Rahul Deodhar's Blog, page 23

July 19, 2011

Challenges of Journalism (chapter from my book)

The recent News of the World scandal left me dejected. The rot in media has reached epidemic proportions.

Amongst all the institutions in a democracy, media has the most powerful role. It is not a pillar of democracy without reason. It is an active observer of the world. It is, to a degree, omnipresent. Therefore, it often acts as eyes and ears of the law enforcement setup. Media is not impartial. It is partial to the public interest and public interest alone. But the foremost role of media is in its ability to view the world through the changing social lens. It has the power and knowledge to debate the changing values and, to a certain degree, influence the course of the society. It is unfortunate that media has failed us.

The revival of journalism must start with examination of its shortcomings. The very definition of journalist is no longer clear.

Who is a journalist?

Journalist clearly does not refer to employees of media institutions. It would be unfortunate to call celebrity experts as journalists. (The term celebrity expert refers to those people who specialise in affairs and the private life of celebrities. It does not refer to experts who are celebrities.) Neither should sports reporters be called journalists. In today's context, some of the real journalists are simply bloggers. It was never more important to define journalists than today. Journalist should be defined as agent who furthers the principles of the democratic system we discussed earlier. Only journalists should be allowed the privileges embedded in the democratic setup. Thus, in my view, News of the World should not get journalistic priviledges. It should be treated differently.

Social connectedness of journalists

The degree of separation between journalists and any individual should be as low as possible. It should be closer to one. Unfortunately, the journalists of today are no longer connected to individuals and their issues. That is why we need celebrities to further genuine causes like planting trees etc. It is imperative that journalists go closer to the individuals and communities.

Focus on speed

The other factor ailing journalism is the focus on speed. That takes away any opportunity for in-depth analysis. Top newspapers are shifting to a two-step approach, journalists usually report the facts on the ground and the section editor thereafter goes through with in-depth analysis.

This model is well developed in financial media. There, providers like Bloomberg, Reuters provide data at varying frequency while the teams of analysts from various brokerages analyze the data and provide the expert perspective.

While I understand the motivation behind this setup, I think it is inadequate. Journalists, in certain cases, operate more like detectives and there is nothing to replace real evidence. Even financial analysts regularly meet with companies and validate the information they receive from data sources.

Further, journalists are more than detectives. They have to sniff out stories where there is no report of a crime. This requires, what experts call, "nose for the job". The depth of journalism, at least in such analytical stories, suffers to a great extent.

Journalists need an aggregator of facts

In the context of current problems, media should at least function as an aggregator of facts and data. Here we refer to media as separate from journalism. The journalists, even if external to such organisations, may be able to mine the data and evolve their analysis. These facts, once established, should be available in public domain. It should be possible to augment and improve them through subsequent fact-finding missions by other media employees.

Journalists, in such a scenario, are moving away from traditional media hierarchy. We need to create recognition for this new breed of journalists.

Problem of continuity

Journalism requires longer follow-ups, particularly for important issues like WTO negotiations, carbon emissions, financial crisis etc. As the events continue to unfold the scope, severity and depth of investigation and understanding changes. Journalists today, are not able to follow through with their stories. In a way, it is easy to follow the scandals of top sportsman or politicians. However, the important debates, related to US healthcare, foreign policies etc, are very difficult to follow.

Popular bloggers, with their subject focus, are able to do a better job at following stories with arguments as commentary. The quality of discussion is enriched. It is probably the reason why top journalists now have their own blogs.

Imperatives

It is critical to design a system where journalists are able to work for the democratic system and further its goal. The system should start by redefining what journalism is supposed to be at its core. Such a system may be actually evolving as a network of bloggers, but it needs to be nurtured and expanded. Further, the current model of subsidising journalists with revenues from corporates or entertainment will not be enough to sustain this key pillar of democracy.

From my book Subverting Capitalism and Democracy - chapter titled Challenges of Journalism

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

July 15, 2011

Global Realignment of Economic Power

Just days before I was thinking how this feels like pre-Bear Sterns days and today Yves Smith has a post titled Shades of 2007. It indeed does feel like it. In a way, there is nothing new. We know how it will end.

However, I fear there is more coming. Something more interesting that we haven't really thought about.

I believe, soon we should enter an era of realignment of economic power. We tend to believe the west is generally rich. But it may soon change. As the screws of austerity will tighten across EU and even the US, the developed world may realize that they are not so rich after all.

To say that such a realignment will be challenging will be an understatement. We will have to evaluate the correct value of each currency, rework the location of manufacturing capacities and realize that the savers of the world will be real demand drivers of global consumption. The process is likely to take 2-3 decades or more.

The question that consumes me, how should we preserve and increase our wealth?

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

However, I fear there is more coming. Something more interesting that we haven't really thought about.

I believe, soon we should enter an era of realignment of economic power. We tend to believe the west is generally rich. But it may soon change. As the screws of austerity will tighten across EU and even the US, the developed world may realize that they are not so rich after all.

To say that such a realignment will be challenging will be an understatement. We will have to evaluate the correct value of each currency, rework the location of manufacturing capacities and realize that the savers of the world will be real demand drivers of global consumption. The process is likely to take 2-3 decades or more.

The question that consumes me, how should we preserve and increase our wealth?

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

July 12, 2011

Cartoon - Barack Obama secret thoughts

Obama - Secret Thoughts by Rahul Deodhar

Note: I promise to improve my sketching.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

July 6, 2011

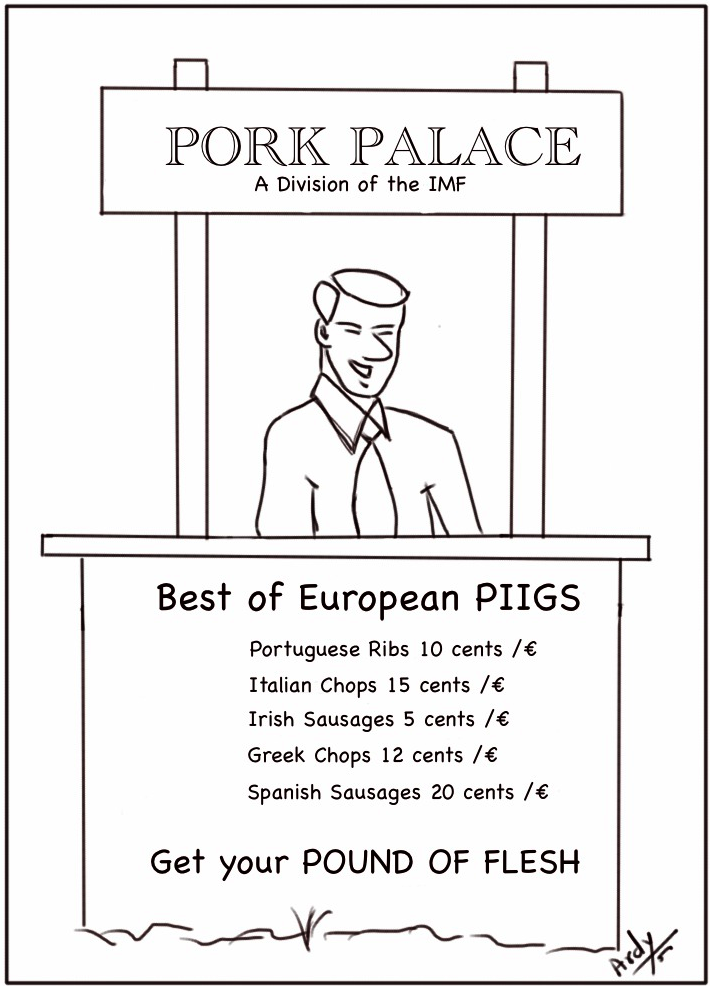

Cartoon - PIIGS

All Rights Reserved - Rahul Deodhar

July 5, 2011

Efficiency of governance

Edward Harrison at nakedcapitalism points to Slovenia going the Greek route. Slovenia, it seems, needs to cut budgetary spending and undertake pension reforms. At the slightest of such references, the right-wingers jump into the fray stating "we need a smaller government". Now you know how I hate when government modifies its promises on healthcare and pension for the old. In this case, smaller government refers to government expenditure in line with the government revenues.

Often that is reduced to lesser people employed by the government. It means less police, less hospital staff, less departments to control something-that-should-not-be-controlled, etc. In other words, smaller government often boils down to lesser governance. But it need not be if we have higher productivity of government staff.

We need to improve the efficiency of governance. A lot of duties of government have been clarified in the constitution. One, I believe, is left behind. In the constitution, it must be made clear that government must strive to lower the cost of governance. It must increase the the deliverables (governance) and reduce the burden on the tax payer (cost of governance). We have seen companies reduce cost, why can't the government? There is a distinct lack of focus on government productivity. It is time to introduce such metrics and track them over time.

I think before we talk of smaller government, let us talk of efficient government. Let us talk of increasing governance and increasing efficiency of government.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

Often that is reduced to lesser people employed by the government. It means less police, less hospital staff, less departments to control something-that-should-not-be-controlled, etc. In other words, smaller government often boils down to lesser governance. But it need not be if we have higher productivity of government staff.

We need to improve the efficiency of governance. A lot of duties of government have been clarified in the constitution. One, I believe, is left behind. In the constitution, it must be made clear that government must strive to lower the cost of governance. It must increase the the deliverables (governance) and reduce the burden on the tax payer (cost of governance). We have seen companies reduce cost, why can't the government? There is a distinct lack of focus on government productivity. It is time to introduce such metrics and track them over time.

I think before we talk of smaller government, let us talk of efficient government. Let us talk of increasing governance and increasing efficiency of government.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

July 4, 2011

The end of middle income trap

There is a lot of research about the middle income trap where the GDP of countries grows but stalls once it reaches the Middle Income group.

How the US kept its lead?The US kept its lead by being at the frontiers of development. First it was the manufacturing productivity boom of the 1900s where Henry Ford found ways to deploy labour in a new way multiplying the productivity. The next few decades was more of no-competition-post-WW1-WW2 phase that created man-power shortage. The US kept its lead by bringing the women into workforce imitating the western Europeans. Over the next few decades, US deployed economies of scale to keep productivity high. This was the dawn of the technical age with new machines aiming for quality and speed. The next phase was information age. Again US companies leading the information era created unparalleled advantage using technology.

What comes next, is the crucial question. It is not yet clear. However, what is clear is that it will definitely require more knowledge and technological input than previously. Can the silicon valley, which has delivered quite a few technological winners, give US the next advantage? The chances are getting smaller every day. But that is nothing to do with Silicon Valley itself, but the political climate in which it must operate. Stifling immigration laws that prevent talent from coming through, unfriendly tax regime that will definitely be a burden on small businesses, lack of science and math educated population and global reach of the VCs may thwart the leadership position of Silicon Valley. Further, technology now allows interactions across the globe allowing crucial connections between VCs and founders possible. There are two areas where size of investment could make a difference. These two areas would be renewal energy and water treatment.

The connection with Middle Income Trap

With the US and developed world acting as a source of demand, and simultaneously as a frontier of development, implied that middle income countries were reliant on currency valuations to ensure competitiveness. The currency strategy, it implies, were creating a ceiling for these countries in terms of incomes. Quite a few countries, like Malaysia, have little difference with US or other developed countries when it comes to actual productivity (as defined in engineering not economics). The lower economic productivity is a function on artificial factors.

I believe we are at a stage when technological edge of the developed countries is not substantial. It is possible that new developments will come from across the world and some other country, possibly China, will take a leadership role in the coming decades. As a corollary, it will escape the middle income trap. With this as an example, it will be possible for others to use similar strategy.

Developed world median-incomes may decline

Concurrently, the median incomes in the developed world, may decline upsetting the conventional benchmarks for what is classified as a middle-income-group. The current crisis, is creating ample structural shifts to hasten this process. Soon, we will see a realignment of real wealth.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

How the US kept its lead?The US kept its lead by being at the frontiers of development. First it was the manufacturing productivity boom of the 1900s where Henry Ford found ways to deploy labour in a new way multiplying the productivity. The next few decades was more of no-competition-post-WW1-WW2 phase that created man-power shortage. The US kept its lead by bringing the women into workforce imitating the western Europeans. Over the next few decades, US deployed economies of scale to keep productivity high. This was the dawn of the technical age with new machines aiming for quality and speed. The next phase was information age. Again US companies leading the information era created unparalleled advantage using technology.

What comes next, is the crucial question. It is not yet clear. However, what is clear is that it will definitely require more knowledge and technological input than previously. Can the silicon valley, which has delivered quite a few technological winners, give US the next advantage? The chances are getting smaller every day. But that is nothing to do with Silicon Valley itself, but the political climate in which it must operate. Stifling immigration laws that prevent talent from coming through, unfriendly tax regime that will definitely be a burden on small businesses, lack of science and math educated population and global reach of the VCs may thwart the leadership position of Silicon Valley. Further, technology now allows interactions across the globe allowing crucial connections between VCs and founders possible. There are two areas where size of investment could make a difference. These two areas would be renewal energy and water treatment.

The connection with Middle Income Trap

With the US and developed world acting as a source of demand, and simultaneously as a frontier of development, implied that middle income countries were reliant on currency valuations to ensure competitiveness. The currency strategy, it implies, were creating a ceiling for these countries in terms of incomes. Quite a few countries, like Malaysia, have little difference with US or other developed countries when it comes to actual productivity (as defined in engineering not economics). The lower economic productivity is a function on artificial factors.

I believe we are at a stage when technological edge of the developed countries is not substantial. It is possible that new developments will come from across the world and some other country, possibly China, will take a leadership role in the coming decades. As a corollary, it will escape the middle income trap. With this as an example, it will be possible for others to use similar strategy.

Developed world median-incomes may decline

Concurrently, the median incomes in the developed world, may decline upsetting the conventional benchmarks for what is classified as a middle-income-group. The current crisis, is creating ample structural shifts to hasten this process. Soon, we will see a realignment of real wealth.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

July 3, 2011

Does the US have enough manufacturing?

There is an interesting article on Huffington Post wherein David Henderson counters a series of posts from Ian Fletcher who argues US has less manufacturing that it needs. Overall, I am in Ian's camp but with differences. I wish to make some different argument about why US needs more manufacturing.

Manufacturing jobs vs. manufacturing output aloneFirstly, it is important to concern ourselves with manufacturing jobs rather than manufacturing output alone because jobs and employment determine the consumption level.

Let us compare two polar opposites, an economy with 100 people employed in producing 100 units of GDP output vs. an economy where 100 units of GDP output is created by 1 person with 99 unemployed. We can imagine the difference in consumption patterns of the economies.

That is why I believe, if consumption has to increase (reflecting on economy getting richer), not only does output have to increase but employment has to be high.

Low cost capital reducing employment intensity of productionThe reason why employment intensity of US manufacturing is reducing can be attributed to cheap capital. In most manufacturing activities, capital and labour are competitors. A higher capital intensity reduces labour intensity.

The relative cheap capital flood of past two decades has come to haunt the US. The easy capital has reduced the employment intensity of its manufacturing and rendered thousands unemployed. Economists will argue that these unemployed are free to engage in other value-adding activity. But that is not easy.

Job and skill matchI have always believed that the job profile of the economy should match its skill profile. A nation of plumbers will need plumbing jobs, a nation of software programmers will need IT jobs. Each nations needs jobs that match its skill profile. I think US has lower manufacturing jobs than its skill profile requires.

Skill profile can be changed, but that takes time. Adaptability to different jobs itself is a skill, a very valued one at that. How adaptable is US workforce? This question must be answered relatively. Is US workforce easier to adapt than Chinese workforce? I have my doubts.

Hence, I believe, US needs more manufacturing jobs rather than simply manufacturing.

Selling rights as opposed to assets - FDI conundrumThe other argument often looks at the capital account surplus as a counterweight to current account deficit. I would not club all the in-bound investments into one. It matters what the US is selling. Is it selling rights as against assets? I refer to rights as rival assets (parallel to rival goods) while simple assets are those with non-rival quality.

[Note: Rival assets are those assets that can be duplicated. A building can be duplicated but not a port or a road. Technically assets are always rival but we need to make distinction to understand the quality of what is being sold. We can sell factories and recreate everything. But we cannot sell ports, roads, beaches, monuments etc. and expect to recreate it. Thus what is asked of Greece is selling rights not assets.]

Thus, when we look at in-bound investments (FDI) we must look at what is being sold before we can comment if it is a fair deal.

In sumI believe Us skill profile needs more manufacturing jobs rather than simply manufacturing output. So long as jobs are taken care of, it does not matter if US has enough manufacturing or not.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

Manufacturing jobs vs. manufacturing output aloneFirstly, it is important to concern ourselves with manufacturing jobs rather than manufacturing output alone because jobs and employment determine the consumption level.

Let us compare two polar opposites, an economy with 100 people employed in producing 100 units of GDP output vs. an economy where 100 units of GDP output is created by 1 person with 99 unemployed. We can imagine the difference in consumption patterns of the economies.

That is why I believe, if consumption has to increase (reflecting on economy getting richer), not only does output have to increase but employment has to be high.

Low cost capital reducing employment intensity of productionThe reason why employment intensity of US manufacturing is reducing can be attributed to cheap capital. In most manufacturing activities, capital and labour are competitors. A higher capital intensity reduces labour intensity.

The relative cheap capital flood of past two decades has come to haunt the US. The easy capital has reduced the employment intensity of its manufacturing and rendered thousands unemployed. Economists will argue that these unemployed are free to engage in other value-adding activity. But that is not easy.

Job and skill matchI have always believed that the job profile of the economy should match its skill profile. A nation of plumbers will need plumbing jobs, a nation of software programmers will need IT jobs. Each nations needs jobs that match its skill profile. I think US has lower manufacturing jobs than its skill profile requires.

Skill profile can be changed, but that takes time. Adaptability to different jobs itself is a skill, a very valued one at that. How adaptable is US workforce? This question must be answered relatively. Is US workforce easier to adapt than Chinese workforce? I have my doubts.

Hence, I believe, US needs more manufacturing jobs rather than simply manufacturing.

Selling rights as opposed to assets - FDI conundrumThe other argument often looks at the capital account surplus as a counterweight to current account deficit. I would not club all the in-bound investments into one. It matters what the US is selling. Is it selling rights as against assets? I refer to rights as rival assets (parallel to rival goods) while simple assets are those with non-rival quality.

[Note: Rival assets are those assets that can be duplicated. A building can be duplicated but not a port or a road. Technically assets are always rival but we need to make distinction to understand the quality of what is being sold. We can sell factories and recreate everything. But we cannot sell ports, roads, beaches, monuments etc. and expect to recreate it. Thus what is asked of Greece is selling rights not assets.]

Thus, when we look at in-bound investments (FDI) we must look at what is being sold before we can comment if it is a fair deal.

In sumI believe Us skill profile needs more manufacturing jobs rather than simply manufacturing output. So long as jobs are taken care of, it does not matter if US has enough manufacturing or not.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

June 30, 2011

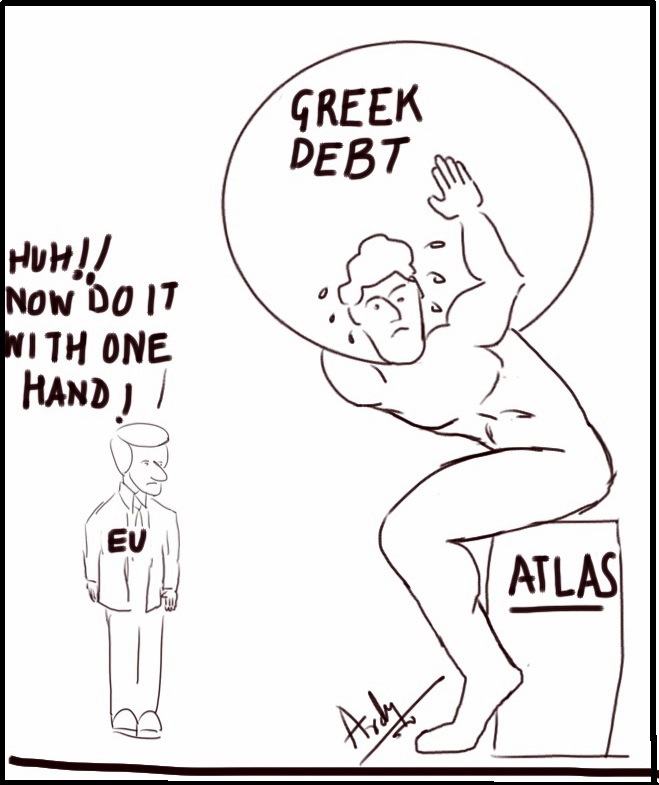

My cartoon about Greek situation

All work copyright Rahul Deodhar

All work copyright Rahul Deodhar

June 28, 2011

Curbing the exuberance in oil (& commodity) prices

The fluctuations in oil prices and commodities are creating a problem for global regulators. There is a way to make the volatility go away while allowing for liquidity. Oil prices dropped $6 as the reserves were released. If not speculation, what is this?

Reign of speculatorsPhysical delivery accounts for only ~3% of the trading that takes place. The rest of the trade is mere speculation or hedging. A lot of arguments are made about the 97% providing liquidity for the 3%. To me, that is too much liquidity. Its corollary, high liquidity means inflation, implies that prices are too high. My gut feel (no research backing) is that this figure should be ~20-30% if not more.

Compulsory deliveryNow if delivery is compulsory for these traders it will make it difficult for random speculators. But it is very difficult to create and enforce compulsory delivery mechanism. In some cases there is legitimate re-sale to other parties (high-seas sale). However, the principle can be deployed with adjustments. Let me explain this mechanism.

Hurdle costsWhat we need is to get the investor to block a percentage of capital required for storage and an annual fee for maintenance and upkeep. This will create a hurdle costs for investors. If they are legitimate investors or genuine traders then there is no extra cost as they already have infrastructure for storage and delivery.

The capital requirement will have to be deployed for each commodity or at least specific types of commodities. e.g. grains may have a single warehouse but oil and grain will have separate investments and upkeep costs.

Trading Caps within hurdle costsOnce the investor pays the capital for storage and maintenance, he creates a maximum allowed position that commodity or commodity group. Hedging may be allowed for 100% of the volume occupied.

This is beneficial for producers tooToday, producers make investment looking at commodity prices and later the prices fall, it will create huge losses. Therefore, producers are reluctant to deploy capital till they are sure the high prices are result of fundamental factors rather than speculation. Hence, oil exploration that could be viable when crude is at $80 is not undertaken till crude goes above $100 and stays there for some time. In short, producers cannot trust the prices communicated by the markets. This leads to a build up of supply side pressures creating an inflationary spiral that abruptly breaks down.

In sumSuch limits should reduce the rampant speculation. This, I believe, will allow for real markets to clear at correct prices. It will ease the burden on consumers and will correctly determine the return on investment by producers.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

Reign of speculatorsPhysical delivery accounts for only ~3% of the trading that takes place. The rest of the trade is mere speculation or hedging. A lot of arguments are made about the 97% providing liquidity for the 3%. To me, that is too much liquidity. Its corollary, high liquidity means inflation, implies that prices are too high. My gut feel (no research backing) is that this figure should be ~20-30% if not more.

Compulsory deliveryNow if delivery is compulsory for these traders it will make it difficult for random speculators. But it is very difficult to create and enforce compulsory delivery mechanism. In some cases there is legitimate re-sale to other parties (high-seas sale). However, the principle can be deployed with adjustments. Let me explain this mechanism.

Hurdle costsWhat we need is to get the investor to block a percentage of capital required for storage and an annual fee for maintenance and upkeep. This will create a hurdle costs for investors. If they are legitimate investors or genuine traders then there is no extra cost as they already have infrastructure for storage and delivery.

The capital requirement will have to be deployed for each commodity or at least specific types of commodities. e.g. grains may have a single warehouse but oil and grain will have separate investments and upkeep costs.

Trading Caps within hurdle costsOnce the investor pays the capital for storage and maintenance, he creates a maximum allowed position that commodity or commodity group. Hedging may be allowed for 100% of the volume occupied.

This is beneficial for producers tooToday, producers make investment looking at commodity prices and later the prices fall, it will create huge losses. Therefore, producers are reluctant to deploy capital till they are sure the high prices are result of fundamental factors rather than speculation. Hence, oil exploration that could be viable when crude is at $80 is not undertaken till crude goes above $100 and stays there for some time. In short, producers cannot trust the prices communicated by the markets. This leads to a build up of supply side pressures creating an inflationary spiral that abruptly breaks down.

In sumSuch limits should reduce the rampant speculation. This, I believe, will allow for real markets to clear at correct prices. It will ease the burden on consumers and will correctly determine the return on investment by producers.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.

June 27, 2011

The June uptick in Indian markets

BSE Sensex June 21-28, 2011, Google Finance

We have clocked 3 days of super-normal uptick in Indian stock markets. Just as I was not clear about what spooked the Indian markets a few days before on June 20th, I am not sure what has gone right since that time.

I think, with respect to Indian markets, we are entering a period of volatility in the Indian markets. The reasons are plenty.

First, it is now a consensus view that inflation will move to double digits soon. What is not understood is real life meaning of this stubbornly high inflation extending beyond two years now. The price acceleration that is implied by continued higher inflation will either impact corporate margins, or impact demand i.e. revenues, or both. To complicate matters further, the investment required for supply-side easing are not coming through. Corporate India is reluctant to work on their long term capacity addition plans. This is clearly not a situation where markets should be heading higher.

Second, there is impending specter of Euro-crisis going out of control. Europe is a huge market for Indian exporters. A slowdown in this area will have a shake out. Even excluding Europe, global demand picture looks soft.

Third, the recent fuel price hikes have complicated the fiscal situation. Indian fuel pricing and tax structure is needlessly complicated. The crude imports are taxed, processing is taxed, there is a sales tax and service charges. Ultimately, the whole oil business contributes substantially to the governments kitty. Any altering of the tax structure is negative for fiscal deficit which is already under stress.

All in all, there is no reason for the markets to behave as they are behaving. While I dipped a week ago at the lower points, I believe there is still down-side risks. We haven't yet completed the correction we were in.

My book "Subverting Capitalism & Democracy" is available on Amazon and Kindle.