Richard L. DeProspo's Blog, page 7

June 9, 2015

NJ Supreme Court Rules on Public Pension Funding

In a surprise move of the New Jersey Supreme Court this morning, the court overruled a lower court decision that required Governor Chris Christie to fully fund deposits to the state pension funds, previously cut by the Governor in his annual budget. Last year, the Governor cut $1.5 billion in funding for pensions from his proposed budget, causing state labor unions to sue for restitution. The unions argued that the Governor was compelled to provide the funding as part of a negotiated settlement with the unions in 2011.

Today's decision reverses the lower court action, with the State Supreme Court ruling that the Debt Limitation Clause of the State Constitution does not recognize or support a multi-year binding commitment to fund public employee pensions, as so argued by the unions and upheld by the lower court. While this ruling may give the state some interim budget relief, it's pension funding obligations remain daunting.

In 2014, the State provided just under $700 million in cash contributions to its employee pension fund. An additional $2.8 billion was spent on employee health care benefits. The total of roughly $3.5 billion represents more than 10% of state budgeted expenses for the year. Despite this significant investment in shoring up its benefit plans, the state will still underfund its statutory annual funding obligations by nearly $3 billion.

To fully fund its requirement, just to keep pace with current accrued pension costs - and with no effort to catch up on prior underfunding - would require $6.5 billion. The state now faces a $90 billion shortfall in its employee benefits funding - $37 billion in pension costs and $53 billion in unfunded health benefits - three times the size of the state budget.

Today's decision reverses the lower court action, with the State Supreme Court ruling that the Debt Limitation Clause of the State Constitution does not recognize or support a multi-year binding commitment to fund public employee pensions, as so argued by the unions and upheld by the lower court. While this ruling may give the state some interim budget relief, it's pension funding obligations remain daunting.

In 2014, the State provided just under $700 million in cash contributions to its employee pension fund. An additional $2.8 billion was spent on employee health care benefits. The total of roughly $3.5 billion represents more than 10% of state budgeted expenses for the year. Despite this significant investment in shoring up its benefit plans, the state will still underfund its statutory annual funding obligations by nearly $3 billion.

To fully fund its requirement, just to keep pace with current accrued pension costs - and with no effort to catch up on prior underfunding - would require $6.5 billion. The state now faces a $90 billion shortfall in its employee benefits funding - $37 billion in pension costs and $53 billion in unfunded health benefits - three times the size of the state budget.

June 5, 2015

New GAO Study on Underfunded Retirement Savings

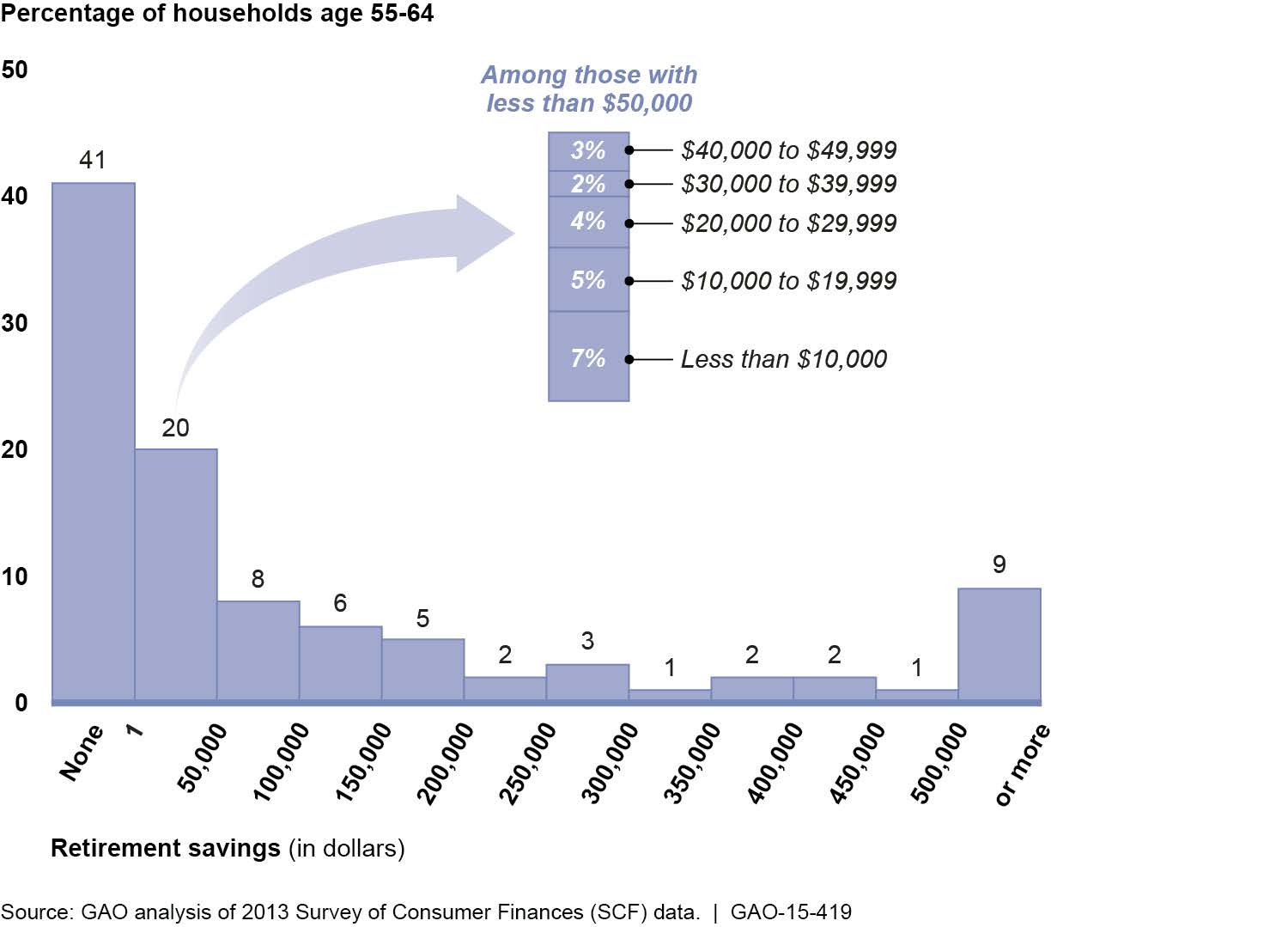

The Government Accounting Office just released a new report on retirement security. Their conclusion: most households approaching retirement have very low savings. Just how low, though, is startling. Among households age 55 and older, one-half have no retirement savings at all in 401(K), IRA or similar defined contribution accounts. Similar findings were reported in a 2013 study of the Federal Reserve Bank, along with the fact that for those age 55 and older that do have retirement accounts, the median balance was just $111,000.

The GAO study, however, also found that 29% of respondents had neither funded retirement accounts nor any employer-sponsored defined benefit plan coverage. Of this group, 41% do not own a home, while an additional 24% own a home with some level of mortgage indebtedness outstanding. For this population, social security, with a median benefit of $15,000 per year, may provide their only means of support in the years ahead. The US Census Bureau estimates that there are currently 40 million Americans aged 65 and older, with this population growing by 10,000 each day. By 2030, an estimated 65 million Americans will have reached retirement age. If 29% are projected to live on a median Social Security income of $15,000 per year (and with Social Security by the Social Security Administration's own projections to become insolvent by 2033) America may soon look like a very different place.

As you might have guessed, the data is no better for younger generations. According to a Harris Poll in 2011, an amazing 32% of the members of Generation X, aged 34-45, reported no personal savings whatsoever. In a recent report of Allianz, 84% of Gen X reports that they see traditional retirement as a romantic fantasy of the past (see post below).

What was most interesting about the GAO report was the distribution of retirement savings among households 55-64. While 41% reported no savings and 20% with savings of less than $50,000, it was the distribution of retirement savings of higher level savers that showed some intriguing patterns. While 9% of the group surveyed showed total savings between $250,000 - $500,000, an additional 9% or an equal number as in the prior group, showed total savings of greater than $500,000. Unfortunately, it's only this latter group, or 9% of those surveyed, that will have much chance of funding a comfortable retirement through 401(k), IRA and similar defined contribution savings plans. The full chart is provided below.

The GAO study, however, also found that 29% of respondents had neither funded retirement accounts nor any employer-sponsored defined benefit plan coverage. Of this group, 41% do not own a home, while an additional 24% own a home with some level of mortgage indebtedness outstanding. For this population, social security, with a median benefit of $15,000 per year, may provide their only means of support in the years ahead. The US Census Bureau estimates that there are currently 40 million Americans aged 65 and older, with this population growing by 10,000 each day. By 2030, an estimated 65 million Americans will have reached retirement age. If 29% are projected to live on a median Social Security income of $15,000 per year (and with Social Security by the Social Security Administration's own projections to become insolvent by 2033) America may soon look like a very different place.

As you might have guessed, the data is no better for younger generations. According to a Harris Poll in 2011, an amazing 32% of the members of Generation X, aged 34-45, reported no personal savings whatsoever. In a recent report of Allianz, 84% of Gen X reports that they see traditional retirement as a romantic fantasy of the past (see post below).

What was most interesting about the GAO report was the distribution of retirement savings among households 55-64. While 41% reported no savings and 20% with savings of less than $50,000, it was the distribution of retirement savings of higher level savers that showed some intriguing patterns. While 9% of the group surveyed showed total savings between $250,000 - $500,000, an additional 9% or an equal number as in the prior group, showed total savings of greater than $500,000. Unfortunately, it's only this latter group, or 9% of those surveyed, that will have much chance of funding a comfortable retirement through 401(k), IRA and similar defined contribution savings plans. The full chart is provided below.