Rahul Deodhar's Blog, page 12

August 17, 2016

What should governments spend on when faced with fiscal stimulus?

At the time of financial crisis of 2008-09, we were lucky to have the best monetary policy experts around. They seemingly used their various tools - some conventional and other unconventional. Yet about 8 years after we find we need fiscal stimulus as Mario Draghi put in an ECB statement in early summer. Luckily the US presidential candidates agree with this view. So in all likelihood, we should see some fiscal stimulus coming in.

Yet, the understanding on the fiscal side does not seem to be as well developed as the monetary sides. For one, exactly what Keynes prescribed is still much debated. Second governments don't know what to spend on. Obama famously called for "shovel-ready" projects. Milton Friedman (who died in 2006) would cringe in his grave. There is nothing more dangerous than a government committed to a fiscal stimulus that does not know what to do with it.

Looking at RooseveltIt is, however, well-accepted that after the World War II, the Roosevelt initiative of building inter-state highway was one of the biggest fiscal stimuli to the US economy. The genesis of this project was the cross-country trip Roosevelt took in mid-1920s which may have given him a hint of its potential. Once it was implemented, its fruits accrued at least till late 1990s. Even in the era when the internet made distance irrelevant, these highways continued to contribute by way of lower transportation cost thereby giving firms advantage in making supply available at lower costs than otherwise.

If fiscal policy is to be deployed today where can we deploy it? What areas would have as much purchase as did the highway program of 1930-40?

To answer this we need to imagine the economy as a network of value chains. Such a network has some common elements which need government support. These are the areas where fiscal policy needs to be directed. This is the efficiency angle. If any government wants to orient its economy in a certain direction then this would be the time to make investments in the missing parts of the value-chain that can be shared in the new era.

A few I can think of:Going green: Reducing Oil-dependance is an option : The very basic pieces of all value chains do contain energy. So an advantage in green energy may be quite advantageous in the long term. Green energy needs a lot of work but could be a potential candidate. It could do with some sort of Manhattan Project 2.0 (the first was for nukes) for making green energy possible. They could standardize the electrical charging stations for hybrids, developing standards and technology to allow smaller wind mill operators to supply into the grid at a time of their convenience. Tesla is looking at this vision through private means.Going blue: Usable water: Food and water will continue to form part of value chains at a very basic level. While global food production is quite high (we destroy a lot of excess food), same cannot be said of global nourishment. It is undeniable that whatever food we grow we will need potable water. Many say if we find green energy then we can desalinate the water. But low fresh water has an ecological impact on bio-diversity, food-chain dynamics etc. that cannot be dismissed. In that sense, the bio-diversity advantage may trickle into better nourishment and healthier foods - who knows. So I would focus on water management.Carbon catchment could be more urgent: In his TED talk Bill Gates made a very poignant statement - we need ZERO emissions, not lower emissions. It is clear that we cannot cut emissions fast enough. But can we trap emissions before they cause global warming? Maybe we should! This is more engineering problem rather than technology problem and may be more beneficial. Alas, its effects are very difficult to quantify.

The nature of fiscal stimulusThe exact quantum of fiscal stimulus is immaterial, though it has to substantial. What matters more is how long is that quantum spread and the conviction behind it. That will decide its efficacy. The fiscal needs to be prolonged, substantial and certain. An uncertain prolonged stimulus or variable stimulus without visibility will have no appreciable impact.

Ideally, it should also be employment intensive. Higher employment intensity will allow the benefits to spread faster through the economy.

The goal of the stimulus is to increase the certainty of jobs and employment while laying down a basic infrastructure for the future. If it achieves this then such a stimulus will work. With a certainty of income will come spending and further downstream positive economic effects.

Note: the suggestions made are simply most promising areas at the moment as per my reading. Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Yet, the understanding on the fiscal side does not seem to be as well developed as the monetary sides. For one, exactly what Keynes prescribed is still much debated. Second governments don't know what to spend on. Obama famously called for "shovel-ready" projects. Milton Friedman (who died in 2006) would cringe in his grave. There is nothing more dangerous than a government committed to a fiscal stimulus that does not know what to do with it.

Looking at RooseveltIt is, however, well-accepted that after the World War II, the Roosevelt initiative of building inter-state highway was one of the biggest fiscal stimuli to the US economy. The genesis of this project was the cross-country trip Roosevelt took in mid-1920s which may have given him a hint of its potential. Once it was implemented, its fruits accrued at least till late 1990s. Even in the era when the internet made distance irrelevant, these highways continued to contribute by way of lower transportation cost thereby giving firms advantage in making supply available at lower costs than otherwise.

If fiscal policy is to be deployed today where can we deploy it? What areas would have as much purchase as did the highway program of 1930-40?

To answer this we need to imagine the economy as a network of value chains. Such a network has some common elements which need government support. These are the areas where fiscal policy needs to be directed. This is the efficiency angle. If any government wants to orient its economy in a certain direction then this would be the time to make investments in the missing parts of the value-chain that can be shared in the new era.

A few I can think of:Going green: Reducing Oil-dependance is an option : The very basic pieces of all value chains do contain energy. So an advantage in green energy may be quite advantageous in the long term. Green energy needs a lot of work but could be a potential candidate. It could do with some sort of Manhattan Project 2.0 (the first was for nukes) for making green energy possible. They could standardize the electrical charging stations for hybrids, developing standards and technology to allow smaller wind mill operators to supply into the grid at a time of their convenience. Tesla is looking at this vision through private means.Going blue: Usable water: Food and water will continue to form part of value chains at a very basic level. While global food production is quite high (we destroy a lot of excess food), same cannot be said of global nourishment. It is undeniable that whatever food we grow we will need potable water. Many say if we find green energy then we can desalinate the water. But low fresh water has an ecological impact on bio-diversity, food-chain dynamics etc. that cannot be dismissed. In that sense, the bio-diversity advantage may trickle into better nourishment and healthier foods - who knows. So I would focus on water management.Carbon catchment could be more urgent: In his TED talk Bill Gates made a very poignant statement - we need ZERO emissions, not lower emissions. It is clear that we cannot cut emissions fast enough. But can we trap emissions before they cause global warming? Maybe we should! This is more engineering problem rather than technology problem and may be more beneficial. Alas, its effects are very difficult to quantify.

The nature of fiscal stimulusThe exact quantum of fiscal stimulus is immaterial, though it has to substantial. What matters more is how long is that quantum spread and the conviction behind it. That will decide its efficacy. The fiscal needs to be prolonged, substantial and certain. An uncertain prolonged stimulus or variable stimulus without visibility will have no appreciable impact.

Ideally, it should also be employment intensive. Higher employment intensity will allow the benefits to spread faster through the economy.

The goal of the stimulus is to increase the certainty of jobs and employment while laying down a basic infrastructure for the future. If it achieves this then such a stimulus will work. With a certainty of income will come spending and further downstream positive economic effects.

Note: the suggestions made are simply most promising areas at the moment as per my reading. Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

August 16, 2016

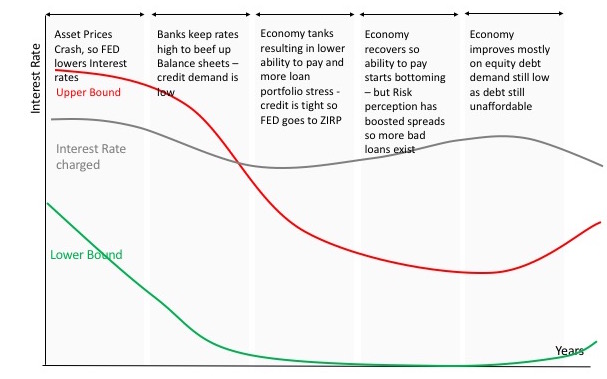

Is assessment of risk a function of interest rate?

The interest rate that can be charged by the bank has two limits.

The Lower bound equals what the central bank charges the bank. Any lower and the bank will make a loss on its lending portfolio.

The Upper bound is the ability of the risk taker to bear the burden of return. Thus, if a bank lends to a business that makes 10% return on capital employed - it cannot charge more than 10% else it will be unviable for the borrower to seek the debt at all.

The Actual interest rate charged is determined by a combination of the following factors:

An assessment of returns of the business based on the economy and her business Income of the borrower in total The value of the collateral pledged against the loan as a security should the borrower be unable to bear that return The demand for loans AND/ORHow well the other loans are doing (health of bank's loan portfolio) AND/ORA combination of these along with global factors Spread Bankers think of returns as spread they make on top of the lower bound, i.e. rate set by the central bank.

Risk V/s Spread Now, in the mind of the banker risk is correlated with the spread. When the banker perceives higher risk she fattens the spread. This "risk" we talk about is risk resulting to the banker. It does not mean risk of the borrower alone. So if the bankers' portfolio is turning bad, the banker will still increase the spread - partly to compensate for the loss she suffers and partly because she assesses the general economic environment to be more risky. Thus, even if the central bank reduces the benchmark interest rate, the banker is reluctant to pass it on if she can avoid it. This creates tighter conditions putting more stress on the borrower. This is why Scot Sumner argues the monetary conditions were actually tight when we were almost at ZIRP.

In an economy that is weak, it acts as a stronger head wind for borrowers. It reduces their ability to borrow and to service their current borrowing. They want to pay down their debt and reduce their loans. Therefore, the economy contracts further. The banks seem happy at first, but soon realise that other borrowers who are not prudent are pushed to default. The implication of this on the bank depends on the mechanics of the process - the proportion of those who default v/s those who pay back, the chronology in which it happens etc.

In the next phase, the economy recovers, predominantly with equity capital. Equity can absorb the losses since it is built for higher risk. The surviving firms and individuals are left with core strength to thrive in intense competition and are more prudent with capital allocation. The banks thereafter can lend to these survivors to help them scale up.

What does this mean? This means, There is inherent value to competitiveness that signifies its ability to survive and repay the debt and repay the equity at decent returns. This ability reduces with increasing leverage by the borrowers. Thus when Anat Admati suggests investment banks have capped leverage ratios to 20 or 10 it makes sense.Banks' business model seems to encourage the use of debt only to amplify equity returns. It is fine in a way but if that is the objective then banks should reduce/cut lending at lot earlier than they do. Naturally, in times of distress when the return ON capital matters lesser than the return OF capital, banks get into big trouble. It seems they get confused about what is their business model. Maybe, better than ZIRP, unleashing a new Government-backed Good Bank to pick up assets at distressed prices at lending rates with narrow and fixed spreads can work better. If the size of this bank is large enough in relation to the banking system, it may result in a lesser shock to the economy.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

The Lower bound equals what the central bank charges the bank. Any lower and the bank will make a loss on its lending portfolio.

The Upper bound is the ability of the risk taker to bear the burden of return. Thus, if a bank lends to a business that makes 10% return on capital employed - it cannot charge more than 10% else it will be unviable for the borrower to seek the debt at all.

The Actual interest rate charged is determined by a combination of the following factors:

An assessment of returns of the business based on the economy and her business Income of the borrower in total The value of the collateral pledged against the loan as a security should the borrower be unable to bear that return The demand for loans AND/ORHow well the other loans are doing (health of bank's loan portfolio) AND/ORA combination of these along with global factors Spread Bankers think of returns as spread they make on top of the lower bound, i.e. rate set by the central bank.

Risk V/s Spread Now, in the mind of the banker risk is correlated with the spread. When the banker perceives higher risk she fattens the spread. This "risk" we talk about is risk resulting to the banker. It does not mean risk of the borrower alone. So if the bankers' portfolio is turning bad, the banker will still increase the spread - partly to compensate for the loss she suffers and partly because she assesses the general economic environment to be more risky. Thus, even if the central bank reduces the benchmark interest rate, the banker is reluctant to pass it on if she can avoid it. This creates tighter conditions putting more stress on the borrower. This is why Scot Sumner argues the monetary conditions were actually tight when we were almost at ZIRP.

In an economy that is weak, it acts as a stronger head wind for borrowers. It reduces their ability to borrow and to service their current borrowing. They want to pay down their debt and reduce their loans. Therefore, the economy contracts further. The banks seem happy at first, but soon realise that other borrowers who are not prudent are pushed to default. The implication of this on the bank depends on the mechanics of the process - the proportion of those who default v/s those who pay back, the chronology in which it happens etc.

In the next phase, the economy recovers, predominantly with equity capital. Equity can absorb the losses since it is built for higher risk. The surviving firms and individuals are left with core strength to thrive in intense competition and are more prudent with capital allocation. The banks thereafter can lend to these survivors to help them scale up.

What does this mean? This means, There is inherent value to competitiveness that signifies its ability to survive and repay the debt and repay the equity at decent returns. This ability reduces with increasing leverage by the borrowers. Thus when Anat Admati suggests investment banks have capped leverage ratios to 20 or 10 it makes sense.Banks' business model seems to encourage the use of debt only to amplify equity returns. It is fine in a way but if that is the objective then banks should reduce/cut lending at lot earlier than they do. Naturally, in times of distress when the return ON capital matters lesser than the return OF capital, banks get into big trouble. It seems they get confused about what is their business model. Maybe, better than ZIRP, unleashing a new Government-backed Good Bank to pick up assets at distressed prices at lending rates with narrow and fixed spreads can work better. If the size of this bank is large enough in relation to the banking system, it may result in a lesser shock to the economy.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

August 15, 2016

Of Free drinks and negative interest rate policy...

If soft drinks (Coke/Pepsi/tea/coffee etc.) were freely available would you tend to have more of it? Often I end up having one extra coke. If its tea/coffee I end up having even more. I will have to work it off that day through exercise or it will cause some harm in the long term.

Zero interest rate policy (ZIRP) is like that - if you already wanted Coke and it was easily available you end up having a little more Coke. Likewise, if you already wanted debt, and it was easily available at almost zero cost, then you will have a little more. But not a lot more - coz you have to work it off.

But what if you don't want them?Say your doctor told you to not have soft drinks at all - no tea/coffee too. Now will you have that? NO? Even if I give you some money - say 2 cents - to have these soft drinks? Still NO?

Well, me giving you some money is similar to Negative interest rate policy (NIRP). Or similar to one aspect of NIRP. You get a tiny advantage if you take on debt. Is it that difficult to understand why it doesn't work as central bankers hope?

But may be NIRP could work...Now some will agree that ZIRP may not work, but, they say, NIRP could work. They point to the second aspect of NIRP which is that if you save you get taxed extra. Now if I have $100 in cash in a bank, next year I will have only $98 so next year I will be able to spend less than I can do today. Isn't that an incentive for spending now rather than next year? I say not always!

There are a few reasons:

If the trends are deflationary your $98 next year may be able to buy as much as $100 today - sometimes even more. If the efficient market hypothesis* were working prices would adjust to reflect the new purchasing power. NIRP would create some deflationary force as well. Yes, it is small but it is deflationary never the less. So unless the NIRP was creating an overwhelming inflationary force, it may push a precariously balanced economy into deflation. The NIRP tax does not affect those paying down an earlier debt. In fact, it encourages people to swap new debt for old debt. Debt repayment helps you avoid the tax. This is even more deflationary.NIRP does not work if I anticipate unpredictable cash requirements - say because I want to keep some money to invest when prices correct, or I think my business loan may need to be repaid if my business does not do well in next quarter, or I expect health care costs etc. In fact, it works reverse - in such cases, I would be encouraged to save $102 or $104 just to keep a buffer.NIRP may push those with huge cash balances to move cash abroad. Do you think Apple and Google will bring that extra cash into a country with NIRP? No way! They might move it to a destination where it will be easier to hold cash. So is this what you want to happen? NO! Who gets affected is the individual who keeps getting taxed extra.I may not want debt or I may not want to spend at all. I have the clothes, I have the phones, computers, TV, house, car, swimming pool etc - all the goodies I can spend on when you nudged me to spend the last time. Now I have mostly everything I need. So why should I spend on something I am not excited about? Beats me!

* I don't think Efficient market hypothesis works on a "point-in-time" basis - though it works on an average basis.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Zero interest rate policy (ZIRP) is like that - if you already wanted Coke and it was easily available you end up having a little more Coke. Likewise, if you already wanted debt, and it was easily available at almost zero cost, then you will have a little more. But not a lot more - coz you have to work it off.

But what if you don't want them?Say your doctor told you to not have soft drinks at all - no tea/coffee too. Now will you have that? NO? Even if I give you some money - say 2 cents - to have these soft drinks? Still NO?

Well, me giving you some money is similar to Negative interest rate policy (NIRP). Or similar to one aspect of NIRP. You get a tiny advantage if you take on debt. Is it that difficult to understand why it doesn't work as central bankers hope?

But may be NIRP could work...Now some will agree that ZIRP may not work, but, they say, NIRP could work. They point to the second aspect of NIRP which is that if you save you get taxed extra. Now if I have $100 in cash in a bank, next year I will have only $98 so next year I will be able to spend less than I can do today. Isn't that an incentive for spending now rather than next year? I say not always!

There are a few reasons:

If the trends are deflationary your $98 next year may be able to buy as much as $100 today - sometimes even more. If the efficient market hypothesis* were working prices would adjust to reflect the new purchasing power. NIRP would create some deflationary force as well. Yes, it is small but it is deflationary never the less. So unless the NIRP was creating an overwhelming inflationary force, it may push a precariously balanced economy into deflation. The NIRP tax does not affect those paying down an earlier debt. In fact, it encourages people to swap new debt for old debt. Debt repayment helps you avoid the tax. This is even more deflationary.NIRP does not work if I anticipate unpredictable cash requirements - say because I want to keep some money to invest when prices correct, or I think my business loan may need to be repaid if my business does not do well in next quarter, or I expect health care costs etc. In fact, it works reverse - in such cases, I would be encouraged to save $102 or $104 just to keep a buffer.NIRP may push those with huge cash balances to move cash abroad. Do you think Apple and Google will bring that extra cash into a country with NIRP? No way! They might move it to a destination where it will be easier to hold cash. So is this what you want to happen? NO! Who gets affected is the individual who keeps getting taxed extra.I may not want debt or I may not want to spend at all. I have the clothes, I have the phones, computers, TV, house, car, swimming pool etc - all the goodies I can spend on when you nudged me to spend the last time. Now I have mostly everything I need. So why should I spend on something I am not excited about? Beats me!

* I don't think Efficient market hypothesis works on a "point-in-time" basis - though it works on an average basis.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

August 2, 2016

Free Trade - or no free Trade - either ways it ain't free!

Econgirl commented about the latest free-trade issue. It is a must read - continue down to the comments too! Then David Henderson commented about it on his blog and the comments where @econgirl responded to his question. All must read in the overall dialogue about free trade.

There are a few things that need consideration:

The losers of free-trade - how adaptable they remain after they lose : In many cases, these people are lost - this is a political price we are paying. Thus, a $10 gain per-consumer v/s say a total job loss of 10,000 people (hypothetical primary loss) usually it remains concentrated (think Detroit) and second and third order economic losses. Now in monetary terms, the gain-loss may be whatever, but when a group of people loses their livelihood without any margin or buffer to create new opportunities for themselves, then it makes for a difficult choice. The initial condition is responsible for the losers being as many as they currently are : If the trade was always free, the adjustment would have taken place a long time ago, giving the population enough margin to adjust. However, the governments by their initial protectionist intervention create a bigger adjustment problem in the future. When a competency develops in a country, the government rallies behind the firms with the very policies which later accumulate into a bigger problem. The adjustment to new potential trade-based threat can be innovation or it can be defeat. The auto-industry failed to innovate - something Tesla did, Ford and GM should have done years ago. But those are victims of their own success. At present, China is funding auto-tech companies to bring out a competitor to Tesla. Free trade - v/s Fair trade : Indeed some countries do "dump" products on to other markets. At the same time, some countries do use "non-tariff barriers" for the protection of domestic industry. When is the "fire-sale" not dumping and when "non-tariff barriers" are not protectionist can only be answered on a case-by-case basis. This ambiguity is used to target Free-trade unfairly. Economic V/s moral - politics enters through morality : Can we allow some trade partner using slave labour to create losses in our country? Economics says why not, morality says no. Blood diamonds are an example. That is where politics comes in. So while overall benefits of free trade may be high - the morality over why the government should not choose one set over other is a strong political motive against change of status quo. Of course people selectively forget that it was government intervention that helped the problem to get bigger.

So in an ideal case:Free Trade is the default. Government has no business interfering in that unless some moral issue arises. The scope of these issues are pretty narrow - slavery etc.Countries should progressively move all policy towards sector neutrality - including trade policy. Thus, a government would be right to have 50% markup over all goods/services entering the country/sold in the country without discrimination.Then let this state continue and let governments step away from the issue altogether. (more on this in another post).

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

There are a few things that need consideration:

The losers of free-trade - how adaptable they remain after they lose : In many cases, these people are lost - this is a political price we are paying. Thus, a $10 gain per-consumer v/s say a total job loss of 10,000 people (hypothetical primary loss) usually it remains concentrated (think Detroit) and second and third order economic losses. Now in monetary terms, the gain-loss may be whatever, but when a group of people loses their livelihood without any margin or buffer to create new opportunities for themselves, then it makes for a difficult choice. The initial condition is responsible for the losers being as many as they currently are : If the trade was always free, the adjustment would have taken place a long time ago, giving the population enough margin to adjust. However, the governments by their initial protectionist intervention create a bigger adjustment problem in the future. When a competency develops in a country, the government rallies behind the firms with the very policies which later accumulate into a bigger problem. The adjustment to new potential trade-based threat can be innovation or it can be defeat. The auto-industry failed to innovate - something Tesla did, Ford and GM should have done years ago. But those are victims of their own success. At present, China is funding auto-tech companies to bring out a competitor to Tesla. Free trade - v/s Fair trade : Indeed some countries do "dump" products on to other markets. At the same time, some countries do use "non-tariff barriers" for the protection of domestic industry. When is the "fire-sale" not dumping and when "non-tariff barriers" are not protectionist can only be answered on a case-by-case basis. This ambiguity is used to target Free-trade unfairly. Economic V/s moral - politics enters through morality : Can we allow some trade partner using slave labour to create losses in our country? Economics says why not, morality says no. Blood diamonds are an example. That is where politics comes in. So while overall benefits of free trade may be high - the morality over why the government should not choose one set over other is a strong political motive against change of status quo. Of course people selectively forget that it was government intervention that helped the problem to get bigger.

So in an ideal case:Free Trade is the default. Government has no business interfering in that unless some moral issue arises. The scope of these issues are pretty narrow - slavery etc.Countries should progressively move all policy towards sector neutrality - including trade policy. Thus, a government would be right to have 50% markup over all goods/services entering the country/sold in the country without discrimination.Then let this state continue and let governments step away from the issue altogether. (more on this in another post).

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

July 6, 2016

Reforming Indian Agriculture

Agriculture reform is one of the big successes of Gujarat Model the foundation of Narendra Modi's political success. Yet, national agricultural reform is still lagging. In a recent article, Ashok Gulati points this out with reference to fertiliser reform. That gave me some food for thought. So here are my set of key ideas for reforms for Agri-dependant population.

Farmers' problems can be summarised easily. Farmers are not sure of what to sow, the technology and funds to improve productivity are difficult to source and they do not have mechanism to maximise the cash flow from what they reap.

Improve Crop Selection : Use soil health card to determine effective crops for that land. Suggest crop selection every sowing season based on available stock of the crop, area already under cultivation and alternatives. Commodity demand and supply can be managed before sowing stage itself. It allows for less farmer/crop failures. Give the farmer data on national area under cultivation for current year and past 5/10 years. (say area under paddy cultivation)Also give total stocks of various commodities (available stock of rice with FCI and national rice stock)Give rice national price trends for past 5/10 years. (say rice prices)Also give comparable import prices for that commodity. Create databank for allowing informed decision on grow v/s import for various crops at various land quality levels.Give suggestions of alternate crops Using these data points let the farmer make an informed decision as to what to plant.

Land and Asset Reforms : Clear land title implies that farmers can get easy benefits of land ownership and clear share of benefits arising from land. It allows farmers to create collateral for investing into farms. Allow clearer ownership of assets such as vehicles, animals and other agricultural implements.

Farmer productivity support : Farm productivity improvement techniques are available at various price points. It is not necessary that most technologically advanced solutions are the best. A database of techniques and corresponding funding agencies should be made available to farmers. This is more information dissemination strategy rather than anything else.

Farmer Produce Income Maximisation:Improve farmer availability by focusing on farmer health. This improve farm-labour availability and thus improves earning potential. It also prevents crops failures because of on-availability of labour.A national farm produce market without middlemen should improve incomes for farmers. But it requires produce classification and grading mechanism. It can be done using kits.Make food processing units investment allowing the produce to be processed for easy transportation across distance and time. Thus, pulping, pickling etc. can be one type of produce revenue maximisation. Other could be farm-side cutting and packaging into easy to consume items - say pre-packaged salads made at farm itself. The whole value-chain from consumers to influencers like dieticians and master-chefs to food factories to farmers should be leveraged.India can leap-frog the agri-produce canning/packaging style processing to directly ready to cook packaging.This activity is more valuable for non-staples like vegetables, fruits etc.

Farmer Income diversification :Augment agricultural income with horticulture, floriculture and other allied agricultural activities. Considering the necessity of creating seepage reservoirs to allow replenishment of land-water, fresh-water based fish, crops etc can be considered. Involve farmers in agri-support transportation services, food processing services etc. Farmer Savings support : Improve reach of banking to rural areas. Problem for farmers is that loan availability is at high cost and savings benefits are at low rates. Even if loans are not made available a secure savings infrastructure needs to be developed for farmers. Jan Dhan is a good first step.

With these, farming should be gaining traction and agriculture can add at least 2 percentage points to India's GDP growth.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Farmers' problems can be summarised easily. Farmers are not sure of what to sow, the technology and funds to improve productivity are difficult to source and they do not have mechanism to maximise the cash flow from what they reap.

Improve Crop Selection : Use soil health card to determine effective crops for that land. Suggest crop selection every sowing season based on available stock of the crop, area already under cultivation and alternatives. Commodity demand and supply can be managed before sowing stage itself. It allows for less farmer/crop failures. Give the farmer data on national area under cultivation for current year and past 5/10 years. (say area under paddy cultivation)Also give total stocks of various commodities (available stock of rice with FCI and national rice stock)Give rice national price trends for past 5/10 years. (say rice prices)Also give comparable import prices for that commodity. Create databank for allowing informed decision on grow v/s import for various crops at various land quality levels.Give suggestions of alternate crops Using these data points let the farmer make an informed decision as to what to plant.

Land and Asset Reforms : Clear land title implies that farmers can get easy benefits of land ownership and clear share of benefits arising from land. It allows farmers to create collateral for investing into farms. Allow clearer ownership of assets such as vehicles, animals and other agricultural implements.

Farmer productivity support : Farm productivity improvement techniques are available at various price points. It is not necessary that most technologically advanced solutions are the best. A database of techniques and corresponding funding agencies should be made available to farmers. This is more information dissemination strategy rather than anything else.

Farmer Produce Income Maximisation:Improve farmer availability by focusing on farmer health. This improve farm-labour availability and thus improves earning potential. It also prevents crops failures because of on-availability of labour.A national farm produce market without middlemen should improve incomes for farmers. But it requires produce classification and grading mechanism. It can be done using kits.Make food processing units investment allowing the produce to be processed for easy transportation across distance and time. Thus, pulping, pickling etc. can be one type of produce revenue maximisation. Other could be farm-side cutting and packaging into easy to consume items - say pre-packaged salads made at farm itself. The whole value-chain from consumers to influencers like dieticians and master-chefs to food factories to farmers should be leveraged.India can leap-frog the agri-produce canning/packaging style processing to directly ready to cook packaging.This activity is more valuable for non-staples like vegetables, fruits etc.

Farmer Income diversification :Augment agricultural income with horticulture, floriculture and other allied agricultural activities. Considering the necessity of creating seepage reservoirs to allow replenishment of land-water, fresh-water based fish, crops etc can be considered. Involve farmers in agri-support transportation services, food processing services etc. Farmer Savings support : Improve reach of banking to rural areas. Problem for farmers is that loan availability is at high cost and savings benefits are at low rates. Even if loans are not made available a secure savings infrastructure needs to be developed for farmers. Jan Dhan is a good first step.

With these, farming should be gaining traction and agriculture can add at least 2 percentage points to India's GDP growth.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

June 24, 2016

Yeah! On Brexit!

Yeah Brexit is a reality! Signifies a few things:

Politicians have misused / abused the Brexit debateThe political and ruling classes are disconnected from the realities faced by the worker class. A sort of marxist dream has come true. Not only can't the politicians talk reasonably with the masses but they also don't seem to care. John Mauldin highlighted Peggy Noonan's protected v/s unprotected rationale - it is playing out now. Necessary corollary - we might be looking at a Trump victory.A sub-set of the worker class problem is the migrant issue. The migrants coming into do have a group of anti-community / anti-EU society that has entered EU creating social tension. While, most of the migrants are male - a statistic that is queer for war-related migration. I would have thought it should be more women and children (as per UN 62% of all migrants out of 800,000 that have traveled to Europe in 2015 are men). Sadly, this has confused the domestic worker class about rational economic threat to their incomes and political threat to safety and well being. The first is short term set-back but results in long term prosperity. The second is a bit scary. The pro-Brexit vote is more because of second than first.Media hasn't done its bit to inform the average person.Media's lack of responsibility since the crisis has been alarming. But the polarised opinion on Brexit put up by media are disappointing. The irrational rabble rousing has overwhelmed the thoughtful assessments and complexity of the issues has been trivialised. Common people in developed countries are going to looseThe discrepancy between easy capital mobility and difficult labour mobility affects the working class. If left unresolved, we will end up with capital controls. (Yeah it is a long way away but we are on that road). Alternatively, we can hope that labour mobility will ease up and people will realise their folly. Our lack of understanding of economics has come to haunt us.Currently, only low income-low skilled people from under-developed countries want to migrate to developed countries because these people are squeezed to be producers in their own country. Similarly, the developed country people are tickled into consuming more than they can afford so that the status quo continues. The developed world citizens do not want to impair their life-style by migrating to developing countries. (That is because developing countries make it difficult to get the same life-style as developed countries - I mean in terms of law and order and quality of education etc.). This one-way traffic had to stop some time.With cheap capital, replacing a low-skill worker by expensive robots is feasible. This pains the working class no end. These people are caught between rock and hard place. They are being forced to go down to low-skill but on-site jobs. (the famous McJobs!)It is this anxiety that has been exploited for Brexit. So part of the blame goes to the economist and finance experts too. These are the very people who look shocked at Brexit vote.After Brexit what next?In an age of increasing inter-connectedness a Brexit vote is first step trying to reverse the globalisation. There are reasons why anti-globalisation forces have followers - I wrote about this messy intermediate globalised system that is straining the worker class. But advantage really lies in globalisation and not protectionism.Unfortunately, the competitive raising of protectionist barriers will only increase. Marine Le Pen is demanding referendum for France. The northern EU members and Germany will soon be left looking stupid. So instead of PIGS defaulting and exiting - non-PIGS will drop off the union.The war on globalisation had to fought on "sovereignty" issue. It is a political war connected with Swiss bank hidden wealth, Tax havens and other "loop holes". Once successful politically, these initiatives will turn on economic policy. The good work of integrating the world will be undone by economic and fiscal policies.

Brexit will be a slow poisonThe consequences of Brexit are far more dangerous but they will take time to play out. That means markets and asset prices will remain volatile. Consequently, long term investment in future shall remain the exclusive domain of governments. Add to this the renewed focus on austerity - 1937 looms all over again.

So it is said - may you live in interesting times.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Politicians have misused / abused the Brexit debateThe political and ruling classes are disconnected from the realities faced by the worker class. A sort of marxist dream has come true. Not only can't the politicians talk reasonably with the masses but they also don't seem to care. John Mauldin highlighted Peggy Noonan's protected v/s unprotected rationale - it is playing out now. Necessary corollary - we might be looking at a Trump victory.A sub-set of the worker class problem is the migrant issue. The migrants coming into do have a group of anti-community / anti-EU society that has entered EU creating social tension. While, most of the migrants are male - a statistic that is queer for war-related migration. I would have thought it should be more women and children (as per UN 62% of all migrants out of 800,000 that have traveled to Europe in 2015 are men). Sadly, this has confused the domestic worker class about rational economic threat to their incomes and political threat to safety and well being. The first is short term set-back but results in long term prosperity. The second is a bit scary. The pro-Brexit vote is more because of second than first.Media hasn't done its bit to inform the average person.Media's lack of responsibility since the crisis has been alarming. But the polarised opinion on Brexit put up by media are disappointing. The irrational rabble rousing has overwhelmed the thoughtful assessments and complexity of the issues has been trivialised. Common people in developed countries are going to looseThe discrepancy between easy capital mobility and difficult labour mobility affects the working class. If left unresolved, we will end up with capital controls. (Yeah it is a long way away but we are on that road). Alternatively, we can hope that labour mobility will ease up and people will realise their folly. Our lack of understanding of economics has come to haunt us.Currently, only low income-low skilled people from under-developed countries want to migrate to developed countries because these people are squeezed to be producers in their own country. Similarly, the developed country people are tickled into consuming more than they can afford so that the status quo continues. The developed world citizens do not want to impair their life-style by migrating to developing countries. (That is because developing countries make it difficult to get the same life-style as developed countries - I mean in terms of law and order and quality of education etc.). This one-way traffic had to stop some time.With cheap capital, replacing a low-skill worker by expensive robots is feasible. This pains the working class no end. These people are caught between rock and hard place. They are being forced to go down to low-skill but on-site jobs. (the famous McJobs!)It is this anxiety that has been exploited for Brexit. So part of the blame goes to the economist and finance experts too. These are the very people who look shocked at Brexit vote.After Brexit what next?In an age of increasing inter-connectedness a Brexit vote is first step trying to reverse the globalisation. There are reasons why anti-globalisation forces have followers - I wrote about this messy intermediate globalised system that is straining the worker class. But advantage really lies in globalisation and not protectionism.Unfortunately, the competitive raising of protectionist barriers will only increase. Marine Le Pen is demanding referendum for France. The northern EU members and Germany will soon be left looking stupid. So instead of PIGS defaulting and exiting - non-PIGS will drop off the union.The war on globalisation had to fought on "sovereignty" issue. It is a political war connected with Swiss bank hidden wealth, Tax havens and other "loop holes". Once successful politically, these initiatives will turn on economic policy. The good work of integrating the world will be undone by economic and fiscal policies.

Brexit will be a slow poisonThe consequences of Brexit are far more dangerous but they will take time to play out. That means markets and asset prices will remain volatile. Consequently, long term investment in future shall remain the exclusive domain of governments. Add to this the renewed focus on austerity - 1937 looms all over again.

So it is said - may you live in interesting times.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

August 30, 2015

Its not a Chinese sell-off!

For the past week, global markets have taken a fancy to the slowing of Chinese economy. It could be envy of watching a defiant surge in Chinese markets without any hiccup what so ever. This story, it appears, has nothing to do with China and more to do with Yellen. China somehow was an opportune discovery.

The American economy, its size, and its global linkages make it core factor in asset price calculations. The US is a primary exporter of capital to most of the important markets of the world. It is also usually the most important sizeable end-consumer for many including China. Comparatively China is less inter-connected.

A US asset price rerating will affect everyone. There is a risk hierarchy of assets explicit or implicit in the mind of the investor. When other central banks do such a thing their Government bonds move along the asset risk-hierarchy but other assets do not get impacted. When the Fed modifies the interest rates the whole hierarchy moves up - it affects all the asset classes. With the impending rate hike by one of the biggest economies in the world we are looking at asset price rerating across the world.

Hike pushes investors into action Generally a reduction in rates allows existing investor more room as prices tend to increase in case of the rate cut. However, when the Fed hikes the interest rates, the riskier asset prices depreciate. This effect tends to push marginal investors into selling thereby creating an opportunity for broader sell off.

The current sell-off seems more likely to be such a sell-off. It is unlikely that this sell-off has anything to do with China. China unfortunately slowed down at that very time and to top it off indulged into some anti-market moves that further spooked the markets. Naturally that has prolonged and aggravated the current sell-off.

Meaning of slowing China China is highly export driven economy. The GDP contribution from investments was growing substantially. Post the 2008 crises two things happened - China increased the investment spending - investment to GDP ratio was ~ 40%, and did it in face of tapering consumption demand. The underlying assumption being that China hoped developed market demand will take-off in coming years.

Had demand returned China GDP would still look robust. It means developed world demand has not returned - despite reasonable GDP growth in developed economies. THAT to my mind is a bigger scare than simply China slowing down.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

The American economy, its size, and its global linkages make it core factor in asset price calculations. The US is a primary exporter of capital to most of the important markets of the world. It is also usually the most important sizeable end-consumer for many including China. Comparatively China is less inter-connected.

A US asset price rerating will affect everyone. There is a risk hierarchy of assets explicit or implicit in the mind of the investor. When other central banks do such a thing their Government bonds move along the asset risk-hierarchy but other assets do not get impacted. When the Fed modifies the interest rates the whole hierarchy moves up - it affects all the asset classes. With the impending rate hike by one of the biggest economies in the world we are looking at asset price rerating across the world.

Hike pushes investors into action Generally a reduction in rates allows existing investor more room as prices tend to increase in case of the rate cut. However, when the Fed hikes the interest rates, the riskier asset prices depreciate. This effect tends to push marginal investors into selling thereby creating an opportunity for broader sell off.

The current sell-off seems more likely to be such a sell-off. It is unlikely that this sell-off has anything to do with China. China unfortunately slowed down at that very time and to top it off indulged into some anti-market moves that further spooked the markets. Naturally that has prolonged and aggravated the current sell-off.

Meaning of slowing China China is highly export driven economy. The GDP contribution from investments was growing substantially. Post the 2008 crises two things happened - China increased the investment spending - investment to GDP ratio was ~ 40%, and did it in face of tapering consumption demand. The underlying assumption being that China hoped developed market demand will take-off in coming years.

Had demand returned China GDP would still look robust. It means developed world demand has not returned - despite reasonable GDP growth in developed economies. THAT to my mind is a bigger scare than simply China slowing down.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

July 7, 2015

Lesson from Grexit

Grexit teaches us something fundamental.

Two Approaches to debt There are two fundamental approaches to debt.

First is the Capitalistic Approach. It says creditors must make investment with eye on risk and should their assessment be wrong, they must take hair-cut. The counter-burden on the debtor is that debtor is forced into austerity so that they make adequate efforts to get the creditors adequate return on their investment. Thus a debtor who made a risky investment is required to pass higher hurdle in the future to prove that his new investment is not as risky. Market adjusts the risk premium to reflect borrowers prudence. A prudent borrower gets lower interest burden while a profligate borrower is required to pay higher.

Second is the Creditor Protection Approach. It protects the creditors to greater extent. The protection afforded comes from various methods. In emergency government could assume private debt (as in EU crisis private debt was assumed by ECB, in 2007-08 crisis even privately owned equity was assumed by the US government). This approach is taken when the creditors are low-risk seeking pension funds or other instrument supporting social benefits. The counter-burden here is not on the debtor, it is on the Government bailing out the creditor. The bailout is only complete if the debt burden is reduced thus, here, the Government takes the hair-cut. This is an approach that promises debt jubilee.

The essentials We may note that hair-cut is an essential ingredient of both approaches. The question is only as to who takes the hair-cut. When ECB assumed private debt, it assumed the hair-cut as well. Denying that renders the approach useless. This is from the creditor side.

Reducing debtor's burden is also essential feature, with different extent in each model. The Capitalistic Approach favours reducing as against eliminating the debt. Thus, the debtor continues to bear the debt that he can sustainably bear. Conversely, in Creditor Protection Approach the almost the entire debt is waived. So, Greece was right to ask for debt reduction.

The Grexit Model

The EU model fares poorly against either of these approaches. It does not have any essential elements and have worse aspects of both models. It is a sort of mixed model.

The EU/ECB dilemma is that if Greece is allowed a Debt reduction, other PIIGS will be next in line. The current mixed approach will imply that ECB will be left holding the bag for all the PIIGS. Now in a normal sovereign, the central bank and sovereign are two facets of same entity. But in EU's case it is not so - primarily because the peoples of EU are not politically united. Thus, ECB is "owned" by Germany and other non-PIIGS a different sovereign than debtors. Can peoples of EU be politically mature to forge EU into a political union? If they do it will fructify the original EU dream.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Two Approaches to debt There are two fundamental approaches to debt.

First is the Capitalistic Approach. It says creditors must make investment with eye on risk and should their assessment be wrong, they must take hair-cut. The counter-burden on the debtor is that debtor is forced into austerity so that they make adequate efforts to get the creditors adequate return on their investment. Thus a debtor who made a risky investment is required to pass higher hurdle in the future to prove that his new investment is not as risky. Market adjusts the risk premium to reflect borrowers prudence. A prudent borrower gets lower interest burden while a profligate borrower is required to pay higher.

Second is the Creditor Protection Approach. It protects the creditors to greater extent. The protection afforded comes from various methods. In emergency government could assume private debt (as in EU crisis private debt was assumed by ECB, in 2007-08 crisis even privately owned equity was assumed by the US government). This approach is taken when the creditors are low-risk seeking pension funds or other instrument supporting social benefits. The counter-burden here is not on the debtor, it is on the Government bailing out the creditor. The bailout is only complete if the debt burden is reduced thus, here, the Government takes the hair-cut. This is an approach that promises debt jubilee.

The essentials We may note that hair-cut is an essential ingredient of both approaches. The question is only as to who takes the hair-cut. When ECB assumed private debt, it assumed the hair-cut as well. Denying that renders the approach useless. This is from the creditor side.

Reducing debtor's burden is also essential feature, with different extent in each model. The Capitalistic Approach favours reducing as against eliminating the debt. Thus, the debtor continues to bear the debt that he can sustainably bear. Conversely, in Creditor Protection Approach the almost the entire debt is waived. So, Greece was right to ask for debt reduction.

The Grexit Model

The EU model fares poorly against either of these approaches. It does not have any essential elements and have worse aspects of both models. It is a sort of mixed model.

The EU/ECB dilemma is that if Greece is allowed a Debt reduction, other PIIGS will be next in line. The current mixed approach will imply that ECB will be left holding the bag for all the PIIGS. Now in a normal sovereign, the central bank and sovereign are two facets of same entity. But in EU's case it is not so - primarily because the peoples of EU are not politically united. Thus, ECB is "owned" by Germany and other non-PIIGS a different sovereign than debtors. Can peoples of EU be politically mature to forge EU into a political union? If they do it will fructify the original EU dream.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

June 24, 2015

Hussman's timing may be wrong again!

John Hussman predicts epic stock crash in his recent newsletter. He says:

Only long-term sustainable, predictable employment creates a turnaround. Till this I agree with him. Now comes the crucial issue of timing. Here he says:

If Fed hikes, it will interfere with the risk equation causing "a breakdown in market internals" as Hussman calls it causing precipitation. But it is unlikely that Fed will hike. Fed may experiment with a token hike but may quickly reverse. Or, more likely, Fed will signal a prolonged pause (lasting more than a year or two).

If Fed does not hike, things won't be as simple as 5.5% annual growth. It will be more. The past data behind this calculations comes from low monetary expansion era. When there is a flood of money, prices should inflate commensurately. Thus, if Fed does not hike, S&P may average annual growth of ~10% or more for few years.

Hence, S&P may double from here before Hussman's prediction comes true. We, no doubt, are establishing an extreme. We are confounded by its extremity.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

The financial markets are establishing an extreme that we expect investors will remember for the remainder of history, joining other memorable peers that include 1906, 1929, 1937, 1966, 1972, 2000 and 2007.He follows up with another gem:

Enlightened members of the FOMC should even question the theoretical basis for their actions. The Phillips Curve is actually a scarcity relationship between unemployment and real wage inflation – basically, labor scarcity raises wages relative to the price of other goods (see Will The Real Phillips Curve Please Stand Up and the instructive chart from former Fed governor Richard Fisher in Eating our Seed Corn). That’s the only variant of the Phillips Curve that actually holds up in the data, and there is no evidence that this or other variants can be reliably manipulated through monetary changes.

Only long-term sustainable, predictable employment creates a turnaround. Till this I agree with him. Now comes the crucial issue of timing. Here he says:

They want to believe that the Federal Reserve has their backs; that as long as the Fed doesn’t explicitly hike interest rates, the market will move higher indefinitely. We saw one question last week that asked “What if the Fed doesn’t raise rates for another 20 years?” Let’s start with an aggressive, optimistic estimate. If we assume that despite conditions warranting two decades of zero interest rates, nominal GDP and corporate revenues will grow at their long-term historical norm of 6% annually over the coming 20 years, we would expect the total return of the S&P 500 to average about 5.5% annually over the next two decades (see Ockham’s Razor and the Market Cycle for the arithmetic behind these estimates). Even in this optimistic scenario, to imagine that this path would be smooth would have no basis in history, requiring the absence of any external shock for the entire period (and I’ve already demonstrated, I hope, that many of the worst market declines in history have been accompanied by Federal Reserve easing).

If Fed hikes, it will interfere with the risk equation causing "a breakdown in market internals" as Hussman calls it causing precipitation. But it is unlikely that Fed will hike. Fed may experiment with a token hike but may quickly reverse. Or, more likely, Fed will signal a prolonged pause (lasting more than a year or two).

If Fed does not hike, things won't be as simple as 5.5% annual growth. It will be more. The past data behind this calculations comes from low monetary expansion era. When there is a flood of money, prices should inflate commensurately. Thus, if Fed does not hike, S&P may average annual growth of ~10% or more for few years.

Hence, S&P may double from here before Hussman's prediction comes true. We, no doubt, are establishing an extreme. We are confounded by its extremity.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

May 26, 2015

The Boring Banking Industry?

Two of the leading voices in finance Frances Coppola and Yves Smith are in a disagreement - sort of a pseudo-disagreement if you ask me - over whether banking should be boring or not. The question itself is the reason for the confusion. Banking should be boring was endorsed by Elizabeth Warren too.

I think Banking should be my kind of boring. By boring I mean two things - it should not be unnecessarily complex, and it should be capable to meet the complexity inherent in banking. Retail banking is not boring - for wrong reasons. It confounds the public with products that are too complex for their needs. At the same time, the back end that supports these products (read - corresponding asset liability matching mechanism, hedging etc.) is not as sophisticated. Investment banking on the other hand is too boring - meaning it does the complex shit right but it passes that shit to people who have no clue without retaining any skin in the game.

Banking has multiple facets:First there is a probability management that allows banks to take deposits for different terms and make loans for different terms and manage the asset-liability gap. This is similar to the insurance industry managing premiums and payouts. A smaller part of this is managing float which is a skill by itself. This is more like extremely short term trading.

The second aspect of banking is your ability to make loans that will pay a decent return without going bust. It is often known as the essence of banking. Borrowers whetting, background checks, credit history check etc. forms part of this aspect of banking.

Third aspect of banking is about sales of a variety of investment products. Here the retail staff of the bank tries to meet its sales targets by selling complex investment products to unsuspecting customers. The customers, most often, are meeting these sales-people to get some transaction done - they are not there to seek investment products.

Fourth aspect is support services which can be totally outsourced. This aspect covers your cheque-book issuances, mailing the account statements, keeping the personal records up to date. Issuing certificates for taxes, etc. On the asset side - it deals with record keeping, and procedural stuff. It is fairly automated and most customers can be empowered to do it themselves as well.

Understanding banking:We cannot classify banking into retail and investment banking and expect to gain any new understand. We need to cut banking up into two chunks - transaction management and investment management.

Transaction management should be boring - like telephone exchanges or something. It should simply be WYSIWYG. It is also similar to McDonalds - it is basic and simple but you need to have skills to pull of the quick delivery at low cost. Meaning it is more a function of skill (can be acquired by repetition) than expertise (research, experience and insight are essential)

On the flip side, the investment management side should be complex. Now loans are debt investments and so is float. Selling investment products is as different from transaction management as chalk and cheese. You need experts to sell those products and ensure that they are not mis-sold. This part has been wrongly simplified. This part requires expertise.

What is boring?

Currently what is boring is selling investment products - which shouldn't be. Most people I know - yes most - do not understand the risks with any of the investment products they buy. It can be insurance policies, term deposits, mutual funds, debt funds, real estate or whatever.

Now basic risk management tells us that just because you buy different products does not mitigate your risks - sometimes your risks may go up. This risk compounding is not even understood by the practitioners let alone the customers. The sellers of these products, to use a popular phrase, get a salary to not understand them.

Now credit cards and over-drafts are not simple transaction management products. They are in fact loan products and deserve to be sold professionally. Most of the unnecessary complexity lies here. People who go for credit cards do not understand the terms of loan they are entering - and Warren has highlighted it time and again. Same goes with OD - while it is not as bad as credit card terms - hereto people do not understand what they are getting into.

There is quite a bit of complexity in term deposit side as well. If we really examine, most of the depositors do not make as much from their deposits as they should. The optimisation is never explained and never understood. It is in the interest of banks that depositors do not understand this - CASA (current account - savings account) helps keep the cost of capital low.

These cannot be boring - quite the opposite. These issues need to be explained - some by the banks selling these products, others by general education.

What is not boring?

Conversely, the transaction management is unnecessarily complicated. Real time settlement should have been a norm now - yet banks do enjoy settlement floats on many payment mechanisms. These represent the money the banks use after the debit the account and before they credit the account of the beneficiary.

One source of complications in transaction is authentication and identification. These cannot be eliminated as they exist to keep your bank account safe. However, all other sources of complexity are available for simplification.

Transaction fees are pretty complex, sometimes they are waived other times you get charged for using some facility during a holiday or something like that.

In sum

Banking is simple and complex at the same time - just not in the right places. It is time to rewire banking - simplify it just as much as required and no more.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

I think Banking should be my kind of boring. By boring I mean two things - it should not be unnecessarily complex, and it should be capable to meet the complexity inherent in banking. Retail banking is not boring - for wrong reasons. It confounds the public with products that are too complex for their needs. At the same time, the back end that supports these products (read - corresponding asset liability matching mechanism, hedging etc.) is not as sophisticated. Investment banking on the other hand is too boring - meaning it does the complex shit right but it passes that shit to people who have no clue without retaining any skin in the game.

Banking has multiple facets:First there is a probability management that allows banks to take deposits for different terms and make loans for different terms and manage the asset-liability gap. This is similar to the insurance industry managing premiums and payouts. A smaller part of this is managing float which is a skill by itself. This is more like extremely short term trading.

The second aspect of banking is your ability to make loans that will pay a decent return without going bust. It is often known as the essence of banking. Borrowers whetting, background checks, credit history check etc. forms part of this aspect of banking.

Third aspect of banking is about sales of a variety of investment products. Here the retail staff of the bank tries to meet its sales targets by selling complex investment products to unsuspecting customers. The customers, most often, are meeting these sales-people to get some transaction done - they are not there to seek investment products.

Fourth aspect is support services which can be totally outsourced. This aspect covers your cheque-book issuances, mailing the account statements, keeping the personal records up to date. Issuing certificates for taxes, etc. On the asset side - it deals with record keeping, and procedural stuff. It is fairly automated and most customers can be empowered to do it themselves as well.

Understanding banking:We cannot classify banking into retail and investment banking and expect to gain any new understand. We need to cut banking up into two chunks - transaction management and investment management.

Transaction management should be boring - like telephone exchanges or something. It should simply be WYSIWYG. It is also similar to McDonalds - it is basic and simple but you need to have skills to pull of the quick delivery at low cost. Meaning it is more a function of skill (can be acquired by repetition) than expertise (research, experience and insight are essential)

On the flip side, the investment management side should be complex. Now loans are debt investments and so is float. Selling investment products is as different from transaction management as chalk and cheese. You need experts to sell those products and ensure that they are not mis-sold. This part has been wrongly simplified. This part requires expertise.

What is boring?

Currently what is boring is selling investment products - which shouldn't be. Most people I know - yes most - do not understand the risks with any of the investment products they buy. It can be insurance policies, term deposits, mutual funds, debt funds, real estate or whatever.

Now basic risk management tells us that just because you buy different products does not mitigate your risks - sometimes your risks may go up. This risk compounding is not even understood by the practitioners let alone the customers. The sellers of these products, to use a popular phrase, get a salary to not understand them.

Now credit cards and over-drafts are not simple transaction management products. They are in fact loan products and deserve to be sold professionally. Most of the unnecessary complexity lies here. People who go for credit cards do not understand the terms of loan they are entering - and Warren has highlighted it time and again. Same goes with OD - while it is not as bad as credit card terms - hereto people do not understand what they are getting into.

There is quite a bit of complexity in term deposit side as well. If we really examine, most of the depositors do not make as much from their deposits as they should. The optimisation is never explained and never understood. It is in the interest of banks that depositors do not understand this - CASA (current account - savings account) helps keep the cost of capital low.

These cannot be boring - quite the opposite. These issues need to be explained - some by the banks selling these products, others by general education.

What is not boring?

Conversely, the transaction management is unnecessarily complicated. Real time settlement should have been a norm now - yet banks do enjoy settlement floats on many payment mechanisms. These represent the money the banks use after the debit the account and before they credit the account of the beneficiary.

One source of complications in transaction is authentication and identification. These cannot be eliminated as they exist to keep your bank account safe. However, all other sources of complexity are available for simplification.

Transaction fees are pretty complex, sometimes they are waived other times you get charged for using some facility during a holiday or something like that.

In sum

Banking is simple and complex at the same time - just not in the right places. It is time to rewire banking - simplify it just as much as required and no more.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".