conclusion that had eluded every other monetary economist since the 1910s, and a conclusion which would make not just fiscal policy but monetary policy impotent.[2]

At this stage all I can do is two things. First, I can gesture at the Republican office holders and policy advisors of last year—at the Doug Holtz-Eakins, the Mark Zandis, the Phil Swagels and the others who are now saying that you should be “skeptical” of “anyone who tells you [expansionary fiscal policy] has had no impact.” Second, I can point out that had John McCain won the 2008 presidential election the Republican administration would have no more hesitation in proposing expansionary fiscal policy than they did in 2008, 2003, and 2001, and that the only reason the views on macroeconomics of Cochrane, Fama and company are now getting a hearing as Republican witnesses in congressional hearings is that Republican legislators need some form of ideological cover for their just-say-no-to-everything-whether-it-is-good-for-the-country-or-not legislative strategy.

Argument #4—that the asset purchase, asset guarantee, and bank recapitalization policies are about to have a big effect and boost the recovery—is one that I really wish were true, but I just don’t see evidence of it, at least not right now. Yes, spreads have narrowed. But asset values are still low: the S&P 500 stands about where it did early last October, after Lehman, after AIG. The banking-sector policies were supposed to boost the confidence and the risk tolerance of the private market in order to get the engine of private sector lending and borrowing and spending rolling again. Things are much better than they were at the start of March 2009, it is true. But as measured by the mark of asset prices, they are no better than they were in October 2008.

And it is by asset prices that the banking-sector support policies should be judged. The right way to look at monetary and financial policy is that it has, ever since 1825, been focused on manipulating asset prices: the central bank buys and sells and guarantees and regulates and subsidizes and nationalizes with an eye toward pushing the prices of financial assets to levels where businesses seeking to raise capital to build capacity and households seeking to spend out of wealth together can issue new assets and so access enough money to push their spending to a level that gets the economy to full employment, or at least out of depression. The policies are always sold as opaque technocratic adjustments to the “money stock” or to a “federal funds interest rate” that real people do not see and is of concern only to bankers. But the policies are and always have been truly aimed at manipulating asset prices. We may believe in a market economy. But since 1825 we have also believed that asset prices are too important to be left to the market to determine when their free market levels produced either depression unemployment or runaway inflation.

Thus the thing to focus on is that the prices of risky financial assets are very low—not as low as they were last March, when the S&P 500 kissed a level of 667, but still very low. Why are they so low? The answer is that the risk tolerance of the private market has collapsed. For example, consider what the University of Chicago’s Nobel Prize-winning economist Bob Lucas told Tom Keene of Bloomberg last March 30—that he was 100% in cash:

LUCAS: [T]here is no question that fear is what this liquidity crisis is. I mean the reason I got into money [with my portfolio] is that I got afraid to leave my pension fund in other securities. So I’m sitting there with a portfolio full of zero-yield stuff just because I’m afraid to do anything else. I think there are millions of people like me.

KEENE: What will be the signal for Robert Lucas to go back into the markets...?

LUCAS: I don’t know. Robert Rubin made a joke about that in the first session today. Nobody knows...

Now let’s pick on Lucas because he is not here to defend himself, Earlier in the interview, he had told Tom Keene:

LUCAS: Our economy’s got a remarkable ability to return to its long term growth trend. And for most of the depressions we’ve had or recessions, the return has been quick. Two or three, four years...

Lucas says that it is highly likely that the U.S. economy will be back to normal in three or four years, with a normal level of unemployment, a normal share of profits in national income—and a normal level of dividends and capital gains. This presumably means that stock prices will also be back to a normal multiple of long-run earnings, which means a year-2015 S&P of 2000 or so, compared to its current value of 1044 or its 2009 low of 667. Investing in the S&P 500 for a four-year horizon now is risky, certainly, but the expected return is high: 15% per year, if you believe Lucas’s forecast. And holding your money in cash is not all that safe either: the scenarios I can envision in which the S&P 500 is at a real value in 2015 corresponding to the value that 667 buys today are scenarios in which inflation has eaten away most of the value of cash.

So what is Lucas doing holding his portfolio in cash? Has risk suddenly increased to an extraordinary extent to force the equity share of his portfolio down from 70% to 0% in spite of the huge jump in expected six-year returns? Has his personal tolerance for risk suddenly collapsed? No. He is irrationally panicked. And, as he says, there are millions like him. Until they recover from their panic, even a perfectly constructed banking and financial system will not produce the asset prices needed for private investment spending to drive us to full employment.[3]

Thus the banking-sector support policies have not been a bust—they have surely kept things from getting much worse. But they have not done much if anything that promises to close the output gap.

What Should We Do Now?

The argument that more expansionary fiscal policies should not be tried because it is theoretically impossible for them to work fails. The argument that more expansionary fiscal policies should not be tried because the unstable nature of global imbalances and U.S. long-run fiscal deficits has us teetering on the edge of a Credit Anstalt-like currency crisis disaster fails. The argument that banking policies have been successful enough that we do not need more expansionary fiscal policy fails.

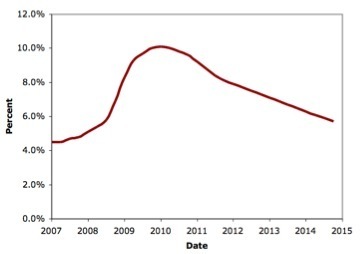

Figure 3: Troika Forecast of the Unemployment Rate as of August 2009

The Congressional Budget Office currently forecasts that the unemployment rate will average 10.2% in 2010, 9.1% in 2011, and 7.7% in 2012 before returning to its normal range with an average of 5.1% in 2013. The administration’s Troika forecast is very similar. Things will almost surely be either significantly better or significantly worse than the forecast—it is a forecast, after all—but the right thing to do is to plan as if the forecast will come true, and then adjust later.

If you are happy with that forecast and think that it is appropriate for the U.S. economy over the next four years, then no further support for the recovery appears needed at this time. If you are unhappy with that forecast, then additional federal government action is definitely advisable.

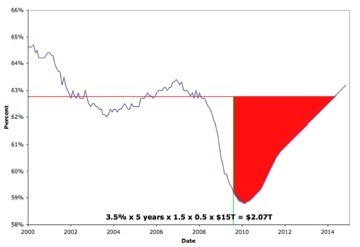

Figure 4: Past and Projected Employment-Population Ratio

What kind of action, however?

The obvious would be additional short-term deficit spending on the federal level:

(1) Triggers to extend the existing expansionary fiscal policy measures should the unemployment rate not decline rapidly: since we remember the history of the 1937-1938 episode, we are hopefully not condemned to repeat it.

(2) An expansion not in length but in flow of the current fiscal boost package: last January a number of us were saying that an $800 billion cumulative fiscal boost was OK—but that there also ought to be a trigger in the budget resolution so that if unemployment rose near 10% the fall reconciliation bill could be used to top off the program. That didn’t happen. It ought to have happened. It would be nice to make it happen—and there is a deal to be struck with more deficit spending in the short-term and tax-increase or spending-cut triggers in the long term should the deficit not return to sustainable levels after the recession passes.

(3) Less obvious would be measures to aid useful deficit spending in other levels of government. During this recession the states have, as Paul Krugman puts it, turned into fifty little (and not so little) Herbert Hoovers. The obvious policy to enable states that want to avoid counterproductive budget-cutting in this recession to do so is:

Have the federal government support the prices of deficit-spending bonds issued by state governments that also put credible and automatic amortization plans in place.

This support could be provided either at the level of the Treasury—with the Treasury Department approving state fiscal policies as sustainable in the long term and thus qualifying for loan guarantees—or at the level of the Federal Reserve—with the Federal Reserve offering to support the prices of state deficit-spending bonds that come attached to legislated sustainable state-level fiscal policies.

(4) Also a possibility: bringing forward long-term investments that we ought to be making over the next generation. The people I talk to at Berkeley who actually know what they are talking about say that over the past decade and a half since the Senate rejected Al Gore’s BTU tax the 3 degree Fahrenheit warmer world in 2150 has probably slipped out of our grasp, and that the good possibility going forward is a 7 degree Fahrenheit warmer world in 2150. To get there the U.S. has to lead—take the first steps—and then work hard to pull the rest of the world along to an appropriate global warming policy.

The best way to get there would be a carbon tax. A somewhat worse way would be a cap-and-trade system that grandfathers in many current highly inefficient uses of open carbon cycle energy. A still worse way would be for the EPA to start regulating greenhouse gases as pollutants. We would like to use the effective carrot of the market rather than the stick of command-and-control regulation, but the Senate may keep us from doing so.

In that case—if we aren’t providing the incentives for businesses and people to make the investments in closed-carbon cycle and other green energy technologies through a carbon tax or a cap-and-trade system—then the government will need to make those investments or provide separate incentive programs to induce people to make them. How big? $5,000 per household in commercial, industrial, and residential cost-effective energy investments does not seem out of line. (We’ve done $20,000 over the past five years in our house and are getting 6% per year at current PG&E electricity prices.) And that would be $500 billion nationwide.

[1] Lawrence Summers (2008), “The Big Freeze, Part IV: A U.S. Recovery,” Financial Times (August 6, 2008) http://tinyurl.com/dl20090927a.

[2] Note that neither Cochrane nor Fama are the right-wing fringe of the economics profession right now. The right wing fringe is composed of the supporters of Ed Prescott, Ed Prescott who used to teach at the University of Chicago before moving to Arizona State. He says that Fama’s conclusion that monetary policy does not affect output is in fact correct: in his view the Great Depression was not caused, as Milton Friedman thought, by the bank failure-induced collapse of the money stock but by Herbert Hoover’s “anti-market, anti-globalization, anti-immigration, pro- cartelization policies were instituted… [which] created a great depression.” Chicago economists of an earlier generation, like Jacob Viner, had no doubt at all in the correctness of their policy advice: that the Great Depression had been caused by unbalanced monetary deflation and needed to be cured by expansionary monetary and fiscal policy.

[3] An aside. Lucas’s irrational panic—and his observation that there are millions of investors like him—makes the part of his interview with Tom Keene in which he attacks Robert Shiller and George Akerlof and their book Animal Spirits quite puzzling. Here is what Lucas says:

I just don’t get it. I mean look at the Black_Scholes formula. People come up with a formula for pricing options, just out of purely mathematical reasoning, and then it turns out it fits certain data amazingly well. And it’s been incredibly useful to people. Now it’s not useful for everything, but for what it does it’s a huge advance in human knowledge. Now what’s the behavioral finance contribution? They reinforce the idea of skepticism. Well, skepticism, it’s easy to be a skeptic. What’s harder is to tell somebody how to do something they didn’t know how to do yesterday. That’s what Black and Scholes did...

Lucas seems to miss the entire big point. Black-Scholes tells you how to do things only if the trades of the non-von Neumann-Morgenstern agents in the economy—that's him—cancel each other out. If they don't cancel each other out—if there are, as Lucas says, “millions of people like me,” then a whole bunch of banks running off of Black-Scholes and similar models create a lot of systemic risk, and then 10% unemployment. That’s the problem Akerlof and Shiller are trying to grapple with.

Noted for Your Morning Procrastination for September 10, 2014

Over at Equitable Growth--The Equitablog

Over at Equitable Growth--The Equitablog

Morning Must-Read: Walter Frick: Social Insurance and Surmounting Anti-Entrepreneurial Job Lock - Washington Center for Equitable Growth

Morning Must-Read: Jonathan Chait: Why the Worst Governments in America Are Big Small Local Governments - Washington Center for Equitable Growth

Lunchtime Must-Read: Marika Cabral, Michael Geruso, and Neale Mahoney: Does Privatized Health Insurance Benefit Patients or Producers? Evidence from Medicare Advantage - Washington Center for Equitable Growth

Lunchtime Must-Read: Jens H.E. Christensen and Simon Kwan: Assessing Expectations of Monetary Policy - Washington Center for Equitable Growth

Afternoon Must-Read: Andrew Harless: Employment, Interest, and Money: An Ultraminimalist Model of the Beveridge Curve, or, How I Learned to Start Worrying and Love Structural Unemployment - Washington Center for Equitable Growth

Inbox Zero Again!! - Washington Center for Equitable Growth

Morning Must-Read: Andreas Fuster, Basit Zafar, and Matthew Cocci: Why Aren’t More Renters Becoming Homeowners? - Washington Center for Equitable Growth

Morning Must-Read: Ryan Cooper: It's Time for a Universal Basic Income - Washington Center for Equitable Growth

Ain't It Fun, Living in an r < n+g World?: Tuesday Focus for September 9, 2014 - Washington Center for Equitable Growth

Morning Must-Read: Martin Wolf: Europe Must Do Whatever It Takes - Washington Center for Equitable Growth

Plus:

Things to Read on the Morning of September 10, 2014 - Washington Center for Equitable Growth

Must- and Shall-Reads:

James Hamilton: Other perspectives on the new bond market conundrum

Paul Krugman: Scots, What the Heck?

Antonio Fatas: Antonio Fatas on the Global Economy: Whatever it takes to see helicopter Mario (Draghi)

Cordell Eddings: You Missed $1 Trillion Return Agreeing With Fed Naysayers

Thomas Picketty and Emmanuel Saez: “A Theory of Optimal Inheritance Taxation,”

Econometrica 81 (2013)

Adair Turner: Facing Reality in the Eurozone

Jérémie Cohen-Setton: The shift in the Beveridge curve

Andreas Fuster, Basit Zafar, and Matthew Cocci: Why Aren’t More Renters Becoming Homeowners?: "With a stronger economy and eased credit standards, flows into homeownership would pick up. However, one caveat is that many potential buyers with relatively low credit scores (35 percent of renters in our sample think that their credit score is below 680) might now be 'discouraged', meaning that they are convinced that they would not be granted credit and thus may fail to apply for a mortgage even after an easing in standards. Also, relaxing credit standards may, of course, have undesirable consequences down the road, since borrowers with lower credit scores are at higher risk of default."

Andrew Harless: Employment, Interest, and Money: An Ultraminimalist Model of the Beveridge Curve, or, How I Learned to Start Worrying and Love Structural Unemployment: "The cumulative sum of the residuals peaks in July 2006, suggesting that there may be a structural break in August. A casual look at the residuals strongly suggests another structural break in July 2010. Both purported structural breaks go in the same direction: a decline in the number of hires associated with any given number of job openings. So, contrary to what I said in 2010, it does look like we are seeing more structural unemployment now than in the past.... So what does all this imply about the natural rate of unemployment?... If the relationship between hiring and unemployment is stable, as it appears to be, then my model implies that shifts in the matching function will determine a shifting relationship between the (assumed constant) NAIRV and the NAIRU (Non-Accelerating Inflation Rate of Unemployment, a.k.a. the natural rate of unemployment). For what it’s worth, my estimates suggest that the hypothesized August 2006 and July 2010 shifts in the matching function would, collectively, increase the NAIRU by a factor of about one and a third. So if the NAIRU was 4.5% (my best guess, which happens to be conveniently divisible by 3) in July 2006, it is 6% now..."

Andrew Harless: Employment, Interest, and Money: An Ultraminimalist Model of the Beveridge Curve, or, How I Learned to Start Worrying and Love Structural Unemployment: "The cumulative sum of the residuals peaks in July 2006, suggesting that there may be a structural break in August. A casual look at the residuals strongly suggests another structural break in July 2010. Both purported structural breaks go in the same direction: a decline in the number of hires associated with any given number of job openings. So, contrary to what I said in 2010, it does look like we are seeing more structural unemployment now than in the past.... So what does all this imply about the natural rate of unemployment?... If the relationship between hiring and unemployment is stable, as it appears to be, then my model implies that shifts in the matching function will determine a shifting relationship between the (assumed constant) NAIRV and the NAIRU (Non-Accelerating Inflation Rate of Unemployment, a.k.a. the natural rate of unemployment). For what it’s worth, my estimates suggest that the hypothesized August 2006 and July 2010 shifts in the matching function would, collectively, increase the NAIRU by a factor of about one and a third. So if the NAIRU was 4.5% (my best guess, which happens to be conveniently divisible by 3) in July 2006, it is 6% now..."

Jens H.E. Christensen and Simon Kwan: Assessing Expectations of Monetary Policy: "An ongoing concern has been that the public might misconstrue the Fed’s forward guidance about future monetary policy and underappreciate the extent to which short-term interest rates may vary with future news about the economy. Evidence based on surveys, market expectations, and model estimates show that the public seems to expect a more accommodative policy than Federal Open Market Committee participants. The public also may be less uncertain about these forecasts than policymakers."

Marika Cabral, Michael Geruso, an Neale Mahoney: Does Privatized Health Insurance Benefit Patients or Producers? Evidence from Medicare Advantage: "The debate over privatizing Medicare stems from a fundamental disagreement about whether privatization would primarily generate consumer surplus for individuals or producer surplus for insurance companies and health care providers. This paper investigates this question by studying an existing form of privatized Medicare called Medicare Advantage (MA). Using difference-in-differences variation brought about by payment floors established by the 2000 Benefits Improvement and Protection Act, we find that for each dollar in increased capitation payments, MA insurers reduced premiums to individuals by 45 cents and increased the actuarial value of benefits by 8 cents. Using administrative data on the near-universe of Medicare beneficiaries, we show that advantageous selection into MA cannot explain this incomplete pass-through. Instead, our evidence suggests that insurer market power is an important determinant of the division of surplus, with premium pass-through rates of 13% in the least competitive markets and 74% in the markets with the most competition."

**Walter Frick: If Your Kids Get Free Health Care, You’re More Likely to Start a Company: "Starting a business is risky enough in the best of circumstances. Most new ventures fail, and the prospect of forgoing a salary is enough to keep many would-be entrepreneurs from taking the plunge. But think about how much harder it would be if your child had a health condition, and you couldn’t get her insurance if you struck out on your own. That’s less of a problem in the U.S. than it was a few years ago, thanks to Obamacare, but until recently it was a very real conundrum.... Gareth Olds of Harvard Business School... analyzed Census data from before and after the passage of the Children’s Health Insurance Program in the U.S.... The self-employment rate for CHIP recipients increased from just under 15% of those eligible to over 18%. That amounts to an a 23% increase. The rate of ownership of incorporated businesses--a better proxy for sustainable, growth entrepreneurship--increased even more dramatically, from 4.3% to 5.8%, an increase of 31%.... The basic intuition behind his methods is that a family just above the CHIP cutoff isn’t all that different from a family just below it..."

Jonathan Chait: Why the Worst Governments in America Are Big Small Local Governments: "Police militarization bore only the faintest responsibility for the tragedy in Ferguson.... Old-fashioned policing tools were all the Ferguson police needed to engage in years of discriminatory treatment, to murder Michael Brown, and to rough up journalists covering the ensuing protests.... Ferguson has exposed a genuine opening for thinking about public life in a way that cuts across traditional ideological lines. The problem is what you might call Big Small Government.... Ferguson... is an Orwellian monstrosity. Its racially-biased Police Department is the enforcement wing of a predatory system of government described in scathing detail in a recent report by ArchCity Defenders... an instrument of fiscal (in additional to social) domination. Court fines account for a fifth of the city’s revenue. Police officers disproportionately search black drivers.... The city issues three warrants per household, and its draconian justice system appears designed to bleed its victims. The report notes, 'A Ferguson court employee reported that the bench routinely starts hearing cases 30 minutes before the appointed time and then locks the doors to the building as early as five minutes after the official hour, a practice that could easily lead a defendant arriving even slightly late to receive an additional charge for failure to appear.'... There are not many people who find their freedom so unjustly impaired by the government in Washington as the people of Ferguson are by their local government.... Big Small Government is all around us. We simply haven’t trained our minds to notice it... both right and left have exhibited forms of this mental block.... Why do coastal states lack affordable housing? Because regulations prevent dense construction.... Here is a genuine case of onerous regulation with dire economic consequences.... Or consider occupational licensing. Some 29 percent of American workers need a state-issued license in order to legally do their job.... Income inequality isn’t just about low taxes for the rich and generous compensation for executives; it’s also about the difficulty working-class Americans have getting a job as a barber or a dental hygienist. These regulations don’t exist because of a popular outcry from voters terrified that the person they hire to help them pick out new drapes may lack formal training for the job. They exist because they serve the narrow interests of tradesmen..."

Simon Wren-Lewis: Unconventional Monetary Policy versus Fiscal Policy: "I cannot see why some people insist that unconventional monetary policy is always preferable to fiscal policy. In a comment on a recent Nick Rowe post, Scott Sumner writes 'My views is that once the central bank owns the entire stock of global assets, come back to me and we can talk about fiscal stimulus'. What this effectively means is that it is better for one arm of the state (the central bank) to create huge amounts of money to buy up large quantities of assets than to let another arm of the state (the Treasury) advance consumers rather less money to spend or save as they like. This preference just seems rather strange, but maybe Lenin would have approved!"

Ryan Cooper: America is running out of jobs. It's time for a universal basic income: "The politics of a guaranteed income get a lot easier when you acknowledge that the U.S. is no longer the land of opportunity.... The fundamental bargain of American society is that for anyone willing to hustle, there is a decent job to be found, or one that will at least prevent abject destitution. It underpins our national mythos as the land of opportunity and self-reliance. It has always been less true than anyone wanted to admit, but for an increasingly large fraction of the population--start with the 16 percent of Americans who regularly don't have enough to eat--it's a sick joke.... One can easily imagine the historical process described by Marx going in reverse. In today's labor market, where there are still twice as many job seekers as job openings, the constant conservative carping about the 'dignity of work' sounds more jarring and vindictive by the day. As someone with a nice, stimulating job, I agree that work can help people flourish. But in an economy that is flatly failing to produce enough jobs to satisfy the need, a universal basic income will start to seem more plausible--even necessary."

And Over Here:

How Good a Deal Are Arkansas's Doctors, Hospitals, and Insurance Companies Getting Out of Their Medicaid Advantage Program? Live from The Roasterie CCCXXVI: September 9, 2014 (Brad DeLong's Grasping Reality...)

Liveblogging World War II: September 8, 1944: "Once the Rockets Go Up, Who Cares Where They Come Down? 'That's Not My Department', Says Werner von Braun" (Brad DeLong's Grasping Reality...)

Monday Smackdown: I'm Going to Divert This for a Special ObamaCare Morals-of-the-Halbig Truthers Smackdown (Brad DeLong's Grasping Reality...)

Post-Weekend Reading: Annalee Newitz: 8 Things We Can Do Now to Build a Space Colony This Century (Brad DeLong's Grasping Reality...)

Wisconsin Forecasted to Lag Further Behind Minnesota: Live from Kaldi's Coffee CCCXXV: September 8, 2014 (Brad DeLong's Grasping Reality...)

Liveblogging World War I: September 9, 1914: von Bulow Retreats to the Marne (Brad DeLong's Grasping Reality...)

Over at Equitable Growth: Ain't It Fun, Living in an r n+g World?: Tuesday Focus for September 9, 2014 (Brad DeLong's Grasping Reality...)

Should Be Aware of:

David Glasner: Hey, Look at Me; I Turned Brad Delong into an Apologist for Milton Friedman

Jay Snyder: Diffuse the Math Bomb

Gwynn Guilford: Blue whale numbers off the US west coast are back where they were when we started hunting them

James Oakes: Genovese, Slavery, Capitalism

Kathy Ruffing, Paul N. Van de Water, and Richard Kogan: “Generational Accounting” Is Complex, Confusing, and Uninformative

Larry Summers:* Bold reform is the only answer to secular stagnation

Martin Wolf: Europe has to do whatever it takes: "In the second quarter of this year, real domestic demand in the eurozone was 5 per cent lower than in the first quarter of 2008. The eurozone’s unemployment rate has risen by just under 5 percentage points since 2008. In the year to July 2014, consumer price inflation in the eurozone was 0.4 per cent.... The eurozone is in a depression; lack of demand has played a crucial role; and the European Central Bank has failed to deliver on its own price-stability target. This is not just sad. It is dangerous. It is folly to assume continued stability if economic performance does not improve. A necessary, though not sufficient, condition for grappling with these challenges is understanding them.... Mario Draghi... the one senior eurozone policy maker who shows a grasp of the issues, made a vital contribution at this year’s Jackson Hole symposium.... The capacity of the peoples of member states to tolerate high unemployment and deep slumps has been impressive. But it cannot be unlimited. If that is what the powers that be continue to advocate, the result will probably be a populist reaction.... Who is sure Marine Le Pen, leader of the far right National Front party, will not be the next president of France? Who would follow Matteo Renzi, Italy’s prime minister, if he failed? Yes, these member states need to act. But they surely need support. Mr Draghi has shown the way. The eurozone must follow."

Sahil Kapur: GOP's Obamacare Nightmare Is Coming True: It's Working: "Conservative strategist Bill Kristol's 1993 memo--'"Defeating President Clinton's Health Care Proposal'--warning that reform would paint Democrats as 'the generous protector of middle-class interests' and strike a 'punishing blow' to the GOP's anti-government ideology.... The real fear back then was that health care reform would succeed. Two decades later, Kristol's prophecy is haunting Republicans.... The shift has been crystallized in contentious Senate races this fall. Senate Minority Leader Mitch McConnell (R-KY) recently signaled that Kentuckians benefiting from the state's Obamacare exchange and Medicaid expansion should be able to keep their coverage. Senate GOP candidates Joni Ernst of Iowa, Tom Cotton of Arkansas, Scott Brown of New Hampshire and Terri Lynn Land of Michigan have all refused to call for rolling back Medicaid expansion in their states. The number of television ads attacking the law have plummeted in key battleground states since April, and now even vulnerable Democratic Sen. Mark Pryor of Arkansas is touting his vote for protecting Americans with preexisting conditions under Obamacare..."

Gavyn Davies: The US recovery looks sustainable this time: "The key question is whether this apparently healthy recovery in growth rates can be maintained this time.... When growth was last above trend in 2010, it proved to be a false dawn. The onset of fiscal tightening... slowed the growth of demand. Confidence... was further punctured by threats of fiscal default in Washington, and fears of a collapse of the euro. These threats to confidence have now largely disappeared.... And in the past 3 months, there is evidence that global GDP growth is picking up.... The stimulus to economic recovery from rising domestic demand in the US looks set to continue.... Housing has barely recovered yet and there is pent up growth from an expansion in the number of households as children eventually move out of their parents’ basements.... With the crucial exception of the labour participation rate... most labour market indicators are moving towards previous mid cycle norms.... The economy could run into supply side constraints that lead to overheating... but... it seems premature to worry too much about capacity limits at present. Labour and capital resources are still under-utilised.... As Dominic Wilson of Goldman Sachs pointed out last week, the US continues to track a fairly normal recovery path for an economy that has been hit by a major housing and financial shock.... With demand recovering and supply not yet a constraint on output growth, there is one remaining worry, and that is financial market over-exuberance. The Fed is still largely ignoring the recent BIS warning.... The Fed clearly thinks that the BIS is crying wolf, but in my view it is the most visible wolf out there at present. Unless the financial markets cause an accident, as they have on some recent occasions, this recovery in economic growth should persist for a while."

Chris Dillow: Interest Rates and the 1%: "Nick Rowe says some of the answers to Paul Krugman's question--why do some of the 1% want to raise interest rates?--are daft conspiracy theories. I'm in two minds here.... Since the mid-80s, the income share of the 1% has risen at the same time as real interest rates have fallen. This tells us that low rates are compatible with the 1% doing well.... Easy money is good for asset prices... allow[s] banks to borrow cheaply to the benefit of senior bankers.... Why do some of the 1% want higher rates? One big reason is an empirical claim--that a small rate rise now would nip inflation in the bud and so prevent bigger rises later.... In this sense, I sympathise with Nick. We don't need a conspiracy theory. Those who want higher rates are making a reasonable (though I think dubious) intellectual point. However, there is a political undertow here... about the balance of risks. In particular, the 1% are more inflation-phobic and less unemployment-phobic than the rest of us. I agree with Steve that the rich hate inflation not least because it creates uncertainty. (There's also the historical point that the inflationary 70s also saw the nadir of the fortunes of the 1%: this might be just coincidence, but why risk it?) This alone creates a bias to tighten. What amplifies this bias is that the rich can tolerate mass unemployment.... Peter's question: why has the Keynesian coalition vanished from modern politics? It's because it is no longer politically necessary. It was not Keynes who convinced capitalists of the need for full employment but Lenin.... I sympathize with both sides. On the one hand, Nick's right to say the call for higher rates is the sort idea that people reasonably disagree about. But on the other hand, an understanding of economic policy surely requires us to ask: what is in the interests of the 1%?..."

Lee Billings: Time Travel Simulation Resolves “Grandfather Paradox”: "On June 28, 2009... Stephen Hawking threw a party.... Everyone was invited but no one showed up. Hawking had expected as much, because he only sent out invitations after his party had concluded. It was, he said, 'a welcome reception for future time travelers', a tongue-in-cheek experiment to reinforce his 1992 conjecture that travel into the past is effectively impossible. But... time travel... would have profound implications for fundamental physics... quantum cryptography... computing.... Our best physical theories seem to contain no prohibitions on traveling backward through time... 'closed timelike curve[s]'....David Deutsch... the paradoxes created by CTCs could be avoided at the quantum scale.... 'It's intriguing that you've got general relativity predicting these paradoxes, but then you consider them in quantum mechanical terms and the paradoxes go away', says University of Queensland physicist Tim Ralph.... Ralph and... Martin Ringbauer... imagine that a fundamental particle goes back in time to flip a switch on the particle-generating machine that created it. If the particle flips the switch, the machine emits a particle—the particle—back into the CTC; if the switch isn't flipped, the machine emits nothing.... Self-consistency in the quantum realm... any particle entering one end of a CTC must emerge at the other end with identical properties.... Ringbauer and their colleagues... polarized photons... 'encode their polarization so that the second one acts as kind of a past incarnation of the first... [the simulation] allows us to study weird evolutions normally not allowed in quantum mechanics'. Those... would have remarkable practical applications, such as breaking quantum-based cryptography through the cloning of the quantum states of fundamental particles.... 'In the presence of CTCs, quantum mechanics allows one to perform very powerful information-processing tasks, much more than we believe classical or even normal quantum computers could do'.... Deutsch's model isn’t the only one around.... Seth Lloyd... resolves the grandfather paradox using quantum teleportation and a technique called post-selection, rather than Deutsch's quantum self-consistency.... 'Deutsch's theory has a weird effect of destroying correlations... a time traveler who emerges from a Deutschian CTC enters a universe that has nothing to do with the one she exited in the future. By contrast, post-selected CTCs preserve correlations, so that the time traveler returns to the same universe that she remembers'.... This property of Lloyd's model would make CTCs much less powerful for information processing, although still far superior to what computers could achieve in typical regions of spacetime..."

Charlie Stross: Schroedinger's Kingdom: the Scottish Political Singularity Explained: "I'm here to interest you in my writing, not recruit you for my Army of Minions™.... But there's a point where politics impinges directly on the circumstances of my writing, and that's when it goes nonlinear, and by nonlinear I mean 'depending on the outcome of three upcoming elections, I may be living in one of three different countries in two years' time'.... It makes it really hard to even think about writing that next near-future Scottish police thriller when I can't predict what country it will be set in, much less what its public culture will look like or where it will be ruled from.... History happened... the Darien scheme nearly bankrupted Scotland's ruling class, and in a desperate attempt to recapitalize (with help from their peers in London) they did an abrupt U-turn on the previous century's policy of sharing a crown but not a parliament, and signed up for the Act of Union in 1707.... This was... an excellent deal for the rich landowners and the metropolitan elites of Edinburgh and Glasgow, but a terrible one for the highland poor. However, a number of anomalies remained.... This arrangement worked more or less all right for a couple of centuries. With the industrial revolution, the major cities of the English midlands, the North of England, and the Scottish lowlands prospered: their fortunes were based on shipping, trade, and manufacturing industry. London also prospered as a centre of commerce, and was a major financial hub: Edinburgh, the Scottish capital, was a secondary financial centre.... So what went wrong?... The loss of relative advantage in manufacturing industry... Margaret Thatcher.... The recession of 1979-82... was just the start of what seemed at times to be almost an undeclared civil war against the north of Britain.... [Today's] Scottish Parliament is not unconditionally sovereign. It exercises powers delegated to it by the Westminster Parliament; certain powers are reserved—policy on illegal drugs, immigration, foreign policy, defence, and taxation are exercised in Westminster.... We now have a parliament led by the SNP (a carefully-planned impossibility), a centre-left party: and an opposition consisting, in order of size, of: Scottish Labour (as reformed by Tony Blair into a right wing party with left-wing heritage), the Liberal Democrats, trailed by the Conservatives and the Greens.... It's been fairly obvious for about three decades now that there's a growing political rift between Scotland and England. England seems to be becoming more parochial, europhobic, and anti-immigrant, and the political sails of all the main English parties are being trimmed to the right.... A vote will be held on the 18th of September. If there is a majority for independence, then the constitutional shit will hit the fan because Westminster will be required to negotiate and enact the enabling legislation for Scottish independence... with a UK-wide General Election coming up in June 2015. The enabling legislation can't be rushed through before the next election (it's too big and complex), so it's going to trail into the next Westminster parliament.... So: in 2017, Scotland will either be an independent nation (initially a constitutional monarchy retaining the shared Crown, as was the case prior to 1707), or part of the UK. Why did I say there might be two different UKs? Well, that's down to UKIP and the Conservative euroskeptics.... The worst case outcome, circa 2017, is that Scotland remains manacled to an England that has voted in a government of the Home Counties, who despise the Scots, and who have successfully campaigned for a referendum in which the English protest vote determines that Scotland will be dragged out of the EU in a vain attempt to wind the clock back to an imaginary vision of a 1950s conservative utopia that never was. Or Scotland might remain part of a UK, but one where when push came to shove the racist right took a kicking... and the softer right-wing government of New Labour is back in charge.... But in the meantime: it's impossible for me to write fiction set in the near future of Scotland until after we've navigated the political white water ahead: the referendum in September 2014, the general election in June 2015, and (optionally) the further UK referendum in 2016/17..."

Stefania D’Amico, Roger Fan, and Yuriy Kitsul: The scarcity value of Treasury collateral: Repo market effects of security-specific supply and demand factors: "In the special collateral repo market, forward agreements are security-specific, which may magnify demand and supply effects. We quantify the scarcity value of Treasury collateral by estimating the impact of security-specific demand and supply factors on the repo rates of all outstanding U.S. Treasury securities. We find an economically and statistically significant scarcity premium. This scarcity effect is quite persistent, passes through to Treasury market prices, and explains a significant portion of theflow-effects of LSAP programs, providing additional evidence for the scarcity channel of QE. Through the same mechanism, the Fed’s reverse repo operations could alleviate potential shortages of high-quality collateral."

September 9, 2014

Over at Equitable Growth: Ain't It Fun, Living in an r n+g World?: Tuesday Focus for September 9, 2014

Over at Equitable Growth:  Consider r, the required real rate of interest on government debt, and the sum of n, the labor-force growth rate, and g, the labor productivity growth rate.

Consider r, the required real rate of interest on government debt, and the sum of n, the labor-force growth rate, and g, the labor productivity growth rate.

When r > n+g, the case for budget surpluses and lowering the debt is strong. We believe that private investments are even more productive to society than the market rate of return on private capital formation tells us. We believe that there are private knowledge and other spillovers from private capital formation. We believe that the quasi-rents from past investments are shared among all those with market power who participate in production. Thus when the government borrows and spends, it crowds out private investments that are very profitable to society as a whole. This point is strengthened by the danger of a runaway government financial crisis should a default premium begin to incorporate itself into government borrowing rates. This point is limited only by intergenerational equity considerations: that if we think the future will be richer than the present, committing funds now to private capital formation rather than to private and government consumption worsens intergenerational inequality. READ MOAR

The problem is that we really do seem to be in a different world than the r > n+g world--in fact, we seem to have been in a different world since 1933. And the question of what to do when r < n+g is much harder. There are then, I think, three possibilities:

One possibility is that r < n+g is telling us that private returns from investment, when properly adjusted for risk, are truly less than the growth rate of the economy--that the economy truly is dynamically inefficient. In this case, the reduction in private capital formation from higher government debt is not a bug but a feature: the economy does have too much private capital, and less would improve welfare.

A second possibility is that private capital is still productive and valuable, but that rent-sharing by stakeholders and the inability of investors to capture knowledge externalities pushes the risk-adjusted private return on capital and thus the government borrowing rate below the total economic growth rate. In this case there is a case for adding a cost-of-crowding-out term to the benefit-cost analysis of government debt finance. But it is also important to recognize that there is no danger of a runaway government financial crisis should a default premium begin to incorporate itself into government borrowing rates.

The third--and I think by far the most likely--possibility is that the fact that r < g for the government is a byproduct of an extremely large outsized risk premium because of private financial markets' failure to mobilize the risk-bearing capacity of the public and failure to establish trust and overcome moral hazard in the credit channel. Thus more government debt provides the private sector with something that it is willing to pay through the nose for: a low-risk way to transfer purchasing power into the future.

Under such circumstances a higher government debt does not reduce but raises the amount of programmatic spending that can be sustained by any given tax share of GDP: an extra proportion (n+g-r)(D/Y) of national income is available each year for government programmatic spending or tax cuts. Plus there is the direct utility gain to debtholders for providing them with something that they value greatly. In this case, there is also (a) no reason to worry about exploding government debt and a consequent government debt crisis, (b) a relatively strong case for using the government's borrowing power to route around the private market's inability to unclog the credit channel and mobilize risk bearing capacity, hence (c) little reason to worry that government debt is crowding out important private capital formation--for, after all, the credit channel is badly clogged.

I certainly think that the evidence is sufficiently ambiguous that we should not make big and irreversible policy moves on the assumption that we do not live in an r < n+g world--particularly when, as now, the aggregate demand and return on public capital externalities from higher government spending and higher deficits look very large.

And the large long-run fiscal gap stems (a) from health-care costs exploding much faster than in other countries, and (b) from assumptions that current law provisions that restrict spending growth and raise taxes will be overturned by future congresses. It seems incoherent to say that we must do more short run damage to the economy by passing more current laws to control future deficits that can then also be overturned by future congresses.

As I look at it, there are three things not in the CBO's Alternative Fiscal Scenario that led me to think that we did not have a large long-run fiscal gap: (1) That someday, somehow, the rise in health-care costs would moderate and we would move toward the OECD average on health spending. (2) The Cadillac Tax and the resulting shift of what are now untaxed employer health benefits into the tax base. (3) The carbon tax--which will come sometime in the nest generation. It seemed to me that an AFS or a generational accounting calculation that did not include these was more a tendentious political intervention in the current debate then an honest technocratic forecast,

And, of course, after Reagan 1981 and Bush 2001 I have to believe that any laws passed that restrict long-run spending growth when Democrats have influence will be undone by laws that cut taxes in the long run when Republicans take control of the government.

The arguments for austerity or even for stabilizing the debt-to-GDP ratio thus seem to me to be very shaky. They are claims that:

Soon, very soon, r is going to rise to be greater than n+g, and much greater than n+g--but when it does we will be unable to change our fiscal policy from one appropriate for r < n+g to one appropriate for r > n+g by a substantial margin.

Even if r < n+g, there is still a social loss from the crowding-out of private capital formation that takes place when government debt is increased.

With taxes fixed as a share of GDP by political pressures, and with deficits limited by deficit phobia, a higher debt means lower programmatic spending.

(3) seems to me to be simply confused. (3) says that the present value of spending is fixed, so all that spending increases and cuts do is move spending around from decade to decade. In that case, you would want spending to be high when r is low because the amount of future spending you have to forego to stay under the tax + interest cap is low; and you would want spending to be low when r is high because they you are foregoing a lot of future spending for each dollar of spending financed by debt today. It's not an argument for not running a large deficit now, when r is low. (2) is possible, but needs to be developed more. (1) is an argument that we should not even set out what the best policy is now because our current political system is so broken that even pointing out that r < n+g will lead to destructive political economic consequences.

Liveblogging World War I: September 9, 1914: von Bulow Retreats to the Marne

From Sewell Tyng: The Campaign of the Marne:

The day of September 8th had been a particularly hard one for the French. The Ninth Army heavily engaged on its left, with its centre yielding and its right almost broken, had engaged every available battalion and no further reserves remained. In vain Foch appealed to De Langle, his neighbour to the east. The Fourth Army too was fighting a desperate battle around Vitry-le-François and had no means of lending support. The 21st Army Corps (Legrand-Girarde) which Joffre had brought from Lorraine to fill the gap between the Fourth and Ninth Armies was still ten kilometres away at nightfall.... It was at this crisis that Foch is reported to have sent his celebrated dispatch to Joffre:

Hard pressed on my right. My centre is yielding. Impossible to manoeuvre. Situation excellent. I am attacking....

During such a day there was little that an Army Commander could do... the situation at the front was changing too rapidly and the confusion was too great to permit of accurate judgements or of timely decisions from Army Headquarters; but one thing Foch could and did do—keep constantly before the combatants the decisive nature of the struggle in which they were engaged.... His subordinates... gave no thought to retreat, but kept their faces constantly towards the enemy. This was the primary object Foch had in mind.... It truly reflected his attitude during the battle, an attitude that requires no comment and that was worth an army corps to the French Ninth Army.

WHEN General von Bülow arrived at Montmort on the evening of September 8th, he was not in a happy frame of mind. He had spent most of the day at Fromentières, barely five kilometres behind the front lines, and what he had seen there had given him small ground for encouragement. Late in the afternoon, a momentary panic had given the Army Commander a few moments of serious alarm, and he had even suggested to General von Einem that it might be advisable for the II Army to retire behind the Marne. When it turned out that the disorder at the front was less important than at first reported and that the French had not taken advantage of it, he had not insisted, but it was evident to him that von Eben's two Reserve divisions had no more than a precarious hold on their positions around Montmirail in the face of greatly superior forces. The situation of the II Army's right flank especially worried Von Bülow....

The point of view von Bülow expressed to Hentsch and to the officers of the II Army staff, as they assembled at his Headquarters in the Château of Montmort:

As a result of all that we have been through and of the hard combats of the last few days the II Army has naturally lost a considerable part of its combat value. It is no longer capable of forcing a decisive victory. As a result of the transfer of two army corps from the left to the right wing of the I Army, a gap has been created which forms an immediate danger to the inner wings of both the I and II Armies. I am informed that enemy columns, brigades or divisions, are on the march into this breach, and I have no reserves left to attack the enemy or to hold him off. The enemy has two alternative courses open to him, either to turn against the left wing of the I Army or to march against the right wing of the II Army. Because of our lack of reserves, either movement might lead to a catastrophe. If the enemy compels a retreat by force of arms, the withdrawal would have to be made through a hostile country and the consequences to this Army might be incalculable. It should therefore be considered whether it would not be better, viewing the situation as a whole, to avert the danger by a voluntary concentric retreat of the I and II Armies.

As the discussion became general and continued on the basis indicated by the Army Commander, an orderly called the Chief of Staff, General von Lauenstein, to the telephone. It was von Einem of the 7th Corps, reporting the loss of Marchais-en-Brie as a result of de Maud'huy's night attack and the consequent menace to Montmirail. Forthwith, Von Bülow decided to draw back the II Army's right wing towards the east to the line Margny-Le Thoult, thereby placing it temporarily at least, beyond the danger of envelopment. The conference went on until nearly midnight, and it was decided to make no further alteration in the orders issued for the following day; the Guard to continue its offensive in conjunction with Von Hausen, while the rest of the army awaited developments. Nevertheless the trend of opinion seems to have been generally pessimistic and the view accepted that unless some way could be found to close the breach between the I and II Armies, either by the withdrawal of the I Army to the east or otherwise, a retirement behind the Marne had become inevitable.

Hentsch made no effort to combat this conception or to urge the point of view expressed the same morning by Von Moltke, Tappen and Von Dommes that no retreat was necessary. On the contrary, it seems that he fully acquiesced in what he found to be the prevailing opinion.... Late at night, as the meeting broke up, Hentsch sent a message to Von Moltke by radio: “Situation serious, but not desperate, at the II Army,” was all he thought it necessary to say. It seems incomprehensible that Hentsch should have limited himself to this brief communication, which must have seemed maddeningly cryptic to the officers at Luxembourg, so eagerly waiting for news. Between midnight and dawn an officer might readily have covered the 200 kilometres between Montmort and Luxembourg by automobile and have brought to the Chief of Staff a full report on the position of the II Army, with the views of its commander and of Hentsch himself; but no such action was deemed necessary, and except for the single sentence of Hentsch's report, the High Command received no word from the II Army on its operations during the day of September 8th.

At 5:30 the following morning, September 9th, Hentsch again conferred with Von Lauenstein and Matthes, to canvass the situation in the light of the night's reports from the front. The Chief of Staff expressed his belief that the II Army could hold its ground only provided the I Army was able to disengage itself from its battle against Maunoury and could retreat eastward, along the north bank of the Marne, far enough to effect a junction with the left wing of Von Bülow's Army. All concurred that such procedure would be difficult if not impossible, and it was determined then and there, for the safety of the II Army, that it should retire behind the Marne and ultimately behind the Vesle. It was agreed that Hentsch should proceed immediately to the Headquarters of the I Army at Mareuil-sur-Ourcq and bring about its retreat in such a direction as to close the breach existing between the two armies.

Von Bülow was not present at this early morning meeting, but there seems to have been no doubt in the minds of those present that he would ratify the conclusion reached, for Hentsch did not see him again before leaving Montmort. While Hentsch was on his way to the Headquarters of the I Army, 80 kilometres from Montmort, von Bülow confirmed von Lauenstein's decision and issued orders for the general retreat of the German II Army behind the Marne. In a laconic message he informed Von Kluck and Von Hausen:

Aviator reports four long columns marching towards the Marne. Heads at nine o'clock at Nanteuil-sur-Marne, Citry, Pavant, Nogent l'Artaud. II Army is beginning retreat, right wing Daméry.

It is of little moment to determine the exact time when the German Army Commander decided to order the retreat, though this is a matter that has been sharply debated. Whether the order came as a result of a determination that had been ripening in Von Bülow's mind since the night before—and there seem many indications that such was the case—whether it was the result of Von Lauenstein's persuasion after the latter's talk with Hentsch in the early morning, or whether it was brought about by the report of British columns approaching the Marne as indicated in von Bülow's dispatch to his colleagues, will probably never be known. The principal thing is to note that the decision was taken, and taken by the Army Commander himself. It seems quite clear, and Ludendorff's Court of Inquiry so found, that Hentsch did not order or purport to order the retreat of the German II Army.

This fact, however, hardly suffices to exonerate Hentsch from all responsibility. Knowing, as he did, the opinion of his superior, von Moltke, and of his colleagues, Tappen and von Dommes, the conclusion is inescapable that Hentsch agreed too readily in the view taken by the commander and the Chief of Staff of the II Army, without making any serious effort to impress upon them the point of view of the High Command. It seems certain that Hentsch was personally convinced that the part of wisdom required the retreat of the II Army. Nevertheless, with knowledge that other views prevailed at Luxembourg, he should at least have made every effort to present these views fully to the II Army Commander, and conversely the views of the II Army to the Chief of Staff, before acquiescing in so momentous a decision. By failing to do so, and by yielding too readily to his personal convictions, Hentsch performed less than his full duty. Whatever the faults of von Moltke during the Campaign of the Marne, he cannot fairly be charged with having initiated the retreat of theR German armies, for Hentsch did not communicate again with Luxembourg until he sent a radio from Fismes in the middle of the afternoon of September 9th, after both the I and II Armies had begun their retirement, and von Bülow himself did not inform the High Command of his decision until the movement of the II Army had started beyond possibility of recall.

The wisdom of the retreat of the II Army, which entailed within a few hours that of its neighbours to the right and left, must be judged objectively, apart from the manner in which it was done and from the reasons alleged in justification after the event. Von Bülow's decision has been generally denounced by German military critics and soldiers, who have almost unanimously taken the position that he regarded the situation on the morning of September 9th with undue pessimism and that nothing warranted his determination. The German thesis is based on the assumption that the right wing of the German II Army, after its withdrawal to the line Margny-Le Thoult, had nothing to fear from the enemy, and that its left wing, with von Hausen's three divisions, was on the verge of inflicting a decisive defeat on Foch, while von Kluck was similarly about to bring his battle against Maunoury to a decisively victorious conclusion.