The depreciation of the mark of 1914-23, which is the subject of this work, is one of the outstanding episodes in the history of the twentieth century. Not only by reason of its magnitude but also by reason of its effects, it looms large on our horizon. It was the most colossal thing of its kind in and, next probably to the Great War itself, it must bear responsibility for many of the political and economic difficulties of our generation. It destroyed the wealth of the more solid elements in German and it left behind a moral and economic disequilibrium, apt breeding ground for the disasters which have followed. Hitler is the foster-child of the inflation. The financial convulsions of the Great Depression were, in part at least, the product of the distortions of the system of international borrowing and lending to which its ravages had given rise. If we are to understand correctly the present position of Europe, we must not neglect the study of the great German inflation. If we are to plan for greater stability in the future, we must learn to avoid the mistakes from which it sprang. There is another reason why the history of this episode is peculiarly significant to students of the social sciences. Accidents to the body politic, like accidents to the physical body, often permit observations of a kind which would not be possible under normal conditions. In peaceful times we may speculate concerning the consequences of violent change. But we are naturally precluded from verifying our we cannot upset the smooth current of things for the advancement of abstract knowledge. But when disturbance takes place, it is sometimes possible to snatch good from evil and to obtain insight into the working of processes which are normally concealed. No doubt there are dangers here. We must not ignore the possibility that the processes thus revealed are themselves we must not infer, for instance, that propositions which apply to large inflations necessarily apply, without modification, to small inflations. But the dangers are it is net difficult to keep them in mind and to guard against them. And the opportunities of fruitful research are enormous. In this matter of the depreciation of the mark, there is hardly any branch of the theory of economic dynamics which is not illuminated by examination of its grim events. For both these reasons, therefore, I hope that this book will obtain a wide circulation among the English-speaking public.

Yesterday, in Portugal, the inflation level has reached the 8% (29 years gone by when it was at that level). While in the euro zone it's at the 8.1% level.

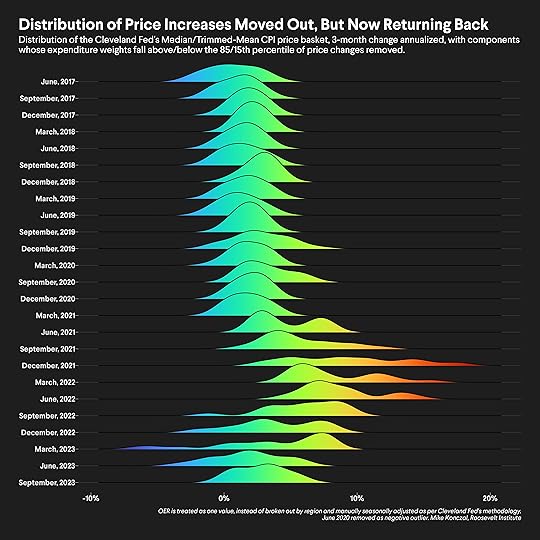

I've recently watched an interview with a former BoE governor* who warns that a "very unpleasant period" may be approaching. He recalled: (1) In the 1970s inflation was at 25% and it wrecked the economy; (2) in 1980s it was tried to target the behavior of money, and a method of exchange-rate to bring inflation down; (3) in the early 1990s there was a deep recession; (4) on September 1992 the UK left the exchange rate mechanism and introduced an inflation target; (5) the BoE was fully independent in 1997; inflation came down, and stayed at 2%, "ever since", said the former governor. But then came the Pandemics and, for example, the USA started printing money at a huge rate, more than any time before.

Now we have the war in Ukraine, ...and energy prices soaring, namely. Post war Germany and 1914 are timely topics to go back to.

"Germany’s monetary experiences have been interpreted in many ways. Some have seen in them a confirmation of the Quantity Theory of Money. Others have maintained that actually the experience of Germany and other countries during the great inflation showed that the quantity theory is not logically satisfactory for the interpretation of concrete facts, but rather that it leads to erroneous conclusions"

"It seems that certain critics of the quantity theory have not grasped the fundamental conception on which this theory is based. It is as follows: the limitation of the quantity of money is necessary for the stability of the price structure." (Page 402 of the book)

The minutiae of the analysis is so great, so detailed, for the time periods under discussion, that the book is highly recommended for fiat-money adepts.

UPDATE (ABOUT INFLATION IN THE US AND Progressive mistakes)

"I think I was wrong then about the path that inflation would take,” Treasury Secretary Janet Yellen

"The long-term driver of inflation, and the reason we have so much inflation, is the fact that we printed six and a half trillion dollars in 48 months and grew the money supply by 40%." In: https://www.newsweek.com/fed-created-...

UPDATE

“Inflation in Europe has reached a 50 year high, emblematic of the collapse of the currency and contraction of the economy. There is no simple cure for the disease of stagflation, but #Bitcoin remains the best therapeutic.” Michael Saylor tweet, 31st of May.

"With USD prices increasing at the most rapid rate in 40 years, the @POTUS and @FederalReserve have both declared a "laser focus on addressing inflation", joining the ranks of the #Bitcoin community, laser focused on inflation since January 3, 2009." Michael Saylor tweet, 1st June 2022

UPDATE

"The Cost of Wishful Thinking on Inflation Is Going Up Too First it wasn’t real. Then it was ‘transitory.’ Now we’re told the Fed will cure it with a few rate hikes." in: https://www.wsj.com/articles/inflatio...

UPDATE

So says Ben Bernanke in his recent Essay. (Time won't go back...wards. It seems.)

UPDATE

"It is not so simple. The ECB can’t print money without stoking inflation."

"We're 13 days away from an absolute explosion on inflation [in the USA]" June 17th, Frank Lunz, pollster and political analyst

UPDATE

It's official in Europe: the USA economy entered a technical recession. But for some in the USA that's not true.🤔

UPDATE

"The annual inflation rate came in at 8.3%,” said CBS interviewer Scott Pelley. “The stock market nosedived. People are shocked by their grocery bills. What can you do better and faster?" "Well,” Biden responded, “first of all, let's put this in perspective. Inflation rate month to month was just an inch, hardly at all." in: "Joe Biden lives in a world of alternative facts" by Washington Examiner September 21, 2022

"People have been reluctant to call this. But the data really want to tell us that inflation has very nearly normalized." Paul Krugman on X 13th October 2023

The book is highly technical -- and I doubt I need to read more of it at this state, so I've moved it into the read column, The basic premises are fairly set out at the outset.

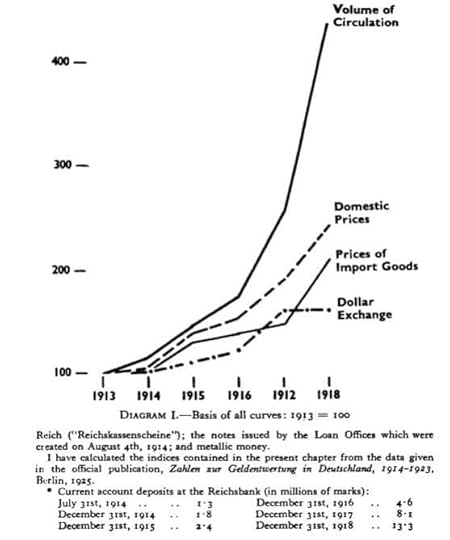

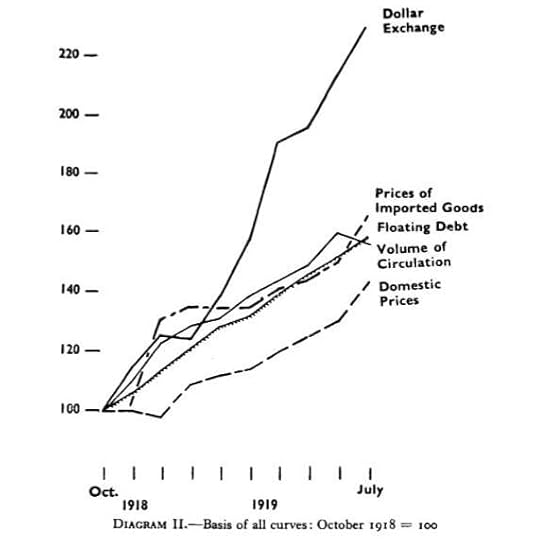

(as an addendum, I should add the following: B.-T. shows that the deficit, which began during the war, led to the printing of money which led to the depreciation. The growth of notes in circulation preceded the rise in prices by some period of time -- and there were fits and starts and stages in the process during which now circulation increased, now prices increased, or during which external and internal prices rose at very different rates. Those who few reparations as the cause of the inflation, by contrast, have always argued that it was the need to pay the Allied demands, which had to be met either in Gold or by forex, that forced Germany to print huge stores of mark notes -- and which thereby led to the depreciation. This claim is, as I note below, demonstrably false.)

Dense, learned, serious, intelligent -- utterly clear for those who have sufficient depth of understanding regarding monetary mechanisms and financial markets -- this book (highly recommended by Marc Faber) offers the definitive refutation of the myth that hyperinflation in Weimar was the result of Versailles and Reparations. This claim about Versailles and reparations, hysterically proclaimed by the Germans even before the ink was dry -- and by German and Nazi apologists ever since -- is here exploded.

Bresciani-Turroni, an Italian who worked on various economic/inflation boards during the period in question, and who thereby had a first-hand as well as an academic knowledge of the issues in play, shows that the depreciation of the mark was a result of the collapse in the current account (that is, a budget deficit) which went negative during the War -- when Germany embarked on an unprovoked campaign for world domination which they could not pay for, financed with debt -- which eventually had to be monitized when there were no longer international buyers to be found for it -- but which they themselves believed and planned to fund by raping the occupation territories in the West and especially in the East -- the early version of Lebensraum.

Moreover, as Bresciani-Turroni demonstrates, it was the Right in Germany -- and the Nationalists -- who prevented the Govt. from balancing its books by opposing EVERY scheme to raise revenue through taxation (which obviously would hit the wealthy).

For more about this issue, including a fascinating account of how Versailles failed precisely because it was too MILD -- see the remarkable and brilliant discussion in MacGregor Knox, To the Threshold of Power, 1922/33, vol. I, pp. 235-243... a truly stunning chapter.

As we move into the Great Inflation of the 21st Century... one will hear a lot about Weimar, reparations -- the poor Germans who were beaten down by British and 'international' 'banker' interests (n.b. the code words...), and Bresciani-Turroni's classic study of the inflation in 1914-1923 will be the perfect answer to them..., if only people will read it....

For those not quite up to the challenge of reading a book of THIS sort, I recommend reading Faber's Tomorow's Gold and David Hackett Fischer's The Great Wave -- both of which are important, deeply informed, fascinating, compulsively readable (imo), and sound...

I put off reading this book for a long time. It was written in 1931 and seemed rather dry. The key to getting the most out of it (for me) was to simply return to the TOC any time the writing veered into something that would be less universal and pick it back up at the next meaningful part.

It is actually a great book. I had always heard it was money printing to pay reparations from the Treaty of Versailles which created the inflation. But Germany had borrowed and printed heavily to wage the war, to the point where before the treaty was signed they were already running a 10 billion mark deficit. After the loss of Upper Silesia, the die seemed to have been cast.

The main takeaway (only my impression which may of course be incorrect) is that overspending leads increasingly to bad downstream options. Taking on debt to wage war created a cascade. The country ends WWI in physically bad shape, with the war debt overhang, and then gets the reparations penalty. They print more marks to both inflate away some of the debt and to make sure there is adequate cash in circulation (since much was leaving in repayments). But if people expect the printing to continue it becomes a self-fulfilling prophesy that destroys value in some places (purchasing power) while creating it in others (exports).

The biggest problem with money printing is there is no way to hold variables constant. They are all covariant, but not in the same direction.

One of the most interesting tidbits was about a man named Jacob Michael. When inflation hit most people reasoned that they would be better off owning physical assets. Michael's gutsy bet was that while people were getting out of marks, they would eventually be liquid capital constrained, so he sold shares and sat on cash, which he eventually loaned at high interest rates, earning a fortune in the process.

The biggest lesson for me was how inescapably complex fiscal and monetary policy is, and how much the market's expectations about central bank behavior plus mass psychology can lead to massive volatility. Given the inflation we've seen in the past year, it is a timely read.