Rahul Deodhar's Blog, page 14

January 16, 2014

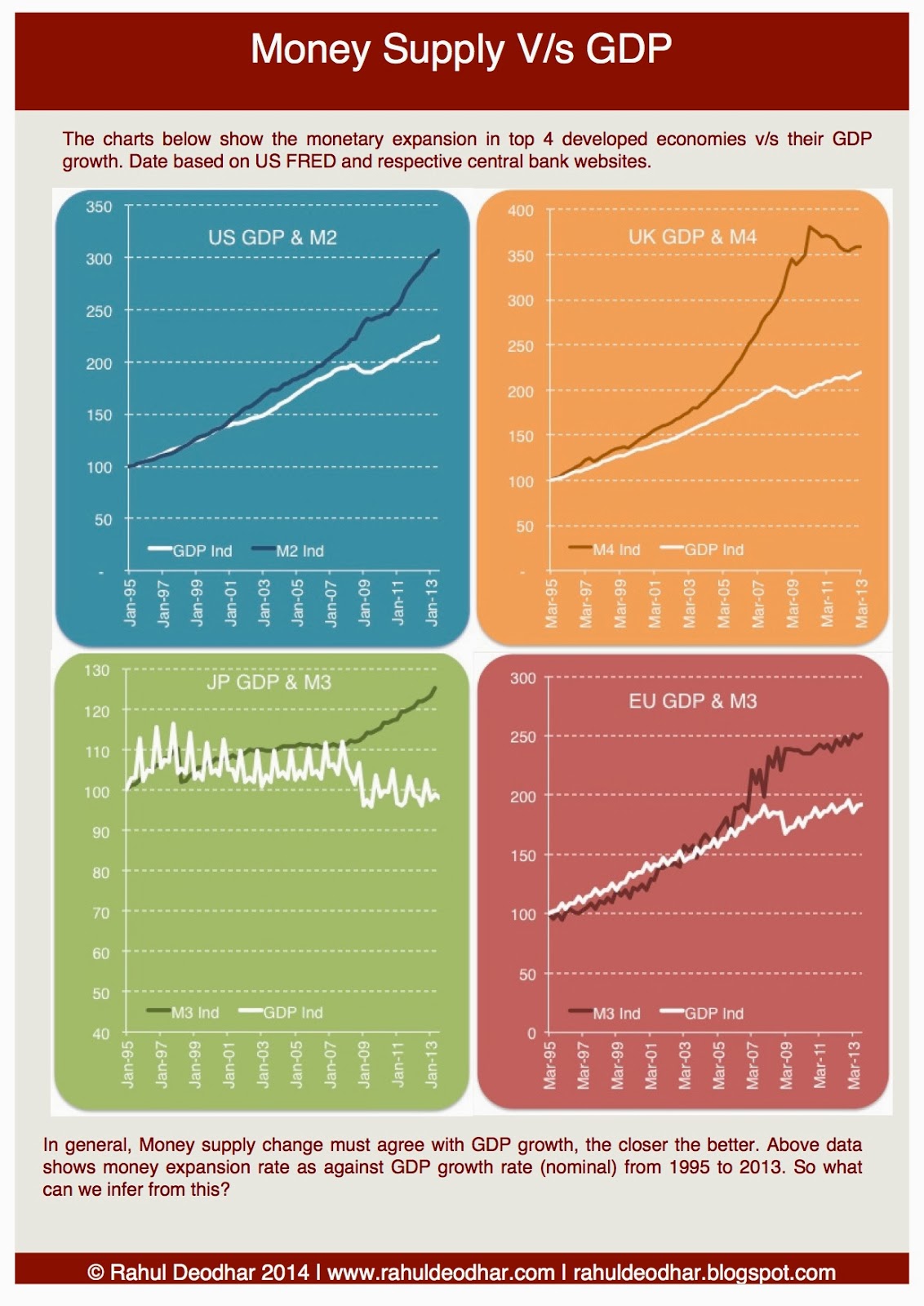

Money Supply and GDP growth

Here is a chart I made showing money supply v/s GDP growth of top 4 developed economies. Tell me what do you think about this.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

January 4, 2014

The globalization puzzle

Dani Roddick has an interesting post about globalization here : http://blogs.lse.ac.uk/politicsandpolicy/archives/38743

The essential argument is institutional in nature. The institutional development Prof. Roddick argues depends on democratic choice expressed by various countries. He therefore concludes that full globalisation is almost impossible. I beg to differ slightly.

I agree at this point in time it is difficult to achieve full globalization. However, it is neither impossible nor unlikely in the future. Prof. Roddick allows for such situation in extreme long term so I may have gotten it wrong.

I think two main forces are working towards that goal.

First internet and technology is making us realize how similar we are as peoples of the world. In older times we were skeptical of other people - they spoke different language, worshipped different gods, had different skin colour, ate different things, etc. There has been even starker change in people's perception of other counties from pre-1960s where non-western was exotic and a global traveller was a privileged person. Well, no longer is that true. We now have people interacting globally with each other across time zones and across cultures. This is a potent unifying force. We see often than this urge to communicate, trade, intermingle often crashes with the political borders and norms developed to keep peoples separate. No longer are we threatened by those of other culture.

Second the world human and environmental rights movement is creating a template for global legal alignment. The UN human rights movement is creating a lowest common denominator set of rights that countries and their people are eagerly adopting. This methodology gives us a template that can be used for developing set of common rights which can expand gradually.

Of course there needs to be a certain convergence between economic development of various countries to make it easier. But this convergence is not as strict a requirement as it was before the internet era. Today the world is truly and rightly coming closer into a global village. And I sure hope this happens in my lifetime.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

The essential argument is institutional in nature. The institutional development Prof. Roddick argues depends on democratic choice expressed by various countries. He therefore concludes that full globalisation is almost impossible. I beg to differ slightly.

I agree at this point in time it is difficult to achieve full globalization. However, it is neither impossible nor unlikely in the future. Prof. Roddick allows for such situation in extreme long term so I may have gotten it wrong.

I think two main forces are working towards that goal.

First internet and technology is making us realize how similar we are as peoples of the world. In older times we were skeptical of other people - they spoke different language, worshipped different gods, had different skin colour, ate different things, etc. There has been even starker change in people's perception of other counties from pre-1960s where non-western was exotic and a global traveller was a privileged person. Well, no longer is that true. We now have people interacting globally with each other across time zones and across cultures. This is a potent unifying force. We see often than this urge to communicate, trade, intermingle often crashes with the political borders and norms developed to keep peoples separate. No longer are we threatened by those of other culture.

Second the world human and environmental rights movement is creating a template for global legal alignment. The UN human rights movement is creating a lowest common denominator set of rights that countries and their people are eagerly adopting. This methodology gives us a template that can be used for developing set of common rights which can expand gradually.

Of course there needs to be a certain convergence between economic development of various countries to make it easier. But this convergence is not as strict a requirement as it was before the internet era. Today the world is truly and rightly coming closer into a global village. And I sure hope this happens in my lifetime.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

December 27, 2013

NIFTY in 2013 chart

The Nifty over in 2013 did something expected - it did three peak- two troughs ~ 2.5 cycles in one year as shown in the chart below.

NIFTY over 2013 calendar (Bloomberg.com)

NIFTY over 2013 calendar (Bloomberg.com)Following are the interesting points to note:

Firstly, the amplitude of the first cycle is smaller than second cycle. I see this increasing over the next year. Thus, in 2014, Nifty will have at least 2.5 cycles each with amplitude at least as much as the second cycle of 2013. It means a lot of volatility which is positive or negative depending on how you look at it.

Secondly, the time between the two cycles is quite small and there was a muted volatility (bearish lull between End Jan to Mid April and bullish lull between end oct to Dec). I see this muted periods getting compressed. In effect we may have crudely speaking one more cycle in 2014.

Thirdly, if you see the underlying macro/micro data it has generally worsened over this period though we are near to all time highs. It is quite parallel to US equity markets.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

December 14, 2013

Irrational Exuberance in Asia - Ghosts of Greenspan in India and China

William Pesek writes an interesting column about easy monetary policies (relatively) in Asia. The central point in the article is that there is a distinct need for reform in Asia; the reform is structural - fiscal and political in nature; the reform is ignored and monetary policy is being used to boost "sentiment"; this cannot last.

I agree with the undertone of the article though there are few distinctions I would draw:

The outline of reform in Asia Ex-Japan is well known. It is a well-trodden path by the developed economies. What is lacking is either the political will or weaker systems that need reform.For political will there has to be some margin in growth. This margin was afforded by a developed country demand for developing country goods.The other reason Central bankers of developing countries are a bit easy with the punch-bowl refills is because the principle strategy for growth is by tagging on to the developed country band-wagon and compete on differentials. This strategy requires competitive exchange rate mechanisms while maintaining investment-ability in countries assets.The so-called monetary tightness / monetary reform have been triggered by either of these two requirements.Thus, central bankers must keep relative position with developed country monetary policy and amongst each other. Thus if one developing country does QE then it becomes imperative for others to follow in order to maintain export competitiveness.Changing track from this strategy is difficult during good times and becomes almost impossible when the developed markets are going through a weak economic growth phase.Even Japan is attached to this strategy.Thus the irrational exuberance carries forward from US monetary policy. It cannot be attributed to developing countries. What can be blamed on developing countries is their lack of will to develop an alternative model that can sustain the dreams and aspirations of their peoples.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

I agree with the undertone of the article though there are few distinctions I would draw:

The outline of reform in Asia Ex-Japan is well known. It is a well-trodden path by the developed economies. What is lacking is either the political will or weaker systems that need reform.For political will there has to be some margin in growth. This margin was afforded by a developed country demand for developing country goods.The other reason Central bankers of developing countries are a bit easy with the punch-bowl refills is because the principle strategy for growth is by tagging on to the developed country band-wagon and compete on differentials. This strategy requires competitive exchange rate mechanisms while maintaining investment-ability in countries assets.The so-called monetary tightness / monetary reform have been triggered by either of these two requirements.Thus, central bankers must keep relative position with developed country monetary policy and amongst each other. Thus if one developing country does QE then it becomes imperative for others to follow in order to maintain export competitiveness.Changing track from this strategy is difficult during good times and becomes almost impossible when the developed markets are going through a weak economic growth phase.Even Japan is attached to this strategy.Thus the irrational exuberance carries forward from US monetary policy. It cannot be attributed to developing countries. What can be blamed on developing countries is their lack of will to develop an alternative model that can sustain the dreams and aspirations of their peoples.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

December 12, 2013

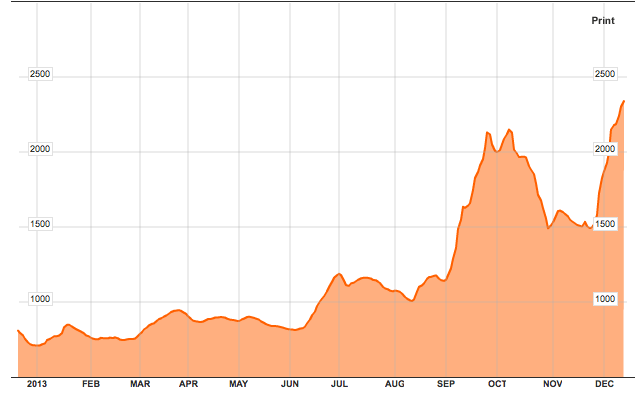

Baltic Dry Index's positive prediction

Have a look at the following chart of the Baltic Dry Index.

I am particularly enthused about BDIY's recent uptick. BDIY was a very strong indicator of Global Trade and economic strength before it lost a bit of credibility in the post-Lehman crisis. The reason I am excited is this:

Shipping industry went through one of the most intensive asset building phase between 2006-2010 with almost double the DWT built as was existing.This industry-specific weakness was coupled with economic weakness stemming from the global financial crisis.The Oil-accumulation during post-Lehman phase provided some respite but it tarnished the image of BDIY as predictor of economic performance.I think the disturbances in BDIY are past us and its present uptick does bore well for us. This means it is time to dip your toes into shipping cos. In India I would go with Shipping Corp [which I have from the previous high :(], Great Eastern Shipping. These companies should benefit from the Iran-Iraq Oil deal.

We need to watch for any global weakness and potential head-and-shoulder formation as happened in 2010.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

I am particularly enthused about BDIY's recent uptick. BDIY was a very strong indicator of Global Trade and economic strength before it lost a bit of credibility in the post-Lehman crisis. The reason I am excited is this:

Shipping industry went through one of the most intensive asset building phase between 2006-2010 with almost double the DWT built as was existing.This industry-specific weakness was coupled with economic weakness stemming from the global financial crisis.The Oil-accumulation during post-Lehman phase provided some respite but it tarnished the image of BDIY as predictor of economic performance.I think the disturbances in BDIY are past us and its present uptick does bore well for us. This means it is time to dip your toes into shipping cos. In India I would go with Shipping Corp [which I have from the previous high :(], Great Eastern Shipping. These companies should benefit from the Iran-Iraq Oil deal.

We need to watch for any global weakness and potential head-and-shoulder formation as happened in 2010.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

December 11, 2013

2014: Images from the Crystal Ball

It is that time of the year again when I take my crystal ball and peer into the future. So lets get going.

The hand that Yellen playsI think overall theme of 2014 will be determined by the hand that the US Fed plays over the first two quarters. There are two reasons why I say that. Firstly, Janet Yellen is clearly from the Bernanke School and people expect the QE -based easy monetary policy will continue. Secondly, contra the above Yellen is talking about modifying the nature of QE to be more directed and precise. I think that is full of risks which market has not fully understood as yet.

QE till eternity? Almost!One thing is clear you cannot have QE taper till you have sustainable employment with a visibility over say a 10-15 year period AND reasonably deleveraged US household. Once that is achieved then you can consider a talk of taper and the resulting volatility will be allayed by stronger household balance sheets and things can progress from thereon. So in effect the following things must happen:Employment must reach about 95% of the workforce. It should be reasonably certain employment.Ideally, US need to see emergence of a new industry which has three characteristics - first it fits with the US competitive character; second, it is a mass employer employing relatively lower skilled people and third it has second order, third order effects. Most likely that industry could be in renewable energy or water conservation space.There must be a reasonable clearing of Household debts and households must be reasonable deleveraged with margin to take on more debt if required.But it won't happen in 2014

To gather up that kind of employment we need a Fiscal side action. A national overhaul of US infrastructure will raise my hopes though it does not promise the sustainable employment for at least 15 years. But it is a fair shot to say the least. The current Fiscal policy is far too short of any meaningful contribution in this regard.

Will QE lead to a US Inflation?The whole idea of stimulus is that money will flow through the channel to the places where it can create value- therefore GDP growth- therefore jobs and this cycle will pull the economy out of the doldrums. Today the situation is different.

First it is difficult to keep injected money within the territorial borders to create the desired effect. This means two things. First the quantum of stimulus required will be far larger considering the wastage. Second, the problems of world have bearing on the quantum.

Second the mechanism of money flow or money flow channel is not functional so you cannot get the flow to the lower rungs (i.e. from asset investors to asset owners). That implies that the money is sloshing into restricted space. It is spilling into global asset classes searching for a channel to reach the bottom. (EM equities being one of them).

There are two things that must happen before the money starts getting channelized properly. You need and investable industry to crop up. And not any industry will do - it must employ relatively lower skilled people in large numbers. When we find such an industry (as a few are being experimented with) we will see money being rapidly absorbed.The current uncertainty of weak institutions collapsing must go away as in early investment stages any industry is quite vulnerable and ours will be no different. When there is adequate certainty that the weaker or failing institutions may be ring fenced into failing safely then it will start growing.When growth gains traction it will lead to inflation. The trouble is that US FED does not want inflation but that inflation is decades away. But looking at that possibility it is doing nonsense like QE tapering etc. Naturally, if you want the industry to appear quickly then it is easier done through Fiscal policy than through monetary policy (no doubt monetary policy needs to be accommodative).

Therefore even inflation will not happen in 2014 and it is a good outcome.

The EU curve ballI think the most weird scenario is that of European Countries. Some are following austerity, others are expanding and the effect is a mixed bag. In fact there is good chance that the next problem will arise in Europe rather than from US tapering.

I think there are more things fundamentally flawed in EU than in US. So I would bet on US in a US v EU debate. Further, I would be wary of developments in EU both political and economic because each has impact on the other.

Further, this problems may come to fruition in 2014. It could be the one almost certain headwind of 2014 unless some dramatic political strategies and monetary policies are put in place. The problematic part is that any meaningful resolution requires massive political coordination spanning different regimes that have different outlook to policies.

I think Martin Wolf has it right in his last video presentation here.

About Indian stock MarketsIndian stock markets are likely to move up till say Jan-Feb and then go through a period of extreme volatility related to elections and possibly few other global factors. The presence of strong and short cycles was critical feature of 2013. I believe this will continue in accordance with slosh-money hypothesis I explained in book and previously on this blog.

The flow and quantum of money means it will keep moving between various asset classes sloshing them with out of the world valuations and ridiculously cheap ticket sizes all in span of 4-5 months. 2013 we had 2 cycles in one year (2 peaks-2 troughs). In 2014 we will have at least 2 (2 peaks-2 troughs) and may be 2.5 (2 or 3 peaks and 3 or 2 troughs).

It means we need to be nimble in investment and must be ready to keep the money off the table. This, as I have experienced in 2013 is more difficult than it sounds. One need not be a daily trader, but the investment strategy must be tested more often than what we previously believed. The days of buy and hold are over and in fact buy and hold has become more destructive option today.

What about Gold and Oil?

To me it seems that Gold and Oil will not be as critical as thought previously. Gold will slowly gain traction and it will go past $3500. The nature and quantum of QE, already delivered and expected to be necessary, will have substantial bearing on the projected price of Gold. The forecast for medium term gold prices varies between $2000 to about $7000 primarily because the fact that the other side of the equation i.e. total amount of money in the system has a wide estimate. Once that clears up the Gold forecast will be much more saner. Having said that, the fact that the total amount of money in the system is unknown/varies drastically itself makes a case for Gold. Thus, I would be buying Gold if I was USD /developed economy buyer. In a different currency, the Gold trade may not be as compelling.

Oil may be more volatile in accordance with the QE news flow. Oil gaining its position as store of value (a story that had abated after Shale and other quasi-oil alternatives). Though Oil as store of value is likely to end disastrously. Oil is no longer the resource crunch story that it was between 2005-2010 period. We have never heard the real oil story. There is no dearth of oil if you set aside the environmental consideration and cost of drilling. So "Peak Oil" really refers to "Peak $50 Oil". The real constraints are in fact the environmental considerations and we may do well to move away from oil sooner than later.

War is coming

So long as US continues on its Japanese strategy, we are going to see possibility of war increasing. It is possible that China will induct 5-6 Aircraft carriers into its navy in 2014 if not more in preparation for war.

The new Chinese leadership will face tougher challenges converting its economy from a producer-driven economy to a consumer-driven economy. Further, the lack of sustainable global demand will not ease the pressure on Chinese government. When the problems of worker migration will ease the problems of worker wages will begin. It will take a great deal of proactivity on part of the new Chinese Leadership to manage these. Further, this is the first truly non-revolution leadership so we are yet to see their mindset.

All said, I see some notoriety involving Chinese sooner or later.

Finally,

As I head to the beach, let me say this, we seem to be in much saner times than we actually are. Insanity is quite a short jump from us at any time. So in such times let sanity prevail, let talents rise and pseudo-leaders fall and let peace be upon us.Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

The hand that Yellen playsI think overall theme of 2014 will be determined by the hand that the US Fed plays over the first two quarters. There are two reasons why I say that. Firstly, Janet Yellen is clearly from the Bernanke School and people expect the QE -based easy monetary policy will continue. Secondly, contra the above Yellen is talking about modifying the nature of QE to be more directed and precise. I think that is full of risks which market has not fully understood as yet.

QE till eternity? Almost!One thing is clear you cannot have QE taper till you have sustainable employment with a visibility over say a 10-15 year period AND reasonably deleveraged US household. Once that is achieved then you can consider a talk of taper and the resulting volatility will be allayed by stronger household balance sheets and things can progress from thereon. So in effect the following things must happen:Employment must reach about 95% of the workforce. It should be reasonably certain employment.Ideally, US need to see emergence of a new industry which has three characteristics - first it fits with the US competitive character; second, it is a mass employer employing relatively lower skilled people and third it has second order, third order effects. Most likely that industry could be in renewable energy or water conservation space.There must be a reasonable clearing of Household debts and households must be reasonable deleveraged with margin to take on more debt if required.But it won't happen in 2014

To gather up that kind of employment we need a Fiscal side action. A national overhaul of US infrastructure will raise my hopes though it does not promise the sustainable employment for at least 15 years. But it is a fair shot to say the least. The current Fiscal policy is far too short of any meaningful contribution in this regard.

Will QE lead to a US Inflation?The whole idea of stimulus is that money will flow through the channel to the places where it can create value- therefore GDP growth- therefore jobs and this cycle will pull the economy out of the doldrums. Today the situation is different.

First it is difficult to keep injected money within the territorial borders to create the desired effect. This means two things. First the quantum of stimulus required will be far larger considering the wastage. Second, the problems of world have bearing on the quantum.

Second the mechanism of money flow or money flow channel is not functional so you cannot get the flow to the lower rungs (i.e. from asset investors to asset owners). That implies that the money is sloshing into restricted space. It is spilling into global asset classes searching for a channel to reach the bottom. (EM equities being one of them).

There are two things that must happen before the money starts getting channelized properly. You need and investable industry to crop up. And not any industry will do - it must employ relatively lower skilled people in large numbers. When we find such an industry (as a few are being experimented with) we will see money being rapidly absorbed.The current uncertainty of weak institutions collapsing must go away as in early investment stages any industry is quite vulnerable and ours will be no different. When there is adequate certainty that the weaker or failing institutions may be ring fenced into failing safely then it will start growing.When growth gains traction it will lead to inflation. The trouble is that US FED does not want inflation but that inflation is decades away. But looking at that possibility it is doing nonsense like QE tapering etc. Naturally, if you want the industry to appear quickly then it is easier done through Fiscal policy than through monetary policy (no doubt monetary policy needs to be accommodative).

Therefore even inflation will not happen in 2014 and it is a good outcome.

The EU curve ballI think the most weird scenario is that of European Countries. Some are following austerity, others are expanding and the effect is a mixed bag. In fact there is good chance that the next problem will arise in Europe rather than from US tapering.

I think there are more things fundamentally flawed in EU than in US. So I would bet on US in a US v EU debate. Further, I would be wary of developments in EU both political and economic because each has impact on the other.

Further, this problems may come to fruition in 2014. It could be the one almost certain headwind of 2014 unless some dramatic political strategies and monetary policies are put in place. The problematic part is that any meaningful resolution requires massive political coordination spanning different regimes that have different outlook to policies.

I think Martin Wolf has it right in his last video presentation here.

About Indian stock MarketsIndian stock markets are likely to move up till say Jan-Feb and then go through a period of extreme volatility related to elections and possibly few other global factors. The presence of strong and short cycles was critical feature of 2013. I believe this will continue in accordance with slosh-money hypothesis I explained in book and previously on this blog.

The flow and quantum of money means it will keep moving between various asset classes sloshing them with out of the world valuations and ridiculously cheap ticket sizes all in span of 4-5 months. 2013 we had 2 cycles in one year (2 peaks-2 troughs). In 2014 we will have at least 2 (2 peaks-2 troughs) and may be 2.5 (2 or 3 peaks and 3 or 2 troughs).

It means we need to be nimble in investment and must be ready to keep the money off the table. This, as I have experienced in 2013 is more difficult than it sounds. One need not be a daily trader, but the investment strategy must be tested more often than what we previously believed. The days of buy and hold are over and in fact buy and hold has become more destructive option today.

What about Gold and Oil?

To me it seems that Gold and Oil will not be as critical as thought previously. Gold will slowly gain traction and it will go past $3500. The nature and quantum of QE, already delivered and expected to be necessary, will have substantial bearing on the projected price of Gold. The forecast for medium term gold prices varies between $2000 to about $7000 primarily because the fact that the other side of the equation i.e. total amount of money in the system has a wide estimate. Once that clears up the Gold forecast will be much more saner. Having said that, the fact that the total amount of money in the system is unknown/varies drastically itself makes a case for Gold. Thus, I would be buying Gold if I was USD /developed economy buyer. In a different currency, the Gold trade may not be as compelling.

Oil may be more volatile in accordance with the QE news flow. Oil gaining its position as store of value (a story that had abated after Shale and other quasi-oil alternatives). Though Oil as store of value is likely to end disastrously. Oil is no longer the resource crunch story that it was between 2005-2010 period. We have never heard the real oil story. There is no dearth of oil if you set aside the environmental consideration and cost of drilling. So "Peak Oil" really refers to "Peak $50 Oil". The real constraints are in fact the environmental considerations and we may do well to move away from oil sooner than later.

War is coming

So long as US continues on its Japanese strategy, we are going to see possibility of war increasing. It is possible that China will induct 5-6 Aircraft carriers into its navy in 2014 if not more in preparation for war.

The new Chinese leadership will face tougher challenges converting its economy from a producer-driven economy to a consumer-driven economy. Further, the lack of sustainable global demand will not ease the pressure on Chinese government. When the problems of worker migration will ease the problems of worker wages will begin. It will take a great deal of proactivity on part of the new Chinese Leadership to manage these. Further, this is the first truly non-revolution leadership so we are yet to see their mindset.

All said, I see some notoriety involving Chinese sooner or later.

Finally,

As I head to the beach, let me say this, we seem to be in much saner times than we actually are. Insanity is quite a short jump from us at any time. So in such times let sanity prevail, let talents rise and pseudo-leaders fall and let peace be upon us.Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

October 15, 2013

Happy Dassera - Why we Indians buy Gold during Dassera / Diwali period?

Indian fetish for gold is well known. The whole of the country goes to the goldsmith and buys their gold during Dassera/Diwali period leading to a huge buying spree. A lot of people ask me how the custom of buying gold during the Dassera (leaves of specific tree that are deemed to be gold) / Diwali period (actual buying of gold) came into being. Then they read wikipedia and various stories about Kuber (the God's treasurer) and other related stories. Here is the real(!) explanation.

Actually the story starts with Ramayana. Ravana, the demon king, had accumulated huge pile of gold and it was kept in Sri Lanka. Ravana being conqueror of three worlds had quite a stock pile at this place. The Ramayana has vivid description of gold-palaces and gold plated public places in Lanka. Nonetheless, he was all powerful so the stock pile was out of bounds for accumulation for the rest of the world.

The sequence of events unfolded such that Rama ended up defeating Ravana killing him on the day of Dassera. Naturally the assets of Ravana were accessible to the investors after that point. Therefore, the price of gold dropped drastically leading to a buying frenzy fuelled by suppressed demand.

The South which got wind of the end of Ravana started trading in gold contracts using tree leaves. The North got the information about demise of Ravana when Rama arrived in his plane (with of course quite a bit of gold) by Diwali. (No bloomberg in those times!)

Today, the situation is quite the reverse, gold prices actually go up during the festive times and therefore it makes no sense to buy gold on Dassera / Diwali period. Rather buy it a month or two before.

To me this story seems more plausible than all the mythical stories we have been fed. But then I am a rationalist.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Actually the story starts with Ramayana. Ravana, the demon king, had accumulated huge pile of gold and it was kept in Sri Lanka. Ravana being conqueror of three worlds had quite a stock pile at this place. The Ramayana has vivid description of gold-palaces and gold plated public places in Lanka. Nonetheless, he was all powerful so the stock pile was out of bounds for accumulation for the rest of the world.

The sequence of events unfolded such that Rama ended up defeating Ravana killing him on the day of Dassera. Naturally the assets of Ravana were accessible to the investors after that point. Therefore, the price of gold dropped drastically leading to a buying frenzy fuelled by suppressed demand.

The South which got wind of the end of Ravana started trading in gold contracts using tree leaves. The North got the information about demise of Ravana when Rama arrived in his plane (with of course quite a bit of gold) by Diwali. (No bloomberg in those times!)

Today, the situation is quite the reverse, gold prices actually go up during the festive times and therefore it makes no sense to buy gold on Dassera / Diwali period. Rather buy it a month or two before.

To me this story seems more plausible than all the mythical stories we have been fed. But then I am a rationalist.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Money Supply - when and how QE becomes dangerous

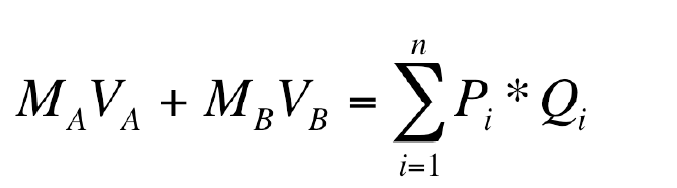

To understand how money supply becomes dangerous, let us begin with our equation which is now modified as follows:

Just to reiterate, here:

M = Money supply

V = Velocity of Money

MA = Original money supply

VA = Velocity of the money supply

MB = Money supply added during QE

VB = Velocity of this expanded money supply

P = Price of good (product or service) "i"

Qi = Quantity of good (product or service) "i" sold

n = Total number of goods

M*V = Money Momentum

PI = Purchase Intensity

Makings of a recession or slowdowns

Before a slowdown we have MB equal to zero as there is no QE. When a slowdown strikes Qi reduces drastically. To compensate the reduction of Qi, central bank injects MB. In the ideal case the velocity VB should be positive and commensurate with MB (the quantum of additional money supply). Now as we discussed the exact mechanics of QE were designed to keep VB low so that injection of money does not cause runaway inflation.

To adjust to excess money supply, the purchase of some items increases. If such items are assets, then we have the hoarding vs. building problem we spoke about. The exact response of the economy depends on the mechanics of QE. However, either ways it plants the seeds for future problems.

When does QE turn bad

When the economy does finally recover, the right side of the equation starts gaining traction. To compensate, the two components on the left, VA and VB have to adjust (assuming no further QE is added). Now the nature of velocity is such that increments in micro-V (velocity at individual level) are more step-changes rather than smooth analogue. Therefore even when the Velocity in the equation is smoother than the micro-V, it increases quite drastically. The pace of increase of the velocity is remarkably higher than pace at which fundamental growth can take place - i.e. growth in "n"or "Q". The excess therefore spills over to "P" or the price leading to inflation. At such moment, there is required to be a mechanism to absorb excess liquidity. But then a precise mop does not exist that can mop at the right places. The result is that there is inflation in certain goods while others are relatively stable.

The argument the inflationists are making is two-fold - first that the increase in V post revival will be far too drastic to allow for commensurate growth in "n" or "Q" to temper the price rise and secondly the central banks will not be able to mop up the rest. In fact, Bernanke's QE strategy created the VA-VB split to allow for quick withdrawal i.e. the second kind of problem. However, this design kept VB low increasing the quantum stimulus required. In other words, Bernanke's design increases the first type of problem.

Lastly, higher the quantum of QE the more difficult it is to mop it up. Which means the economy will absorb it relatively quickly and this absorption will result into a high-inflation scenario.

The correlated bad effects

The US economy being the global leader and dollar being global reserve currency, there are correlated bad effects to deal with. When inflation gains traction, there is change in the value of holdings of other countries in US (dollar reserves which were necessary for currency management). If the change in value is substantial then there will be a possibility of renewed currency wars.

If the inflation increases beyond control then there is a risk of currency losing its function as carrier of information (of value). This triggers a wider crisis globally.

In Sum - Can we prevent bad after-effects of QE

We can but in all probability we won't looking at current politics. Avoiding the bad side-effects requires integrated monetary-fiscal approach. There is not much room for political compromise as most of the activities are almost imperative. We need the US politicians to be lot more saner than they actually are. But is it expecting too much? I don't know.

Note: This post is derived from my book Subverting Capitalism and Democracy. You can read the book at the link below.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Just to reiterate, here:

M = Money supply

V = Velocity of Money

MA = Original money supply

VA = Velocity of the money supply

MB = Money supply added during QE

VB = Velocity of this expanded money supply

P = Price of good (product or service) "i"

Qi = Quantity of good (product or service) "i" sold

n = Total number of goods

M*V = Money Momentum

PI = Purchase Intensity

Makings of a recession or slowdowns

Before a slowdown we have MB equal to zero as there is no QE. When a slowdown strikes Qi reduces drastically. To compensate the reduction of Qi, central bank injects MB. In the ideal case the velocity VB should be positive and commensurate with MB (the quantum of additional money supply). Now as we discussed the exact mechanics of QE were designed to keep VB low so that injection of money does not cause runaway inflation.

To adjust to excess money supply, the purchase of some items increases. If such items are assets, then we have the hoarding vs. building problem we spoke about. The exact response of the economy depends on the mechanics of QE. However, either ways it plants the seeds for future problems.

When does QE turn bad

When the economy does finally recover, the right side of the equation starts gaining traction. To compensate, the two components on the left, VA and VB have to adjust (assuming no further QE is added). Now the nature of velocity is such that increments in micro-V (velocity at individual level) are more step-changes rather than smooth analogue. Therefore even when the Velocity in the equation is smoother than the micro-V, it increases quite drastically. The pace of increase of the velocity is remarkably higher than pace at which fundamental growth can take place - i.e. growth in "n"or "Q". The excess therefore spills over to "P" or the price leading to inflation. At such moment, there is required to be a mechanism to absorb excess liquidity. But then a precise mop does not exist that can mop at the right places. The result is that there is inflation in certain goods while others are relatively stable.

The argument the inflationists are making is two-fold - first that the increase in V post revival will be far too drastic to allow for commensurate growth in "n" or "Q" to temper the price rise and secondly the central banks will not be able to mop up the rest. In fact, Bernanke's QE strategy created the VA-VB split to allow for quick withdrawal i.e. the second kind of problem. However, this design kept VB low increasing the quantum stimulus required. In other words, Bernanke's design increases the first type of problem.

Lastly, higher the quantum of QE the more difficult it is to mop it up. Which means the economy will absorb it relatively quickly and this absorption will result into a high-inflation scenario.

The correlated bad effects

The US economy being the global leader and dollar being global reserve currency, there are correlated bad effects to deal with. When inflation gains traction, there is change in the value of holdings of other countries in US (dollar reserves which were necessary for currency management). If the change in value is substantial then there will be a possibility of renewed currency wars.

If the inflation increases beyond control then there is a risk of currency losing its function as carrier of information (of value). This triggers a wider crisis globally.

In Sum - Can we prevent bad after-effects of QE

We can but in all probability we won't looking at current politics. Avoiding the bad side-effects requires integrated monetary-fiscal approach. There is not much room for political compromise as most of the activities are almost imperative. We need the US politicians to be lot more saner than they actually are. But is it expecting too much? I don't know.

Note: This post is derived from my book Subverting Capitalism and Democracy. You can read the book at the link below.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

June 16, 2013

What is worse? Comments on John Mauldin's Economists are still clueless

John Mauldin's weekly newsletter is a must read as always. This time he titles it Economists are still clueless. He rants about how economists failed to predict the crisis totally.

However, my problem is not that the economists failed to predict the crisis, nor it is that they have been repeatedly failing at it. My problem is that economists still do not understand how economic systems work. The present economic model has serious gaps that fail to even indicate a remote possibility of an interlinked financial system, etc.

There is serious difference of opinion among economists about how economics actually works. And this makes it less of a science than an art. No doubt there are large number of variables involved in the process, the problem is that these variables have inter-dependencies that economists themselves are not aware of.

I believe the basic model I have proposed in Subverting Capitalism - that of bargaining power within a transaction based economy is better alternative to map economics as a whole. Secondly, I believe my model will take us towards a coherent view of micro and macro economic study rather than the difference we see today.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

However, my problem is not that the economists failed to predict the crisis, nor it is that they have been repeatedly failing at it. My problem is that economists still do not understand how economic systems work. The present economic model has serious gaps that fail to even indicate a remote possibility of an interlinked financial system, etc.

There is serious difference of opinion among economists about how economics actually works. And this makes it less of a science than an art. No doubt there are large number of variables involved in the process, the problem is that these variables have inter-dependencies that economists themselves are not aware of.

I believe the basic model I have proposed in Subverting Capitalism - that of bargaining power within a transaction based economy is better alternative to map economics as a whole. Secondly, I believe my model will take us towards a coherent view of micro and macro economic study rather than the difference we see today.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Bank Deposits, Savings and function of Money

We will divert from our series a bit and get to an important aspect of Money which is its function. However, Money performs two functions.

Raison d'etre of money

Money came into being to facilitate exchange of goods. Money split the old time barter (which was one transaction) into two transactions (goods-I-have for money and money for goods-I-want). This allowed for both transactions to achieve market efficiencies. Enabling transaction is the first function of Money. So money is medium of exchange. In this process Money conveys information about prices of goods. When the prices change, it conveys information about changes to the product or the environment or some other thing. This information function of money is as important as the second.

Second function of money is that of a store of value. Value of money means its purchasing power. Bank deposits are storing value. Technically, money should not be performing this function. But this function is inadvertently taken up by money when the information about the product or money itself changes the price levels and hence the purchasing power. Thus, for example, after exchanging goods-I-have for money, when I was having money with me, the price of goods-I-want halved. That means the purchasing power of money increased and thus money became more valuable.

Thus when we hold money and there is change in the information available leading to change in prices, the function of money is that of store of value.

What should money do?

Money should enable transactions - so it must not hinder your transactions (by credit card not being available). Or by becoming so valuable itself that people want to post-pone their transaction to get a better deal.

It should convey information about prices so that you can compare and match your funds, needs and compare alternative purchases (apples vs apples vs oranges etc). This information must be reasonably stable. So if I understand that price of a shirt is about $25 then tomorrow it cannot be $150 or $5 because that will create confusion. But it can be say $23 or $27 and it would not be much of problem.

Money has no business being store of value by itself. However, the fact remains that money remains the only way to measure value. We do not have other unit to measure it.

Douglas Rushkoff (starting about 23 min) on money should push transactions.

Use of money and current and deposit accounts

So actually, money in our current account is actually money to be used for transaction as a medium of exchange while the money we have in time-deposits or other deposit accounts is actually money as a store of value. Now if you ask any lay person, if the amount of money in both the accounts reflects this functional segregation and you will find it does not. The way we use money mixes up the two functions of money.

One way to clarify the usage is to make it clear that current account is your money awaiting transaction while deposit account is your investment into the bank. This segregation will make it clear to users what exactly they are using money as. Thus, banks should provide the analysis of expenses from the account and that should indicate a certain current account balance. The rest should be into deposit accounts.

Now, from the level of deposit insurance available to the bank, there should be disclosure about the amount of your money protected by deposit insurance. When deposit insurance is applied it must be applied to current account first and then to deposit account.

Purchasing power of the money

In an ideal case the purchasing power of the money should remain perfectly the same. If the purchasing power remains exactly the same the productivity gains will result in lowering of prices which is also termed as deflation. Now we also do not want that because in a deflationary scenario, holding money becomes lucrative as its value only increases and this affinity for money creates a hindrance in transactions. As we discussed, ideally money should not hinder transactions in any way.

To overcome this, we settle for a slight inflation. If we do it right, then the inflationary force exactly balances out the productivity gains and therefore results in no change in the prices. But such ideal outcome is not possible. So the policy maker must err in his judgement. A better side to err (it is debatable) is on the side on inflation but only ever so slight inflation.

George Selgin on Good Deflation and Bad Deflation

In Sum

The function of money and our appreciation of the function itself has policy implication. We must understand the function of money before we understand monetary policy itself.

Note: This post is derived from my book Subverting Capitalism and Democracy. You can read the book at the link below.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Raison d'etre of money

Money came into being to facilitate exchange of goods. Money split the old time barter (which was one transaction) into two transactions (goods-I-have for money and money for goods-I-want). This allowed for both transactions to achieve market efficiencies. Enabling transaction is the first function of Money. So money is medium of exchange. In this process Money conveys information about prices of goods. When the prices change, it conveys information about changes to the product or the environment or some other thing. This information function of money is as important as the second.

Second function of money is that of a store of value. Value of money means its purchasing power. Bank deposits are storing value. Technically, money should not be performing this function. But this function is inadvertently taken up by money when the information about the product or money itself changes the price levels and hence the purchasing power. Thus, for example, after exchanging goods-I-have for money, when I was having money with me, the price of goods-I-want halved. That means the purchasing power of money increased and thus money became more valuable.

Thus when we hold money and there is change in the information available leading to change in prices, the function of money is that of store of value.

What should money do?

Money should enable transactions - so it must not hinder your transactions (by credit card not being available). Or by becoming so valuable itself that people want to post-pone their transaction to get a better deal.

It should convey information about prices so that you can compare and match your funds, needs and compare alternative purchases (apples vs apples vs oranges etc). This information must be reasonably stable. So if I understand that price of a shirt is about $25 then tomorrow it cannot be $150 or $5 because that will create confusion. But it can be say $23 or $27 and it would not be much of problem.

Money has no business being store of value by itself. However, the fact remains that money remains the only way to measure value. We do not have other unit to measure it.

Douglas Rushkoff (starting about 23 min) on money should push transactions.

Use of money and current and deposit accounts

So actually, money in our current account is actually money to be used for transaction as a medium of exchange while the money we have in time-deposits or other deposit accounts is actually money as a store of value. Now if you ask any lay person, if the amount of money in both the accounts reflects this functional segregation and you will find it does not. The way we use money mixes up the two functions of money.

One way to clarify the usage is to make it clear that current account is your money awaiting transaction while deposit account is your investment into the bank. This segregation will make it clear to users what exactly they are using money as. Thus, banks should provide the analysis of expenses from the account and that should indicate a certain current account balance. The rest should be into deposit accounts.

Now, from the level of deposit insurance available to the bank, there should be disclosure about the amount of your money protected by deposit insurance. When deposit insurance is applied it must be applied to current account first and then to deposit account.

Purchasing power of the money

In an ideal case the purchasing power of the money should remain perfectly the same. If the purchasing power remains exactly the same the productivity gains will result in lowering of prices which is also termed as deflation. Now we also do not want that because in a deflationary scenario, holding money becomes lucrative as its value only increases and this affinity for money creates a hindrance in transactions. As we discussed, ideally money should not hinder transactions in any way.

To overcome this, we settle for a slight inflation. If we do it right, then the inflationary force exactly balances out the productivity gains and therefore results in no change in the prices. But such ideal outcome is not possible. So the policy maker must err in his judgement. A better side to err (it is debatable) is on the side on inflation but only ever so slight inflation.

George Selgin on Good Deflation and Bad Deflation

In Sum

The function of money and our appreciation of the function itself has policy implication. We must understand the function of money before we understand monetary policy itself.

Note: This post is derived from my book Subverting Capitalism and Democracy. You can read the book at the link below.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".