Farnoosh Torabi's Blog, page 18

April 23, 2014

Get Rich Slowly: The Course!

Do you have a personal career hero? Someone you consider to be a role model in your specific field?

As a financial writer and still-aspiring leader in the online financial space, one of my career heros is J.D. Roth. When it comes to the who’s who in the financial blogosphere, J.D. is the messiah. In 2006, he launched Get Rich Slowly, an award-winning website, which has been heralded as the Web’s most inspiring personal-finance blog by Money Magazine. He’s also the author of Your Money: The Missing Manual.

I’m excited to announce that J.D. has a brand new 52-week course called Get Rich Slowly: The Unconventional Guide to Mastering Your Money. The program starts at just $39.

J.D. spent the past year developing the online course and as part of the curriculum he’s created a special guide called “Be Your Own CFO.”

“My premise is that if people were to manage their personal finances as if they were managing a business, they’d be much more successful with money,” he tells me. The spectacular course also includes weekly emails featuring J.D.’s best money tips, as well as 18 audio interviews and transcripts with money gurus Liz Weston and Jean Chatzky, Gretchen Rubin, author of The Happiness Project, and many more. Plus, tons of downloadable support material.

It’s finally available and I hope you’ll consider joining.

Just click HERE to learn more and sign up.

April 22, 2014

How Women Breadwinners Can Save Their Relationships

When She Makes More received a very thoughtful and balanced review on Forbes.com, written by staff writer Susan Adams. While Adams did not agree with every point in the book (naturally), I sense that she appreciated my researched suggestions to help breadwinning women – and the men who love them – thrive in their relationships. In her words, “The phenomenon of the breadwinning woman will only keep growing. We’ll see a lot more books like Torabi’s, which will be a good thing.”

Below is the beginning of Adams’ review. For the rest, please visit Forbes.com.

Farnoosh Torabi’s new book, When She Makes More: 10 Rules for Breadwinning Women,takes on a trend that’s posing an ever-greater challenge to married couples and that I’ve experienced in my own home. Millions of women earn more than their spouses. According to Torabi, who speaks, writes and does TV spots about personal finance, in a quarter of American households with children under age 18, the mother is the primary source of income. That’s more than five million women, a number that has quadrupled since 1960. If only that were a universally good thing for families. Instead Torabi ticks off a host of problems she’s dug out of academic studies and from Pew Research Center reports.

A few highlights: A 2010 Cornell study found that among 18- 28-year-old married and cohabiting couples who had been together for more than a year, men who were totally dependent on women’s salaries were five times more likely to cheat than men who earned the same as their partners. Other studies show that when women earn more, they wind up taking on more, not less of the housework and childcare. A 2013 study by a professor at Washington University’s Olin Business School in St. Louis who collaborated with some Danish colleagues revealed that in relationships where women made slightly more than their spouses, men were 10% more likely to need prescription medication for erectile dysfunction, insomnia and anxiety, and the greater the income gap, the more problems men had with ED. Torabi conducted her own survey of 1,033 professional women and found that the women who made more than their partners reported less relationship satisfaction and more embarrassment about how much they made compared to their spouse than the women who earned less.

April 21, 2014

Today: Is it Worth It?

On the Today show this morning I discussed which insurance policies – from extended warranties to travel insurance – are really worth it.

Visit NBCNews.com for breaking news, world news, and news about the economy

Extended Warranties

According to Consumer Reports, their advice is to skip it! The extended warranty kicks in after the manufacturer’s own free warranty, which usually lasts one year and for many appliances and tech gear – if they break down – will usually do so within that time frame.

That said, for complex or new technologies or those you think may be more susceptible to damage or theft – a lengthier warranty which kicks in after the manufacturer’s warranty may be worth it. I personally have always benefited from extended warranties for my Mac computer and iPhone and even phones owned prior to the iPhone…I’m clumsy. I drop things and forget where I leave things. Replacing an iPhone, for example, is far more expensive than AppleCare ($99 for iPhones and iPads, $250 for Macbooks).

Travel Insurance

More and more, this is a YES, as it can be very expensive to switch or cancel your travel plans. If you are booking any non-refundable travel, then this should be a serious consideration. Airlines, as we know, tend to impose heavy fees when we want to change our travel plans. And travel insurance (aka trip insurance) –depending on the package you get – not only reimburses you in case you have to cancel your trip for any reason…it may also include medical coverage, which can be extremely smart to get if you’re going to a foreign country and your medical coverage doesn’t extend beyond the U.S.

The cost is anywhere from 4 to 8% of your trip’s value.

Whole Life Insurance

Life insurance, in general, is only necessary if you have dependents like children or others who require financial support from you. It replaces your income and can benefit the needs of your dependents in the event of your death. There are two types: WHOLE (also known as Permanent) and TERM.

Most people are fine purchasing TERM life insurance, which provides basic coverage for a limited number of years. It expires after say, 10, 15 or 20 years from the day you buy it and begin paying into it. For most people, TERM is the way to go. It’s more affordable…for example, if you’re 35 years old, healthy and take out a policy starting now and for the next 20 years, you’re looking at $150 to $250 a year. Source: https://www.trustedchoice.com/life-insurance/compare-coverage/cost/

WHOLE insurance, on the other hand, is designed to be in place for your entire lifetime and has a guaranteed death benefit. It also comes with a partial cash value that you can borrow against at any time. So it, has a lot more flexibility which may be attractive to some people who want an additional way to protect finances down the road. But the annual cost is MUCH higher, six to 8 times higher than TERM. And so high that policyholders have a hard time paying the premiums. One study by the Society of Actuaries found that 20% of whole life policies get canceled in the first three years or 40% within the first 10 years because people can’t keep affording the premiums.

Home Warranty

I like home warranties. A home warranty protects NEW homebuyers against breakdowns related to large appliances, and electrical and plumbing issues within the first year or so of moving into a new home. According to the Executive Director and General Counsel of Service Contract Industry Council, it can cost anywhere from $300 to $500.

Sometimes the seller or homebuilder will foot the cost of the insurance as an incentive. This could be worth it because it buys peace of mind. Typically you see this type of insurance offered with homes that are newly constructed.

This is not to be confused with home insurance, which is a separate protection you buy from an insurance agent that covers your property against bigger issues like theft, certain weather damage, fire, etc.

Forbes

“Torabi…offers some thoughtful analysis and tries out considered and provocative solutions.”

When He Makes Less

While my new book, When She Makes More, directs advice towards breadwinning women, it is also a celebration of the wonderful, supportive men who love them.

Edward Coambs is one of these amazing men. He wrote to me a short while ago saying that after viewing my short trailer for the book, he became quite emotional. His wife, a dentist, makes more than him. After they had their first child he felt the need to step off the corporate track and become a full-time stay at home parent. “It has been an incredible journey for the last three three years… To say that our family has felt stress in the most unusual ways is an understatement,” he told me.

I can’t tell you how much I appreciate Edward’s honest feedback. I asked if he’d be willing to share more about his story for my blog and he generously agreed. Here is his story, a man’s reflection on what it is like to be in a relationship with a woman he loves, who happens also to make more.

Edward’s story begins here:

Little did I know how a trip to the pool hall would change my life forever. That night, a group of mutual friends introduced me to the love of my life: a stunning, captivating woman in her last year of dental school. I had never met anyone like her. At the time, I was the Average Joe: a firefighter completing my undergraduate degree in business, and I was mesmerized by the professional path she had chosen.

My wife and I have now been married seven years. She has since started her own dental practice, and I have gone on to complete two graduate degrees. Despite all of the encouragement and support I have gotten on my journey, I have always felt a bit weird about having a wife who makes more than me, but I seldom express my own feelings of inadequacy.

While I would love to see myself as some super self-confident guy, I struggle at times with my sense of self and being the provider for my family. You see, doctors typically receive a certain level of dignity and respect because of their profession, and I sometimes feel I’m in the shadow of that. The only way that I could figure out how to step out of that shadow was to continually educate myself – hence the two master’s degrees.

“Despite all of the encouragement and support I have gotten on my journey, I have always felt a bit weird about having a wife who makes more than me, but I seldom express my own feelings of inadequacy.”

I have had plenty of guy friends say they would love to be in my position. Yet, I feel like they really don’t understand what it is like when she makes more. While our culture is starting to be more conscious and accepting of female breadwinners, for me, there have been many explicit and implicit messages about the role of the man in the family. They have only been exacerbated by me stepping off the corporate track and becoming a stay-at-home dad and full-time graduate student. As a result, I entered two new worlds. First, I became totally reliant on my wife to provide for our family. Then, I found myself serving as “Mr. Mom.” Talk about feeling out of place. During this season of life, it took a lot of patience, energy and support to maintain my sense of masculinity.

I found myself serving as “Mr. Mom.”

Talk about feeling out of place.

My wife has never made a big deal out of making more money then me. She has always provided me with the greatest levels of respect and dignity, especially in the simple things, like letting me pay for dinner on date night. Okay, I know that seems superficial, but it has helped me maintain a sense of masculinity. When she makes more, it really causes you to think about what it means to be a man and challenges our traditional view of men’s and women’s roles in marriage.

Up until this point, I’ve focused on my wife the dentist, but she’s also my wife the woman. Fortunately, I fell in love with the woman. What I have come to see over time is that my wife looks to me for nurturing, love and support – not money. Because her expectations of me are in line with what I can offer, we have a very healthy and enjoyable marriage.

Ed Coambs is a Certified Financial Planner and the founder of Marriage and Money Matters which help families build a financial house that matters.

April 16, 2014

Oh, Phyllis. My Open Letter to the “Pro Family” Conservative

I seriously regret eating my veggie lasagna leftovers for lunch…especially right before reading Phyllis Schlafly’s Christian Post op-ed entitled, “Facts and Fallacies About Paycheck Fairness.”

I’m quite nauseated…and also feel really, really sorry for Phyllis. It’s because of folks like her with such antiquated – and deranged – views on what women’s roles “should be” that I dedicate an entire chapter in my upcoming book, “When She Makes More: 10 Rules for Breadwinning Women,” The chapter offers prescriptive advice on how modern women and men can deal with these sometimes overbearingly judgmental individuals. In everyone’s life a little Phyllis Schlafly may fall. It could be a parent, a coworker or neighbor who just.doesn’t.get.it.

And the advice for those of us on the other end of the dribble goes something like this, “Find compassion for the haters, for they may never be able to understand what’s real and what’s bright, as you have.”

I have to say that I’m also confused, Phyllis. First and foremost, what are your sources? You seem to be making things up as you go along. For example, you write:

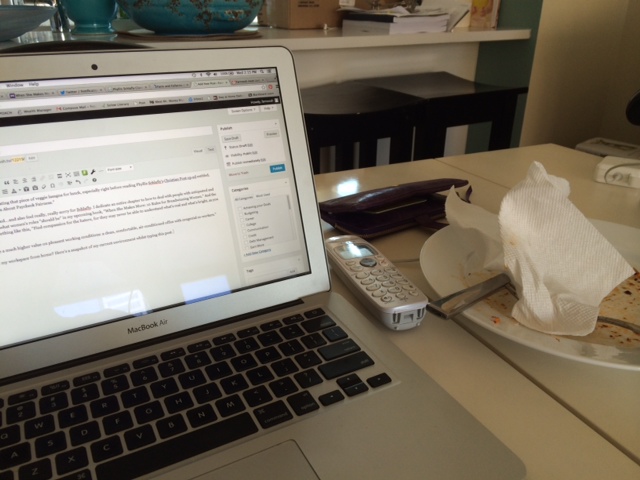

“Women place a much higher value on pleasant working conditions: a clean, comfortable, air-conditioned office with congenial co-workers.”

Um, have you seen my workspace/kitchen table from home? Here’s a snapshot of my current work environment. (Say hi to my lasagna crumbs!)

“A successful woman who reaches a high rank in her career is more likely to reduce her working hours.”

Even if this is true, why might be this be, hmm? Could it be that she has a family waiting for her at home and wants to be at the forefront of her parenting responsibilities – in addition to working cruel hours at a company that likely has limited maternity leave, let alone a paternity leave policy? Perhaps her boss won’t cut her a break so she’s forced to compromise somehow? Oh, nevermind. I suppose this fat paycheck lady is just leaving early to get her nails done, right Phyllis? Where ARE her priorities?

Then you drop this bomb: “Women voluntarily” choose “lower pay.”

I can’t even.

And then the icing on the cake: “Perhaps an even more important reason for women’s lower pay is the choices women make in their personal lives, such as having children.”

I’m 7.5 months pregnant. I *think* my husband is aware, but I haven’t actually stopped to ask him if he knows we’re having a baby. I mean, I don’t want to bother him with “my choice” to have children.

Perhaps I should also confess to him that I make more?

What say you, Phyllis?

Join Me in New York City!

To celebrate the launch of my new book, When She Makes More, I’d like to invite you all to a special evening at the historic Henri Bendel boutique in New York on May 6th. Enjoy a Q&A with me discussing my findings in WSMM, some light shopping at Henri Bendel and meeting fellow fantastic people (while enjoying champagne & chocolates!)

Event details are below. This is a ticketed event. It costs $35 and includes a $35 HB gift card, signed hard copy of When She Makes More and other goodies – a more than $100 value! You can reserve your spot here.

April 12, 2014

Farnoosh’s Mail Bag: How to Invest?

Well, I’ve got some advice…!

Hooman asks: “The stock market…is very confusing for me. What do you recommend to someone trying to build up his future. I am not sure what investment path to choose.”

Hooman, you’re not alone. The stock market is hardly an easy or predictable thing. Figuring out which direction stocks will move is anyone’s guess! The best way to invest and take advantage of the stock market – without the hassle of trying to understand its every move – is to participate in a tax-friendly retirement fund like your employer’s sponsored retirement fund (e.g. a 401(k)) and/or an individual retirement account (IRA). I’ve got more details on these investments here.

Neville asks: “I’ve been slowly getting my finances in order and I finally am in control (lots of debt and spending in my 20′s). I have a stable job, but feel behind in savings. How much should someone have by their mid 30s in retirement? If I have 10% of salary going to retirement should I increase to make up for my 20′s? Also, what is the average debt for people in my age range (with no mortgage).

Hooman, congratulations for getting your financial ducks in a row! We all make mistakes and run into a little (or a lot of) debt in our 20′s (myself, included). First things first (before beefing up retirement), I’d recommend you shore up at least 6 months of emergency savings. Calculate all of your fixed expenses for one month: housing, gas, food, utilities, insurance, etc. and multiply by 6. Try to sock away at least that much in a liquid account first. This will ensure that if you lose your job or run into a financial bind, you don’t have to resort to credit cards again to make ends meet.

Now, as for retirement, since you didn’t invest much – or at all – in your retirement account in your 20′s, I’d say try to invest a little bit more than 10% for now. You have some important catching up to do, I won’t lie. It’s hard to say how much you *should* have saved by your mid 30s. But I can tell you that when I started to save for retirement in my early 20′s, I put aside 10% every year. By the time I hit 30, I had a little over $60,000 saved. I actually just read a recent article on Slate.com that estimated how much we should have saved by a certain age, depending on our current average incomes. For example, a 40 year-old earning $100,000 should have roughly $200,000 in retirement savings. I don’t entirely agree with this chart (I think it’s a bit too aggressive). It’s an interesting assumption, but overall, I think there’s no way to calculate an exact answer for everyone.

Here’s some of my general investment advice when it comes to saving in a retirement account:

Run the Numbers

How much you need to save depends on when you’d like to retire, in addition to what kind of lifestyle you envision having during retirement. Plan to live on the beach? Plan to work in retirement? You can crunch some of these numbers with help from your company’s 401(k) provider or, you can use free online retirement calculators at ChooseToSave.org and AARP.org.

Commit to 10%

If you have no clue when you plan to retire or what your expense will look like, a good rule of thumb is to invest at least 10% of your annual income into a retirement account, such as a 401(k) or IRA. The maximum contribution this year to a 401(k) is $17,500. For IRAs, it’s $5,500.

Stay Diversified

Diversification is a tried and true strategy to sound long-term investing. Aim for a mix of stocks, bonds and cash-like investments in your retirement portfolio. How to diversify, exactly? That depends largely on your age and risk tolerance. If you’re young and able to afford more risk, investing in 85% stocks, 10% bonds and 5% money market funds, may be one way to go.

Auto-Rebalance

Over time, it’s likely that your portfolio’s allocation will shift with movements in the stock market. For example, after a difficult year in the market, you may end up with too much weight in bonds and not enough in stocks. It’s important to rebalance your portfolio at least once a year to get it back to its original composition. Or, better yet – if your company offers it, opt for “automatic rebalancing,” which lets your plan manager rejig your investments automatically.

Avoid Knee-Jerk Reactions

As we learned in the previous recession, emotion-driven, knee-jerk reactions tend to be irrational, so avoid making any impulsive moves with your money when you watch stocks drop. You don’t want to pull out now, only to miss out on the rebound. Keep in mind: Many 401(k) investors who stayed the course managed to recoup their losses. In fact, according to Fidelity Investments, those who invested in target-date funds (aka age-based funds) and stayed the course during the 2008-2009 financial crisis, finished with the highest account balances by the summer of 2011, versus those who reduced or stopped contributing.

April 8, 2014

Equal Pay Day: One Bright Spot

Did you know that “Equal Pay Day” has technically been around since 1996? I certainly did not.

This year the public awareness event is receiving what seems to be unprecedented media attention, as the country and key influencers make gender pay equality a top priority. Books like Lean In, new research from the Pew Institute and veteran journalists like Maria Shriver have brought the issue back into the limelight.

President Obama has even announced two executive orders to close the gender wage gap.

With my book, When She Makes More, coming out May 1, reporters have been reaching out to me today to capture my thoughts on the topic. Where do we see progress and how can women earn more in the workplace?

One bright spot is that young women have narrowed the pay gap. While the overall wage disparity has women making on average 77 percent less than men, the gap, according to Pew Research, is 93 percent between Millennial men and women.

Part of what is fueling this trend is the fact that women are achieving greater academic success. Beginning in grade school, young female students are generally earning higher grades than their male classmates, due to what researchers cite as better “approaches towards learning.” Girls are characterized as more attentive, eager to learn and organized when it comes to education – and teachers are rewarding them for that. Young women are also enrolling in college and graduating with diplomas at higher rates than men. In the graduating class of 2013, women earned the majority of Bachelor’s and Master’s degrees. The projection is the same for 2014 and beyond.

In recent years the employment market has also favored women in certain ways. In the last decade the male-dominated manufacturing sector, for example, has shed almost six million jobs, nearly one third of its total work force, and has taken in few young workers. Meantime, job openings in health, education, and services, sectors that tend to be led by female employees, have been on the rise.

Women are also prioritizing their professional lives more than men during their younger years. A 2012 Pew Research Center study found that 66 percent of young women ages 18 to 34 rate their career high on their list of life priorities, compared with 59 percent of young men.

The older women get, though, the tougher it becomes to maintain that earnings momentum partly due to more moms taking time off to raise their families. Unfortunately, paternity leave, even when offered, is not something most working fathers are willing to take. Senior level and executive positions, which pay more, are also still, by and large, going to men. And of course, we have the issue of gender discrimination still at play in the workforce, contributing to the income disparity – and something the President is attempting to address with new laws.

What do you think about all of this? What are some other forces weighing down on a woman’s ability to earn as much as her male colleagues?